This article was previously published in New Suits: Appetite for Disruption in the Legal World, edited by Michele DeStefano and Guenther Dobrauz (Stämpfli Verlag, 2019).

The word “alternative” is definitely trending in the legal zeitgeist. Beginning with the U.K. Legal Services Act and accelerating through the legal tech startup boom, discussion about the growing importance of alternative business structures (ABSs) and alternative legal service providers (ALSPs) has become a cottage industry in the legal press, and increasingly in the legal academy as well. And for good reason. According to a recent report by Thomson Reuters, Georgetown Law’s Center on Ethics and the Legal Profession, the University of Oxford’s Said Business School, and Acritas (a leading provider of legal market intelligence)—a collaboration that in and of itself is a powerful indication of how widespread the discussion of this topic has become—revenues from ALSPs grew from $8.4 billion in 2015 to $10.7 billion in 2017—a compound growth rate of 12.9 percent. Nor is this growth limited to just a few industries or kinds of alternative services. As the Thomson Reuters report documents, more than one-third of companies, and more than 50 percent of law firms, report that they are currently using at least one of the top five functions typically performed by ALSPs. At the same time, all of the Big Four accountancy networks—PwC, Deloitte, EY, and KPMG—have received ABS licenses to operate as multidisciplinary practices (MDPs) in the United Kingdom. Given the exponential growth in the number of legal startups over the past few years, it is no surprise that practitioners and pundits alike expect, according to a 2018 Altman & Weil report, that “competition from non-traditional services providers will be a permanent trend going forward in the legal services market.”

Some law firms will surely “die” and some lawyers will surely lose their jobs. Nevertheless, we believe that so-called “traditional” large law firms will continue to occupy an important place in the legal ecosystem for the foreseeable future.

And yet, for all the talk about the growing importance of these “alternatives,” the very discourse used to cast these new providers as the harbingers of impending dramatic changes in the market for legal services continues to marginalize and mask their true significance. Specifically, by labeling everything from legal tech startups, to long-established outsourcing and electronic discovery providers, to leading information and technology companies and the Big Four as “alternatives,” the current debate reinforces the prevailing wisdom, as succinctly stated by John Croft, president and co-founder of Elevate in a 2018 Artificial Lawyer article, that “there is one ‘proper’ way of providing legal services (i.e., going to a traditional law firm) and any other way is ‘alternative’ (i.e., wrong/new/risky!).”

It is not surprising that the discourse has evolved in this fashion. In medicine, for example, “authorities have devoted significant energy and resources to making sure that alternatives maintain lesser status, power and social recognition either alongside or within the margins of dominant systems.” Given that lawyers exert even more control over the regulatory system that governs law than doctors do in medicine, it is entirely predictable that incumbents have worked hard to cabin the legitimacy of these potentially “subversive elements” of the legal ecosystem, to borrow Ross’s evocative phrase about medicine, as “alternatives” to “real” law firms. Indeed, even the Merriam-Webster Dictionary defines the word “alternative” as “different from the usual or conventional; existing or functioning outside the established cultural, social, or economic system.” As a result, the only unifying definition that Thomson Reuters et al. could muster in their original report on this phenomenon was to say that ALSPs “present an alternative to the traditional idea of hiring a lawyer at a law firm to assist in every aspect of a legal matter.” Tellingly, their 2019 report makes no attempt at all to define what constitutes an ALSP.

In this article, we argue that this characterization of the range of new providers competing for a share of the global corporate legal services market is fundamentally flawed. This is not because we believe that we are about to witness “the death of big law” or, even more dramatically, “the end of lawyers.” To be sure, some law firms will surely “die,” and some lawyers will surely lose their jobs. Nevertheless, we believe that so-called “traditional” large law firms will continue to occupy an important place in the legal ecosystem for the foreseeable future—although as we suggest below, the law firms that prosper will be those that harness what we define as “adaptive innovation” to respond to their clients’ changing needs. But the ecosystem in which both law firms and a wide range of other providers will compete is one that will increasingly require the integration of law into broader “business solutions” that allow sophisticated corporate clients to develop customized, agile, and empirically verifiable ways of solving complex problems efficiently and effectively. As this ecosystem matures, it will both decenter traditional understandings of how to provide high-quality legal services, while at the same time raising critical questions about how to preserve traditional ideals of predictability, fairness, and transparency at the heart of what we mean by the rule of law. Understanding the dynamics of this new ecosystem will be critical for all legal service providers seeking to do business in the new global age of more for less.

The very discourse used to cast these new providers as harbingers of impending dramatic change continues to marginalize and mask their true significance.

Our argument proceeds in three parts. First, we briefly locate the current demand for ALSPs within the broader context of the large-scale forces that are reshaping the global economy and therefore inevitably reshaping the market for corporate legal services in which both “traditional” and “alternative” providers compete. These forces, we argue, are producing a market that favors “integrated solutions” and value-based pricing over traditional domain expertise purchased on a fee-for-service basis. Second, we discuss the implications of this trend for legal service providers of all types. Specifically, we argue that corporate clients will increasingly demand professional services that are “integrated,” “customized,” and “agile.” These demands, in turn, will move what are now considered “alternative” providers, such as technology companies, flexible staffing models, and multidisciplinary service firms like the Big Four, to the core of the market, while putting pressure on law firms to articulate how their services contribute to producing integrated solutions for clients. Finally, we conclude by identifying some key challenges that this new corporate legal ecosystem poses for legal education, legal regulation, and the rule of law.

From oligopoly to global supply chains: The evolution of the corporate legal services market

The first thing that is misleading about the current discourse that seeks to define a set of “alternatives” to traditional law firms is that it frequently equates “alternative” with “new.” The original 2017 Thomson Reuters report on ALSPs is typical. After asserting that “traditionally, clients looked to law firms to provide a full range of legal and legally related services,” the report states that “today, by contrast, consumers of legal services find themselves the beneficiaries of a new and growing number of nontraditional service providers that are changing the way legal work is getting done.” But this way of characterizing the current suite of “alternative providers” fails to acknowledge that clients have been looking for alternative ways to source legal services for more than a century—starting with engaging what we now consider to be “traditional” law firms. This historical context is critical to understanding the contemporary market for corporate legal services and its likely future.

ALSP 1.0: The Cravath System

Ironically, what we now consider to be the “traditional” mode of providing corporate legal services was once itself an “alternative.” Before the turn of the twentieth century, there were no large law firms in the United States or, for that matter, anywhere in the world. The overwhelming majority of lawyers were solo practitioners or worked in small and loosely affiliated law firms, serving a mix of individual and business clients primarily by appearing in court. To the extent that America’s businesses had legal needs, they were serviced either by internal lawyers—for example, David Dudley Field, chief counsel to the Erie and Lackawanna Railroad, who was one of the most powerful (and arguably corrupt) lawyers in the latter decades of the nineteenth century—or by a mix of solo practitioners and self-help. It was not until the early decades of the twentieth century that lawyers like Paul Cravath, Thomas G. Sherman, and John W. Davis created what has come to be known as the “Cravath System”—formally organized law firms consisting of “associates” and “partners” hired directly from top law schools, providing a full suite of services to big corporations—that we now take for granted as the norm against which all other service providers should be judged. Moreover, like all “alternatives,” the Cravath System was considered subversive by the legal elites of the day. Committed to the traditional ideal of lawyers as “independent professionals” modeled on the self-employed English barrister, as late as the 1930s these elites derisively described Cravath and other firms as “law factories” that were destroying the soul of the legal profession. (For more on the development of large law firms, see Marc Galanter and Thomas Palay’s seminal volume Tournament of Lawyers [University of Chicago Press, 2019].) Yet, by the 1960s, large law firms following the Cravath System were universally viewed as the gold standard for providing legal services, attracting top talent, and sitting atop the income and prestige hierarchy of the profession.

What we now consider to be the “traditional” mode of providing corporate legal services was once itself an “alternative.”

The Cravath System triumphed because it was exceptionally well-aligned with other key elements of the evolving corporate ecosystem in which these firms operated. Specifically, Cravath System law firms filled an important space in the rapidly expanding “client market” for corporate legal services and took advantage of a rapidly increasing “labor market” composed of law school graduates. With respect to the client market, the first half of the twentieth century witnessed the creation of whole new areas of public and private law governing the conduct of corporations. Yet these entities had little or no internal legal resources to address the problems and opportunities these new laws and regulations created. As a result, corporate clients established long-term and near-exclusive relationships with their principal outside law firms. At the same time, a growing number of new law schools were turning out bright young law school graduates who had been taught to “think like a lawyer” but with virtually no training on how to “be” lawyers and relatively few options for obtaining employment other than “hanging out a shingle” and learning to practice law on their own (or in poorly paid—or even unpaid – and generally unsupervised apprenticeships with established lawyers). As a result, Cravath System firms had no trouble finding an abundance of bright students from top law schools who were eager to join these organizations and willing to work long and demanding hours for the chance of becoming partners with all the perquisites this status credibly conveyed.

By the latter decades of the twentieth century, however, this beneficial alignment had begun to unravel. It is this unraveling that has created the space for a new generation of “alternatives” to emerge.

ALSP 2.0: The in-house counsel movement and its progeny

As Cravath System law firms proliferated and became more profitable, it became increasing clear that this now-traditional way of providing corporate legal services contained the seeds of its own destruction. The form of this disruption to the corporate ecosystem came in the form of the rapid growth of increasingly sophisticated in-house counsel. Beginning in the 1980s, large companies began hiring general counsel (GCs) to oversee all the company’s internal and external legal needs. (For a full treatment on the rise of the general counsel, see The Practice, volume 2, issue 4.) At the outset, these internal lawyers cast themselves as a straightforward alternative to traditional law firms on the simple grounds that it is cheaper to buy wholesale than retail. But this labor arbitrage argument quickly gave way to a substantive claim that in-house lawyers were actually better than their law firm counterparts because they are in a better position to “understand the company’s business” than outside law firms and therefore can better align the legal function to achieve these business objectives. As a result, GCs have increasingly become the company’s “chief legal purchasing agent,” charged with breaking up the long-standing relationships between companies and law firms and requiring firms to compete for every new piece of significant business. At the same time, these increasingly credentialed and sophisticated internal lawyers now act as the company’s “chief legal diagnostician,” determining the company’s legal needs and how these needs fit into the company’s overall strategy and goals—thus becoming a credible alternative to the law firm senior partners who traditionally played this “trusted-adviser” role. This “in-house counsel movement,” as the legal scholar Robert Eli Rosen has aptly labeled this phenomenon, has significantly altered the balance of power within the legal ecosystem by reducing the information asymmetry between corporate clients and traditional law firms.

By the end of the first decade of the twenty-first century, LPOs were an established part of the corporate legal ecosystem.

But as legal costs continued to rise even for companies with large and sophisticated in-house counsel departments, the internal lawyers whose initial claim was that they were a low-cost alternative to traditional law firms began to face increasing pressure to find even lower-cost options to using the expensive fixed-cost resource of full-time in-house lawyers. Not surprisingly, many GCs began turning to the same kinds of “alternatives” that their corporate employers were already using to reduce costs and drive productivity in the business as a whole. General counsel began to experiment with three kinds of alternatives to both traditional law firms and in-house lawyers:

- The “outsourcing” and “offshoring” of low-value and repetitive legal tasks to either captured or independent entities

- “Flexible staffing” solutions, either through “secondments” from law firms or through procuring additional human resources from general or specialized temporary staffing firms

- Multidisciplinary professional service firms (MDPs) offering efficiencies of scale and scope by bundling legal services together with accounting, tax, and consulting services

Collectively, these three supplemental resources further shifted the balance of power between in-house counsel and law firms, while at the same time blurring the boundary between these two “traditional” legal service providers.

ASLP 2.1: Outsourcing and offshoring

The increasing integration of the global economy during the last decades of the twentieth century led many multinational companies to build global supply chains to leverage high-quality, low-cost resources and competitive opportunities around the world. As both global trade and the speed and sophistication of information technology increased, these companies increasingly resorted to labor arbitrage as a means of cutting costs by “replacing higher-waged domestic labor with cheaper foreign labor.” It was not long before GCs began to apply this same logic to legal services.

General Electric, whose legendary GC Benjamin W. Heineman Jr. is widely considered the father of the modern in-house counsel movement, was among the first to pursue this strategy. In 2001, GE established “an in-house legal office in India, staffed by lawyers, to handle issues relating to its plastics and consumer finance divisions.” Many other companies and organizations followed, including law firms like Orrick Herrington & Sutcliff, which opened its Global Operations Center in Wheeling, West Virginia. Many more contracted with the growing number of Indian legal process outsourcing firms (LPOs) offering a variety of basic legal tasks, such as legal transcription and legal coding; legal research services and contract drafting; and patent and trademark searching and mapping as well as patent application drafting. By the end of the first decade of the twenty-first century, these LPOs were an established part of the corporate legal ecosystem.

By the second decade of the twenty-first century, secondments had become an important alternative to increasing the size of in-house legal departments.

If technology enabled companies to use outsourcing and offshoring to efficiently unbundle their production process, these same forces also created a challenge for in-house counsel in their quest to control legal spend. Since 1938, producing company documents and records in response to an adversary’s “discovery” request has been a key component of litigation in U.S. federal courts. Until the turn of the twenty-first century, responding to such requests was the province of bleary-eyed associates in large law firms manually inspecting boxes of documents in dingy warehouses. But beginning in the late 1990s, these paper records began to be replaced by electronic ones. In 2001 this trend came to a head with the collapse of Enron, which brought down the venerable accounting firm Arthur Andersen, largely on the basis of the failure to properly handle electronic records. As Mitt Regan and Palmer Heenan report, “The complexity and expense of electronic discovery has led a large number of firms to rely on e-discovery vendors and information technology specialty companies as key members of litigation teams.” The result has been the creation of a cottage industry of technology companies and specialty firms creating software to help companies store, categorize, and retrieve electronics records. Like LPOs, these “alternative service providers” are now a key part of the corporate legal ecosystem.

ALSP 2.2: Temporary staffing

The internet revolution and the imperatives of cost control also brought about the emergence of flexible staffing options. For decades, companies have been turning to temporary and contract workers to cut costs, acquire expertise, and increase flexibility. As legal budgets tightened, GCs began experimenting with similar tactics. Their first option was to utilize a resource not typically available to other parts of the company: experienced lawyers “seconded” from top law firms for little or no cost. By the second decade of the twenty-first century, secondments had become an important alternative to increasing the size of in-house legal departments—an alternative whose appeal comes in part from the fact that it blurs the boundary between law firms and clients.

In addition, however, both companies and law firms began turning to a variety of temporary staffing companies to hire contract lawyers as an alternative to bringing on more permanent staff. Although some used traditional staffing companies offering lawyers as part of their suite of services, a growing number of others began turning to a new breed of providers specifically focused on legal services. Axiom is the most prominent of these law-focused offerings. Founded in 2000 as a more effective way to do secondments, Axiom quickly distinguished itself from traditional temp agencies by recruiting lawyers with blue chip credentials from top law schools and experience in leading law firms and in-house legal departments who were willing to trade income for a more flexible lifestyle. The goal was to provide clients with the same high-quality service they expected from their own lawyers and outside law firms without the high price tag associated with these “traditional” providers. Although Axiom self-consciously presented itself as an “alternative” to traditional law firms, it has also taken steps designed to blur the distinction between their model and traditional law firms by reassuring both the lawyers who worked for the company and the clients who hired them that Axiom incorporates all the best features of these traditional service providers but without the costs. Thus, Axiom boasts that it provides its lawyers “extensive professional development opportunities including mentorship, memberships to PLI [the Practising Law Institute] and other professional organizations, and an integrated network of peers just as they would at any traditional firm.”

By the 1990s, it was clear that the Big Five intended to make legal services a key part of their multidisciplinary offering.

The competitors who followed Axiom’s lead have blurred the boundary between “alternative” staffing and “traditional” law firms even further. Consider, for example, Lawyers on Demand (LOD). LOD was originally established in 2007 by the U.K. law firm Berwin Leighton Paisner (BLP) as a way of offering its clients former BLP lawyers as temporary staff as an alternative to Axiom and other staffing companies. In 2012, BLP spun out LOD as an independent entity, merging it with AdventBalance, an Australian flexible staffing company that itself was initially started by law firms—Balance Legal, started by the Australian law firm Freehills in 2008, and Advent Legal, founded the same year by Allen & Overy’s head of business development in Sydney. BLP, however, retained an 80 percent share in the new entity, which it sold in 2018 only when the firm merged with the U.S. firm Bryan Cave. Although LOD is now for the first time not affiliated with a “traditional” law firm, like Axiom, LOD has spawned a number of “virtual law firm” competitors, many of which continue to be owned and/or operated by law firms. The fact that these and other similar flexible staffing organizations are now also an established part of the legal ecosystem further blurs the boundary between these “alternative” providers and traditional law firms.

ALSP 2.3: MDPs

In addition to putting pressure on costs, the increasing integration of global markets also created a host of managerial and strategic challenges for companies. As noted by the economist Michael Spence, the disadvantage of going global is that “global supply chains are inherently more complex” and difficult to manage and control. Corporate clients therefore began seeking ways to ease such complexities—complexities that frequently involved problems at the intersection of business, strategy, finance, technology, and law. In the 1980s the Big Five accountancy networks began rebranding themselves as MDPs capable of answering this need by bringing together a variety of professionals in a single firm. (For more, see The Practice, volume 2, issue 2.)

By the 1990s, it was clear that the Big Five intended to make legal services a key part of their multidisciplinary offering. Beginning in Continental Europe and spreading to the United Kingdom, Arthur Andersen began building a legal network, subsequently described by the legal publication The Lawyer (2007) as the first step in what Andersen “hoped would be a globally dominant multidisciplinary partnership.” As they trained their sights on the United States, however, these new entrants took steps to lessen the distinction between themselves and “traditional” law firms. Thus, to minimize the appearance of conflicts of interest with their core auditing business, the four firms that had entered the U.K. legal market began to integrate their affiliated law firms under the umbrella of separately branded legal networks—Andersen Legal, Landwell, KLegal, and E&Y Law—all led by “star” lawyers recruited from top law firms. The strategy behind this shift in organization and recruiting was simple: look as much like a traditional law firm as possible. As a lawyer working at one of these legal networks succinctly explained, “if you are competing with a law firm, you’ve got to look like a law firm.” Once again, this strategy blurred the boundary between these “alternative” providers and their traditional law firm counterparts.

The empire strikes back

In sum, by the first decade of the new millennium, the corporate legal services market had already generated two generations of “alternative” providers: Cravath System law firms, as an alternative to solo practitioners and self-help, and in-house legal departments, as an alternative to “traditional” law firms, along with a variety of new “alternative” providers designed to give GCs additional leverage to reduce their use of laws firms even further. Moreover, the lines between these “alternatives” and the traditional modes of delivery to which they were explicitly or implicitly compared have always been ambiguous. Cravath System law firms utilized a variety of mechanisms—for example, touting their exclusive lawyer ownership, strong commitment to professional values, and strict norms against commercialism—to mimic the norms and practices of “independent” professionals as a means of protecting themselves from the “law factory” critique. Similarly, in-house legal departments frequently organized themselves to look and function like internal law firms, while insisting that GCs were as much “lawyer statesmen” as the private firm lawyers they sought to supplant. And the new wave of producers from LPOs to temporary staffing companies to the Big Five all argued that by employing lawyers who used to work at top law firms (as owners and managers, if not always as direct service providers), they were really just like “traditional” law firms—albeit without the huge cost structure driving corporate clients to look for “alternatives” in the first place. At the same time, as a result of the growing number of secondments to clients, captured LPOs (such as Orrick’s facility in Wheeling, West Virginia), “ancillary” businesses offering consulting and other related services (such as Arnold & Porter’s APCO Associates and Duane Morris’s nine consulting subsidiaries), and increased reliance on temporary staffing models (such as Lawyers on Demand), “traditional” law firms had adopted many of the norms and practices of the “alternative” providers with which they increasingly competed.

Few in the profession think that we are likely to see the levels of exuberant growth that the corporate legal sector enjoyed in the years before the GFC anytime soon.

Partly as a result of “Big Law’s revenge,” as Joan Williams, Aaron Platt, and Jessica Lee put it, the first few years of the new century were not kind to the newest wave of “alternative” providers. Emboldened by the wave of accounting scandals following the collapse of Enron and the resulting demise of Arthur Andersen, the organized bar moved aggressively to press governments and regulators to place severe limits on the ability of the remaining Big Four accounting firms to offer legal and other nonaudit services to their audit clients. At the same time, the booming economy that began by the second quarter of 2002 reduced the urgency for many companies to invest in “alternative” providers, which law firms were successfully able to portray as risky and lacking in quality as compared with the often similar (albeit more expensive) services being offered by law firms. As Axiom’s CEO Mark Harris lamented in a subsequent interview, “going up against century-old brands in a tradition-bound profession was tough, especially since we were targeting the large enterprise segment [with the suggestion to try] something new and untested.” Ultimately, although clients were interested and intrigued with what the ALSPs had to offer, often there was no sense of urgency to change. The global financial crisis (GFC) fundamentally shifted this dynamic.

ALSP 3.0: The GFC and the integration of law into global business solutions

In the years since the collapse of Lehman Brothers triggered the GFC, legal commentators have engaged in a fierce debate over whether this signal event heralded a fundamental paradigm shift in the corporate legal services market—one that will inevitably produce “the death of big law” if not “the end of lawyers” —or whether the GFC is more like the painful but ultimately temporary corrections that the corporate legal market endured in 2001 and 1991. Ten years out, the one thing that is clear is that it is unlikely to be either. The fact that many top firms had their most profitable year ever in 2018 underscores that we are not on the verge of “the death of big law”—although important law firms have failed, and many others have staved off failure by throwing themselves into the arms of more financially solvent firms willing to take on some (but usually in the end, not all) of their struggling partners and associates. And after declining for several years, both applications to law school and legal employment in the United States are once again on the rise—although neither has returned to pre-2008 levels. Nevertheless, few in the profession think that we are likely to see the levels of exuberant growth that the corporate legal sector enjoyed in the years before the GFC anytime soon. Instead, the large-scale forces that have been transforming the corporate legal services market before the GFC—globalization (notwithstanding the important rise of nationalism and protectionism), the acceleration in the speed and sophistication of information technology (notwithstanding important concerns over privacy and security), and the increased “blurring” of the boundaries that used to separate once-distinct products and services (notwithstanding regulatory barriers intended to protect competition and prevent the undermining of public norms)—are continuing to put pressure on all legal service providers to produce what Ron Dolin and Thomas Buley have aptly called “adaptive innovation” that responds to the demands of the new global age of more for less.

One can see this process of adaptation with respect to each of the “alternative” models that companies began turning to in the years leading up to the GFC.

From outsourcing and offshoring to nearshoring and partnerships

In the years following the GFC, the LPO industry has worked hard to overcome the skepticism with which some clients and law firms still regarded it as a result of its marginal status as an “alternative” service provider. Thus, LPO providers actively lobbied bar officials to clear ethical issues while instituting rigorous controls taken from the business world such as Six Sigma and ISO certification to reassure end users and regulators about quality, confidentiality, and security concerns. This quest for legitimacy has undoubtedly been aided by the fact that the industry is no longer composed primarily of small independently owned companies in India but increasingly consists of captured LPOs owned or under the control of multinational companies and large law firms. The fact that many of these facilities have recently been partly or completely “nearshored” to low-cost locations in the United States or Europe that are both closer to clients and perceived to be safer has made it even easier for clients and law firms to view what were once considered radical “alternatives” as a taken-for-granted part of the legal supply chain.

Partly as a result of “Big Law’s revenge,” the first few years of the new century were not kind to the newest wave of “alternative” providers.

Indeed, these now-mainstream players are finding themselves increasingly in competition with an even newer breed of technology firms, ranging from legal tech startups to established technology giants. As indicated above, there has been an explosion in the number of legal tech startups since 2008. Many of these firms are now seeking to leverage technology developments to offer some of the same services offered by LPOs.

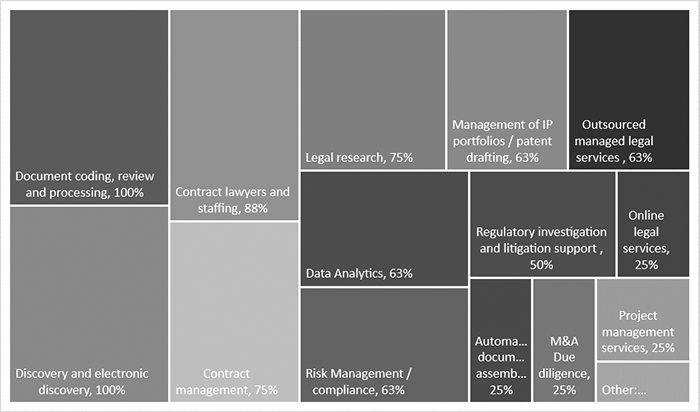

One can see this overlap by examining the descriptions in the scholarly literature and popular press of the types of services offered by legal tech companies. Exhibit 1 presents an analysis of the types of services offered by technology companies based on a review conducted by one of us for the International Bar Association of 280 academic papers and professional reports, with particular emphasis on 19 of those documents that addressed the types of services offered by technology companies in the aftermath of the GFC. The percentage of total documents citing particular legal services offered by these ALSPs provides a rough proxy of the salience of these services in the legal community. As Exhibit 1 demonstrates, the majority of the services described are similar to what was typically sent to LPOs and e-discovery companies in the period prior to the GFC. Software solutions now actively compete with labor arbitrage as the primary mechanism for both companies and law firms to reduce legal costs.

Not surprisingly, in a software-driven competition, established technology companies are likely to have a significant advantage. These companies have the kind of financial and technology resources, brand recognition, and market experience in developing and implementing software solutions that help companies and law firms feel confident that they can deliver on their promises. As a result, companies such as Thomson Reuters, LexisNexis, and Wolters Kluwer have become important players in providing software solutions to companies and law firms. But these giants are also competing with a range of legal startup companies that seek to differentiate themselves from these more established companies by focusing on new or emerging technologies in artificial intelligence and machine learning, by demonstrating greater flexibility and speed in addressing client requirements, and by offering lower costs.

All these software solutions further blur the line between “alternative” and “traditional” providers. Because software is embedded into the user’s existing infrastructure, legal tech companies are as much partners with law firms and in-house legal departments as they are substitutes for these “traditional” services. Indeed, in recent years, law firms such as Clifford Chance (through its new innovation unit Clifford Chance Applied Solutions) and Littler (through its multiple CaseSmart products) have begun developing their own software, which they use to streamline their own practices and/or sell directly to clients.

Oracle’s recent entry into the legal managed services business shows just how interconnected all these providers have become. On January 7, 2019, Oracle announced that it was launching a global “legal practice management system” targeted to law firms in the United Kingdom, with the intention of expanding to the United States and other legal markets. Oracle’s offering is meant to compete directly with similar products currently offered by Thomson Reuters by bringing, in the words of a managing partner who has been briefed on the new product, “Oracle’s cloud and AI technology into it, which makes it a rather different proposition.” Although the tools Oracle will bring to this service are new, the company’s interest in applying its expertise in enterprise management planning to the legal market is not. In 2002, Oracle teamed up with a legal tech startup to create an early version of a similar system for Clifford Chance, which the global law firm still uses today. That system has now been spun off in a separate company called Aderant, which now actively competes with Thomson Reuters—and now Oracle—in selling practice management systems to law firms. When one adds to this tangled history the fact that Oracle formally launched its new product at an event cosponsored by PwC and that in 2015 Oracle experimented with a partnership with the LPO giant Elevate Services to bring another version of managed services to the legal market, it becomes increasingly difficult to draw any sharp distinction between these various participants in the legal ecosystem.

Indeed, the day after its former partner Oracle announced its latest entry into the managed services market, Elevate announced that it had purchased Halebury, a flexible staffing company in the United Kingdom specializing in providing temporary lawyers for in-house legal departments, but which has increasingly been partnering with law firms such as Hogan Lovells. Significantly, the combined firm is now eligible to convert to an “alternative business structure” that will allow it to provide “both in-house legal teams and law firms with a 360-degree service offering spanning talent, resourcing, consulting, technology, and managed services.” Coming on the heels of its acquisition of legal AI technology and consulting firm LexPredict and contract life cycle management company Sumati Group, it is clear that Elevate is now poised to both collaborate—and compete—with “traditional” law firms and legal departments in a way that will further blur the boundary between these increasingly linked participants in the legal ecosystem.

The same can be said of UnitedLex’s recent outsourcing deals with DXC Technology and GE. Rather than simply outsourcing specific legal tasks, DXC has partnered with UnitedLex to create a unified legal team in which both organizations jointly manage the legal function—including 150 DXC lawyers becoming UnitedLex employees, and 250 UnitedLex lawyers, engineers, and project managers dedicated to supporting DXC globally. (For more on the development of so-called “managed legal services,” see “Managing to Deliver?”). The goal, according to DXC’s general counsel, is to create a “One Department mindset” providing “seamless legal services to the business client, regardless of whether the team member is from DXC or UnitedLex.” In 2018, UnitedLex entered into a similar arrangement with GE, which eventually resulted in GE’s executive counsel and director of legal support solutions joining UnitedLex as senior vice president and deputy general counsel. This deal, in turn, follows on the heels of a similar arrangement between GE and PwC in which the Big Four accounting firm hired more than 600 GE accountants, lawyers, and tax advisers who will continue to do GE’s tax work but who will also help PwC develop tax products that can be marketed to other PwC clients. As the International Tax Reporter commented: “The GE-PwC merger sets a bold new precedent for the relationship between big business and law firms” creating a “hybrid model in where the company gets a team they know and can trust, supplemented by the capacities of the Big 4.” In addition to blurring the boundaries between “traditional” internal lawyers and “outsourced” legal resources, all three of these deals underscore how in-house legal departments, LPOs, and the Big Four are all competing—and cooperating—in the same market.

The increasing prevalence and sophistication of software solutions have spurred a revolution in the way that companies manage and deploy human capital.

UnitedLex’s most recent deal with LeClairRyan further underscores this trend toward what business scholars call “cooptition”—simultaneous cooperation and competition—in the new legal services ecosystem. In June 2018 the outsourcing firm and the Am Law 200 law firm announced the creation of ULX Partners, which they described as “a strategic business platform designed to empower a ‘constellation’ of law firms with market-leading technology, new sources of capital, project and knowledge management, process innovation, and recourse management to deliver maximum value to clients and improve law firm economics.” Lauded by UnitedLex’s CEO “as the most disruptive to the practice and business of law since lawyers began billing their time,” the venture is intended to be a substitute for prior attempts at “outsourcing various law firm operations and law-firm owned hybrid staffing options,” which, according to UnitedLex (which itself spent the first 10 years of its existence selling exactly these kinds of solutions), “have largely failed to address urgent client needs and do not ensure that law firms have the right economic structure and high-impact training to evolve and thrive in a legal 2.0 environment.”

Whether ULX Partners will be able to deliver on these ambitious promises, of course, remains to be seen. The fact that LeClairRyan has been shedding partners since the announcement was made underscores that the success of this and other hybrid models is far from guaranteed. What is already clear, however, is that the line between LPOs and traditional law firms is becoming far less clear than the “alternative” label would suggest. The fact that the most recent Thomson Reuters et al. report claims that “about one-third of law firms say that they plan to establish their own ALSP affiliate within the next five years” is certain to blur this boundary even further.

The same trend can be seen in the market for “alternative” staffing arrangements.

From temporary staffing to agile work

The UnitedLex and PwC outsourcing deals highlight the extent to which both companies and law firms are looking for flexibility in the way they manage their workforce. Although outsourcing tasks—or even personnel—is one way to accomplish this goal, both in-house legal departments and law firms are increasingly looking for ways to create flexibility and encourage creativity among the lawyers and staff who remain. Once again, the software revolution is driving these “traditional” legal service providers to adopt norms and practices pioneered in the “alternative” world of technology.

The increasing prevalence and sophistication of software solutions has done more than decrease the utility of standard labor arbitrage strategies to reduce costs. It has also spurred a revolution in the way that companies manage and deploy human capital. This revolution began in 2001, when a group of software engineers issued “The Agile Manifesto” calling for software development to be redesigned around 12 principles encouraging continuous improvement, collaboration, adaptation, team efforts, and rapid delivery of valuable products and services. Today, this agile approach to project management is now widely used by leading software development companies such as Cisco, Microsoft, Spotify, and Salesforce and is increasingly being adopted by these and other companies for non-software-related projects. And, since 2008, agile project management is increasingly being applied to legal services.

A growing number of law firms are also embracing agile approaches to legal work.

Not surprisingly, in-house legal departments have been the first to embrace this new way of working, creating small, self-governing, cross-functional teams to solve problems and drive results for clients. A key part of this process is creating flexible staffing and collaborative approaches that allow teams to access expertise and technology from both inside and outside of the company. In response to this trend, companies like Axiom, which traditionally specialized in providing temporary staffing for specific projects as a substitute for either internal hiring or engaging external law firms, are increasingly entering into long-term partnerships such as Axiom’s recent five-year deal with Johnson & Johnson to provide contract management support across the company’s entire global platform. Although “labor arbitrage is an element of this second phase of disaggregated legal delivery,” the core of Axiom’s new value proposition is, as Marc Cohen wrote in a 2016 Forbes article, to “leverage technology and processes to create ‘agile’ workforces that are well-suited to the unpredictable, on-demand, and geographically disparate needs of their customers.” In addition to blurring the boundary between “in-house” and “alternative” providers, this trend also underscores the growing interdependence of “staffing” and “technology” in an agile working environment—a confluence that is likely to blur the boundary between “traditional” and “alternative” providers even further.

Although behind their counterparts in corporate legal departments, a growing number of law firms are also embracing agile approaches to legal work. Responding to both the practices of their technology clients and the increasingly urgent demand by millennials for greater flexibility and work-life balance, law firms such as Orrick are expressly embracing a version of agile work. Stating that the “one-size-fits-all approach to legal careers is outdated,” Orrick promises an “agile” work environment including “working from home, flexible work arrangements (FWA), job sharing, distinctive parental leave benefits, and even opportunities to work remotely in a location where Orrick does not have an office”—further promising that “we don’t ask you to make a choice between ‘agile’ working and partnership consideration.”

Once again, like the promises made by UnitedLex, whether either in-house legal departments or law firms will be able to create a truly agile work environment remains to be seen. What is clear, however, is that these agile work practices are further blurring the boundary between “alternative” providers like Axiom and the practices of “traditional” law firms and legal departments.

The evolution of the Big Four’s legal model since 2008 reveals a similar dynamic.

From MDPs to integrated solutions

In the years following the collapse of Arthur Andersen and the passage of the Sarbanes-Oxley Act of 2002 (SOX) and other legislation around the world seeking to limit the Big Four’s ability to deliver nonaudit services to their audit clients, the near universal consensus among professionals and pundits, as The Economist put it in a 2003 article, was that the “accountancy firms drive in the legal arena is dead.” As The Economist went on to explain, not only did this legislation prevent the Big Four’s legal arms from offering services to their “huge client base,” but “law firms have themselves become more global in recent years and many do not need the accounting giants’ international reach.” In the immediate aftermath of SOX, the Big Four appeared to confirm that they had abandoned their efforts to become important players in the market for legal services, publicly declaring that they were unwinding their legal networks.

Since the 1990s, some of the world’s leading companies have been providing integrated solutions rather than selling “standalone” products or services.

Notwithstanding these public pronouncements and some initial actions to disband their legal arms, however, over the last decade the Big Four have quietly rebuilt their legal networks to the point where they are now larger than they were in 2002. As we have documented elsewhere, by exploiting gaps in the regulatory structure that allow them to sell legal and other nonaudit services to companies that they do not audit, and taking advantage of their global reach to grow their legal practices in countries where regulatory restrictions on legal practice are either weak or nonexistent—or where regulatory reforms increasingly allow multidisciplinary practice—the Big Four legal networks now have a significant presence in every important legal market in the world with the notable exception of the United States. Nor are the legal services delivered by these networks confined to tax. Although tax-related advisory services remain an important cornerstone, the Big Four legal networks are now delivering services in a broad range of legal fields, including premium practices such as finance and M&A, and fast-growing ones such as compliance and employment law.

Most important, unlike when they entered the legal market in the 1990s, the Big Four are no longer seeking to brand themselves as “traditional” law firms by mimicking the practices of their Big Law counterparts. Instead their goal is to create a new kind of professional service that integrates law into global business solutions. Thus, rather than establishing freestanding legal networks, each of the large accountancy firms have aggressively moved to integrate their legal offerings with their other advisory services to build on their strong capabilities in technology, strategy, project management, and global service delivery. This fully integrated MDP model is now legal in the United Kingdom, where each of the Big Four have now been granted an “alternative business structure” license.

In championing this new model as an “alternative” to traditional law firms, the Big Four are following a more general trend toward “integrated solutions” in professional services. Since the 1990s, some of the world’s leading companies have been providing integrated solutions rather than selling “standalone” products or services. For example, IBM, a pioneer of this business model, increased revenues by 50 percent thanks to its Global Solutions unit. Originally IBM sold computers as integrated systems. By the mid-1980s, however, specialized firms began to supply modular components. This gave big clients, such as American Express, the buying power to lead the integration of components into a system that would solve their unique business requirements. As Andrew Davies, Tim Brady, and Michael Hobday write: “Rather than mirroring this trend towards vertical disintegration by turning IBM into a group of individual component suppliers, Louis Gerstner, IBM’s CEO, executed a strategy in 1993 to build on the firm’s broad base of vertically-integrated capabilities by focusing on the provision of complete integrated solutions for a customers’ computing and service requirements.” (For more on IBM and the development of “managed services,” see “Managing to Deliver?.”)

Technology is not the only area where the Big Four are building capacity to deliver integrated solutions.

The actions of the Big Four over the past few years make it clear that they are intent on developing a similar set of capabilities. Deloitte’s investments in legal technology are illustrative of this trend. In 2014, Deloitte purchased ATD Legal Services, one of the few providers of managed document review services in Canada. In 2016 they purchased Conduit Law, a provider of outsourced lawyers ranked by the Financial Times as one of the “Most Innovative North American Law Firms.” Most recently, Deloitte formed a strategic alliance with Kira Systems, which has been described by the company’s chief executive, Noah Waisberg, as “the largest professional services AI [artificial intelligence] deployment anywhere, period.”

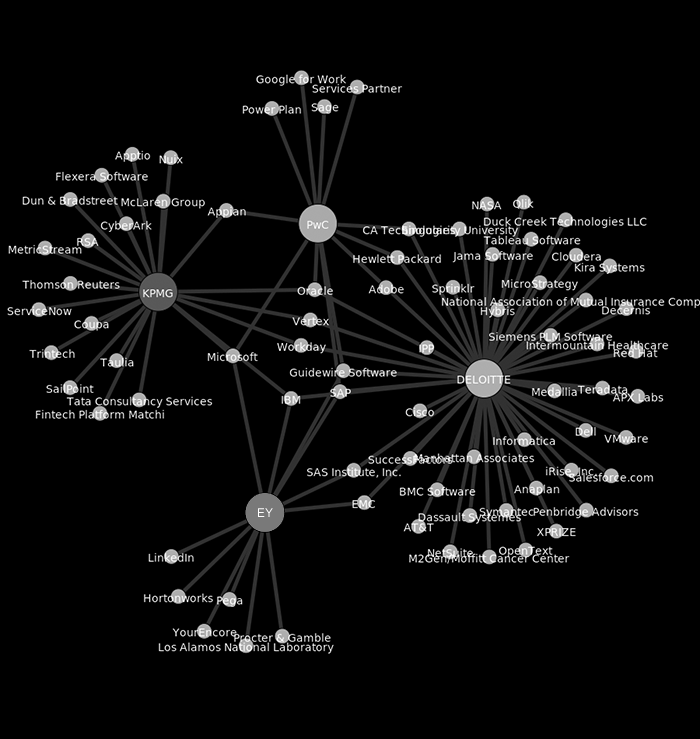

But the Big Four are investing in more than legal technology. Exhibit 2 highlights the Big Four’s multiple alliances with leading technology companies disclosed on their websites by May 2017. As Deloitte makes clear on its website, these alliances are meant to cocreate solutions to help clients solve “complex challenges […] by combining leading technology with […] time-tested business acumen and strong industry relationships.”

Nor is technology the only area where the Big Four are building capacity to deliver integrated solutions. Since 2014, the Big Four have aggressively expanded their capabilities in strategy consulting, on-demand talent models, digital applications, cybersecurity, and crisis services. All these services are increasingly relevant to global companies seeking to deal with complex problems at the intersection of law, business, strategy, and technology, such as data privacy and cybersecurity, antibribery and corruption, and safety and catastrophic risk.

At the same time, the Big Four are moving aggressively to acquire or develop similar complementary competencies in law. Thus, in 2018, Deloitte launched Legal Management Consulting designed to assist companies in helping their legal teams “keep pace with the commercial needs of the business” while assisting them “to do more with the same or fewer resources.” Deloitte followed this launch by forming a strategic alliance with U.S. immigration law firm Berry Appleman & Leiden, which will allow it to help global clients with immigration issues around the world, including in the U.S. market.

Many “traditional” law firms are responding by acquiring or creating consulting and advisory networks of their own.

The remainder of the Big Four have been equally active. Thus, PwC announced in 2017 that it was launching ILC Legal, a U.S. law firm, to help U.S. clients on international matters, as well as Flexible Legal Resources, providing flexible staffing solutions. At the same time, PwC moved to beef up its own managed legal services business by poaching Claire Hirst, a senior manager from Axiom. Hirst is expected to work closely with the two partners who head up PwC’s New Law services—partners that the accounting giant poached the year before from Radiant Law, an awarding-winning boutique law firm where they led sales and client delivery. And, in 2018, KPMG hired former King & Wood Mallesons global managing partner Stuart Fuller to launch its Legal Operations and Transformation Services (LOTS) unit, which aims to “transform the in-house legal function for a more complex future.” That same year, EY Legal took over Riverview Law, a managed legal service provider in the United Kingdom previously funded by the global law firm DLA Piper. To further expand legal services offerings globally, in 2019, EY announced an agreement with Thomson Reuters for the acquisition of Pangea3—an Indian pioneer in the LPO space that had been acquired by Thomson Reuters in 2003.

Not surprisingly, these and other similar moves have finally gotten the attention of “traditional” large law firms, most of which until recently had bought into the prevailing wisdom that the Big Four were no longer a threat to their market position after the accounting scandals in 2001, particularly in the United States, where multidisciplinary practice is still formally prohibited. The fact that the Big Four’s integrated solutions model taps into the frequent complaints by GCs that law firms do not provide commercially relevant advice has undoubtedly contributed to this response. As a recent study by LexisNexis, in partnership with the Cambridge Judge Business School at University of Cambridge, underscores, although “clients repeatedly emphasized that they look to law firms for solutions to business problems, … forty percent noted that senior partners of their law firms appeared to lack more than a basic knowledge of their business […] and seventy-five percent mentioned they get little help from law firms when analyzing the complex portfolio of legal work given to them.” Such sentiments are likely to continue to raise the visibility of the Big Four’s legal offerings, which already occupy four of the top five spots in a recent ranking of “alternative service providers” among global GCs.

But these same trends underscore how misleading it is to characterize the Big Four’s integrated solutions model as an “alternative” to traditional legal services. Just as we are seeing traditional outsourcing and flexible staffing companies blur the boundaries between “alternative” and “traditional” legal services to meet the changing needs of global clients, the Big Four are building their capacity to provide integrated solutions by acquiring, and partnering with, other legal service providers, including traditional law firms and legal departments. For example, in 2019, Deloitte Legal established an alliance with employment law firm Epstein Becker Green with the goal—as boldly stated by Piet Hein Meeter, global managing director of Deloitte Legal—of “bridg[ing] a critical gap in the U.S. market to support clients who require a global solution for employment law and workforce management issues.” As PwC’s former chairman Dennis Nally succinctly put it: “The idea that as a professional services network we would house all of those capabilities within PwC is a model that’s really outdated.”

It is far from certain that any of the participants in this increasingly complex ecosystem—let alone all of them— will be able to deliver on their promise of innovation and change.

At the same time, many “traditional” law firms are responding by acquiring or creating consulting and advisory networks designed to build multidisciplinary capacity of their own. For example, in 2015, DLA Piper International entered the field of corporate and financial advisory services by incorporating Noble Street Limited in the United Kingdom. While Noble Street and DLA Piper “operate as separate businesses,” the focus is on cross-selling financial and consulting services to the law firm’s strong international client base. The launch of Noble Street follows a wave of international law firms entering the corporate advisory field since 2010, thus acknowledging clients’ demand for external legal advisers who “understand their issues, focus on delivering solutions to their challenges and share the risks with them”—as boldly claimed by the law firm Bird & Bird on the occasion of the creation of a joint venture with ASE Consulting.

The fact that several of the largest and most influential global law firms are now advertising themselves in ways that are indistinguishable from the Big Four’s self-presentation is just one more example of the kind of “adaptive innovation” that at least some big law firms are using to respond to the challenges of the new corporate ecosystem. As Dolin and Buley argue, even in an age of increasing disruption from “alternative” providers, traditional law firms continue to offer several important advantages in the marketplace. Specifically, Dolin and Buley point out that large law firms continue to serve an important purpose in providing the kind of specialized services and flexible capacity that led to the original success of the Cravath System, as well as the kind of reputational bonding that mitigates search and monitoring costs, particularly in high-stakes matters. Given these advantages, it is not surprising, as Dolin and Buley predict, that we “see Big Law starting to incorporate disruptive methodologies and migrate their [virtual practice rules] to adapt to changing market demands such as efficiency and evidence-based analysis.”

Whether or not these efforts are successful, they underscore that the move toward an integrated solutions model is no longer an “alternative”—and therefore marginal—part of the legal ecosystem. Instead, it is increasingly clear that in 2019 and beyond, the entire legal ecosystem, including global multidisciplinary professional service firms, established and startup legal technology companies, international legal talent platforms, top legal process outsourcers, in-house legal departments, and many leading law firms, are all focusing their growth strategies on the development of integrated solution platforms that will allow them to increase the value of their legal services. The fact that a growing number of companies now have “legal operations specialists” whose express charge is to drive greater efficiency and rationality in the corporate legal services market—and that these specialists are now coming together, along with a variety of innovation professionals from law firms and “alternative” providers, in the Corporate Legal Operations Consortium (CLOC) to share best practices and create common standards—will undoubtedly accelerate this trend even further. (For more on these legal operations specialists, see “Everyone’s a Law Company.”)

To be sure, it is far from certain that any of the participants in this increasingly complex ecosystem—let alone all of them— will be able to deliver on their promise of innovation and change. As a subtitle of a 2018 report on “The State of Law Firm Innovation” indicates, “A recent survey shows law firms understand the importance of innovation but are not supporting it enough.” Those attempting to move from “innovation” to a fully integrated solutions model for the delivery of corporate legal services are likely to find the task even more challenging. As we have suggested previously, the Big Four continue to face important challenges in successfully deploying this model in their core tax and consulting businesses, challenges that raise legitimate questions about whether they will be able to translate whatever they have learned in those fields to the even more complex and regulated terrain of the market for corporate legal services. And while CLOC has made great strides, as Nicholas Bruch notes, much of the organization’s promise to rationalize the legal services market remains unfulfilled. Indeed, IBM’s recent problems internally adapting the digital transformation that it espouses for its clients underscores just how difficult it is even for a company formally committed to the integrated solutions model to adopt it fully.

A growing number of companies now have “legal operations specialists” whose express charge is to drive greater efficiency and rationality in the corporate legal services market.

Nevertheless, even if no legal service provider—whether “traditional” or “alternative”—is able to completely transform itself into an integrated solutions provider, the trends documented in this article are already making this approach to delivering legal services an increasingly important part of the ecosystem. We therefore conclude with a few thoughts about what this evolution might mean for traditional understandings of legal education, legal regulation, and the rule of law.

A new framework

In a prescient article published in 2002, the American legal scholar Robert Eli Rosen hypothesized that changes in the corporate market for legal services were turning both in-house counsel and outside firms into just another “consultant” whose primary task is to integrate legal knowledge into cross-functional teams to better achieve business objectives. The movement toward an “integrated solutions” model of the corporate legal ecosystem described in this article will undoubtedly further accelerate this trend. Moreover, it is also clear that this ecosystem involves more than just the “traditional” legal service providers Rosen envisioned—and, indeed, more than just lawyers. And yet, our current tools for understanding this ecosystem divide the world not only between “traditional” and “alternative” legal service providers but even more insidiously between “lawyers” and “nonlawyers.”

This framework obscures key challenges that the integration of law into global business solutions poses for core aspects of the “traditional” model of legal services that will not—and should not—be fully disrupted. Although artificial intelligence and machine learning will surely replace some legal jobs, the delivery of corporate legal services is likely to remain a human capital intensive endeavor for the foreseeable future. But these humans must be taught to work effectively with new technologies, in environments where lawyers and other professionals and knowledge workers (whom we should stop calling “nonlawyers”) must learn to collaborate effectively to deliver value to increasingly sophisticated and cost-conscious clients. To focus only on lawyers for the moment, this will require law schools to teach a broad range of “complementary competencies”—technology and data fluency, business literacy, cross-cultural adaptability—along with core legal knowledge and skills to their graduates. Similarly, regulators must move beyond categorical imperatives and blanket invocations of “core values” rhetoric to create “evidence-based regulation” that actually examines the merits of both “traditional” and “alternative” delivery models—and the growing number of hybrid models that incorporate elements of both.

It is clear this ecosystem involves more than just the “traditional” legal service providers Rosen envisioned—and, indeed, more than just lawyers.

But this does not mean that the “core values” of the legal system should be abandoned entirely. To the contrary, in an era in which the rule of law is under increasing threat around the world—including in the Global North, where allegiance to law and legal institutions has always been presumed robust—it is imperative that we cultivate a legal ecosystem that encourages powerful global companies not only do what is “legal” but what in the end is fundamentally “right,” as Ben W. Heineman Jr. has put it, particularly in a world in which these private actors exert as much, if not more, influence as public governments on a wide range of issues at the heart of human flourishing. If we are not ready to fully deregulate the ride-hailing market in response to disruptive companies like Uber and Lift, we certainly should not leave the predictability, fairness, and individual rights at the heart of the rule of law solely to market forces.

Needless to say, these are large and difficult issues far beyond the scope of this article. Instead, we end with the modest hope that our analysis will contribute to a new framework for addressing these vital questions. A framework in which we stop viewing the new participants who are reshaping the market for corporate legal services as “alternatives” to some mythical “golden age” when “traditional” law firms defined the epitome of service and professionalism. A framework, we hope, in which every legal service provider will be evaluated on their ability to contribute to the creation of real solutions for clients, while also understanding their obligation to help preserve the core values of the rule of law that create the infrastructure that makes every solution, private or public, possible.

David B. Wilkins is the Lester Kissel Professor of Law, vice dean for Global Initiatives on the Legal Profession, and faculty director of the Harvard Law School Center on the Legal Profession.

Maria José Esteban is a Ramon Llull Contracted Doctoral Professor and a lecturer of business law in the Department of Law at ESADE, and senior research fellow and codirector (along with Professor Wilkins) of the Big 4 Project at the Harvard Law School Center on the Legal Profession.