The interest of the Big Four accounting firms in pursuing the legal markets, and their progress in doing so, is well documented in David B. Wilkins and Maria Esteban Ferrer’s 2018 report, “The Integration of Law into Global Business Solutions: The Rise, Transformation, and Potential Future of the Big Four Accountancy Networks in the Global Legal Services Market” (Law and Social Inquiry, Volume 43, Issue 3). While the Big Four (or Big Five) have been threatening entry into the legal market since the late ’90s, they have been quietly adding capability, which now places their law practices in more than 85 countries with a legal workforce of more than 10,000 attorneys. In addition, Big Four practices have been recognized by major ranking services such as Chambers, The Legal 500, Best Lawyers, and the Financial Times.

This raises the question of how the largest law firms have decided to respond to this potential threat to their businesses, which have long been protected by regulatory rules worldwide. Over the past five years, there have been numerous press announcements of new consultancies formed and positions created by these firms beyond the practice of law that include new types of professionals, and one could conclude that they are coherently pursuing new strategic directions.

The Big Four have been quietly adding capability, which now places their law practices in more than 85 countries with a legal workforce of more than 10,000 attorneys.

A few examples: In 2015 DLA Piper launched Noble Street, a new corporate advisory arm of the firm “focused on financing, corporate and M&A activities within the media, entertainment, technology and sports sectors.” In 2017 Hogan Lovells began offering consulting services for its clients in the financial services sector after bringing aboard a former director from PricewaterhouseCoopers’ own regulatory consulting practice. The following year, in 2018 MinterEllison elected a high-ranking partner at Ernst & Young as its CEO. In 2019 McDermott Will & Emery acquired the health care research and advisory firm Farragut Square Group, adding talent to its health policy consulting subsidiary McDermott+Consulting. Lastly, in 2020 Paul Hastings launched its Life Sciences Consulting Group in collaboration “with the lawyers in Paul Hastings’ leading Life Sciences practice to offer clients a one-stop shop.”

To identify and understand what courses of action are now underway, I conducted in-depth interviews with leadership of Global 100 firms from January through October 2020 to determine their perception of the seriousness of this threat and the corresponding responses taken by these firms. I interviewed global chairs, managing partners, chief operating officers, and the heads of global strategy both in person and telephonically with 20 firms providing a fairly representative spectrum of the types of firms within the Global 100. I chose not to use surveys, which are of limited use when attempting to understand strategic thinking, purpose of actions, and intent of changes undertaken to capitalize on market opportunity or defend existing market positions. Among the key themes discussed in every interview were each firm’s understanding of the threat, the degree and timing of potential impact, and the changes (if any) the firm was planning to make to adjust to the newer market influences on their business.

Summary of findings

The firms interviewed are largely pursuing three fundamental strategies:

- Not changing operation or focus

- Establishing complementary working relationships with the Big Four

- Transforming the firm to provide multiprofessional integrated solutions

The majority of the firms interviewed operating in 10 countries or fewer are taking no action as a result of Big Four competition. Either these firms have fully evaluated the threat and concluded that they are not competitive due to the type of work they perform, or they have not seriously conducted a firmwide evaluation of the threats, although individual concerns were often expressed.

The most targeted practice by the Big Four was quite understandably the tax practice.

Not surprisingly, we found that firms with a large geographic presence (offices in more than 10 countries) are most likely to be taking concrete steps to deal with the competition they encounter from the Big Four accounting firms. Their current strategic responses are either to build complementary relationships with the Big Four and work together to satisfy client needs, or to transform their firm into a multidisciplinary professional services organization and offer an integrated set of professional services, a delivery approach similar to consultancies and now being expanded by the Big Four accounting networks with one very important addition: the inclusion of licensed attorneys. The difference in these two approaches closely aligns with the type of work the law firm is currently doing for clients. The first approach (complementary) is taken primarily by firms that have more-sophisticated practices with high-end “bet the company” legal work. The firms that are taking the second approach typically have high-volume “run the company” work, which is often associated with newer entrants in the market.

Statistical responses

In looking at the entirety of the responses of all firms, a relatively small number of firms had a good grasp of the Big Four’s activities, with little more than a third of those interviewed having a high degree of familiarity with the activity of the accounting firms. Just less than half of the firms were casually aware of the Big Four presence (primarily outside the United States), and less than a quarter had virtually no knowledge of their participation in legal markets. Not surprisingly, the same firms with a high degree of familiarity also expected a significant impact on their own business, while a slightly larger portion of firms concluded that there would be low to no impact on their business. Half of the firms observed that competition from the Big Four was here today, and the other half believed that any impact would be more than five years in the future. About a third of the firms in the sample have already experienced Big Four competition, but the majority did not have recent experience. This finding was supported by the fact that half of the firms didn’t know if they had lost business because their partners don’t report competitive losses, even if they are locally known.

Often the experience with Big Four competition is different in each geographic region, with the majority of competitive reporting coming from Europe. Asia/Pacific was the second most mentioned region. In terms of practice-area impact, the most targeted practice by the Big Four was quite understandably the tax practice, followed by compliance, regulatory, immigration, and general corporate work including M&A.

Strategic choices

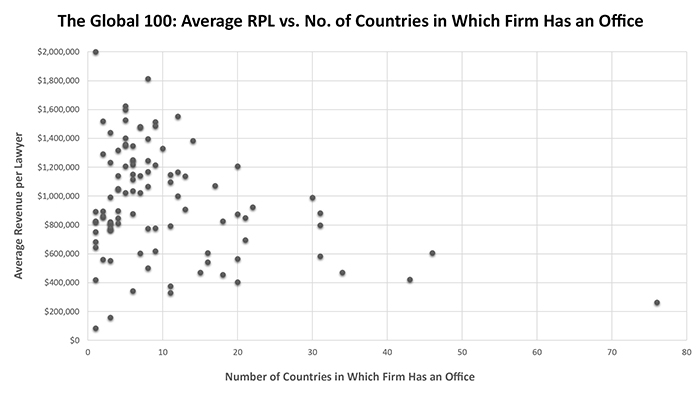

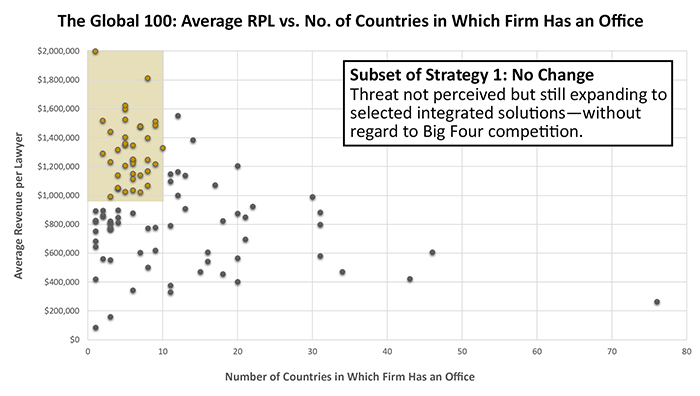

Further market segmentation of the Global 100 firms, beyond their total revenues, is helpful in understanding the logic behind the strategic choices these firms are making. It is quite logical that firms with a broad global footprint have experienced Big Four competition, so one primary factor to differentiate firms is the number of countries in which they have a presence. The second pertinent characteristic of a firm relative to the exposure to Big Four competition is the sophistication of the work they are doing, since it is conventional thought that the Big Four entry point into the legal market is commodity work. While sophistication of work is often a contentious topic of discussion with any partner or group, the client’s viewpoint is useful. Clients pay for value, and the amount they pay for high-value work can be associated with the revenue per lawyer (RPL) of a firm.

A relatively small number of firms had a good grasp of the Big Four’s activities.

Of course, this is not a perfect measure, and differences in productivity and geographic regional pricing will impact this number, but it is an easy measure to obtain from the American Lawyer’s Global 100 report and provides a reasonable proxy for the sophistication of work any firm is doing. Building a matrix of RPL versus number of countries with offices provides the scatter plot in Figure A. For reference, the average RPL in the 2020 Global 100 report is approximately $975,000. (For more on market segmentation of elite law firms using these types of matrixes, see my previous article “Postrecession Strategies.”)

Figure A

NOTE: The “Revenue per Lawyer” axis has been capped at $2 million in these charts to maintain readable scale. All charts are derived from ALM Intelligence data.

To provide a graphical view into the logic behind the strategic choices firms are making, this matrix allows us to position firms on the strategic playing field. Without giving away anything regarding the identities of my interviewees, that field includes firms like Wachtell, Lipton, Rosen & Katz, with the highest RPL ($3.3M) and a relatively small number of countries with offices (one); firms like Dentons, with a relatively low RPL ($264,000) and the highest number of country offices (78); and everywhere in between. These extremes demonstrate the range of firms in the Global 100.

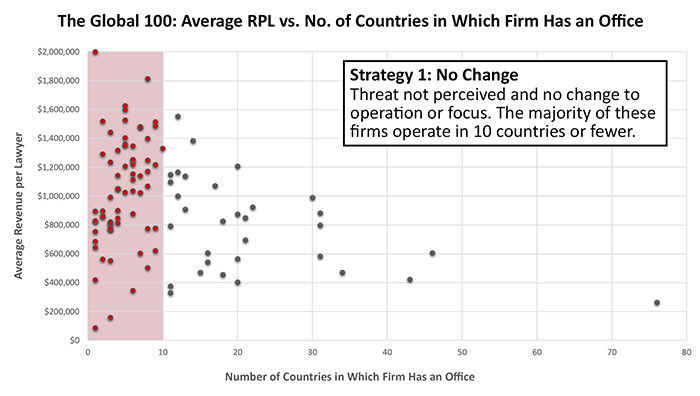

Strategy 1: Not changing operation or focus

The majority of the firms interviewed have chosen to make no changes in their operation due to Big Four presence or competition. The majority of the firms who have chosen to make no changes—more than three-quarters—have physical locations in 10 countries or fewer. In some cases there appears to have been a careful analysis of the competition the Big Four presents, and an affirmative decision was made to take no action because the accountancies do not represent a meaningful threat in the near future. In other cases, little or no analysis has been done and firms are ignoring the threat of new competition, although some of the interviewees expressed concern over the lack of critical assessment.

Figure B

A few representative quotes from these firms help illuminate their thinking:

- “The Big Four are not true competitors for us.”

- “We have a moat around our castle via the ABA.”

- “We are moving upstream, so we shouldn’t see any competition from them.”

- “If we built a new strategic plan today, competing with the Big Four wouldn’t be included.”

- “We only have one partner that believes there are barbarians at the gate.”

- “Our awareness is 1-inch deep.”

- “Lack of higher-level relationships beyond the legal department is huge; the Big Four will have the inside track.”

Clearly, some firms are very concerned, and others are very confident that their market positioning will insulate them from Big Four competitive pressures. Figure B positions these firms on the matrix.

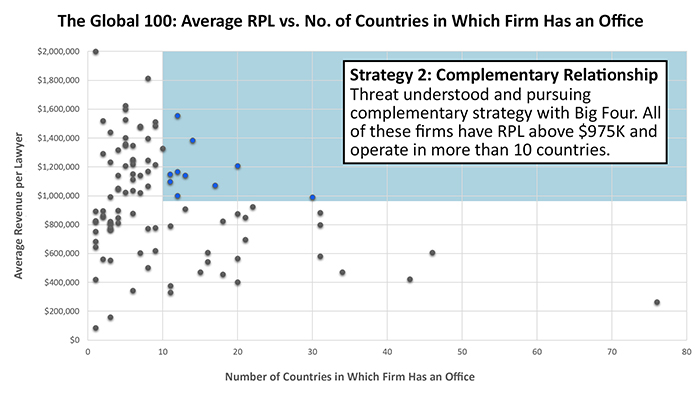

Strategy 2: Establishing complementary working relationships with the Big Four

Some firms, typically with broad global practice presence, have determined that their best approach is a complementary relationship with the Big Four rather than direct competition. These firms typically have higher-end or more-sophisticated practices that would be considered having “bet the business” rather than “run the business” capabilities. These firms often will bring in the Big Four (or other capable consulting firms) to assist a client in larger projects that require process expertise, technology capabilities, or scale that the law firm cannot provide. They are comfortable in their relationships with the client and have a high level of trust in the consultancies to respect the expertise and positioning of each firm with the clients. In other words, each organization “stays in their lane.”

Figure C

A few quotes from these firms highlight their competitive thinking:

- “We are not building a large in-house team to provide all the talent necessary and will bring others in: technology, industry experts, due diligence, etc.”

- “We really don’t view Big Four as direct competitors, but rather as additional resources we can bring to the client. The Big Four are worried about not having a good relationship with the GC, and we can remedy that deficiency.”

- “We have very complementary relationships, and the accounting firms have been generous with knowledge sharing, especially with technology.”

All the firms interviewed that have chosen this strategic approach have offices in more than 10 countries and RPL greater than the Global 100 average of $975,000, as can be seen in Figure C. To be clear, not every firm interviewed that resides within this shaded area is taking this approach, but every firm taking this strategy fits within this boundary.

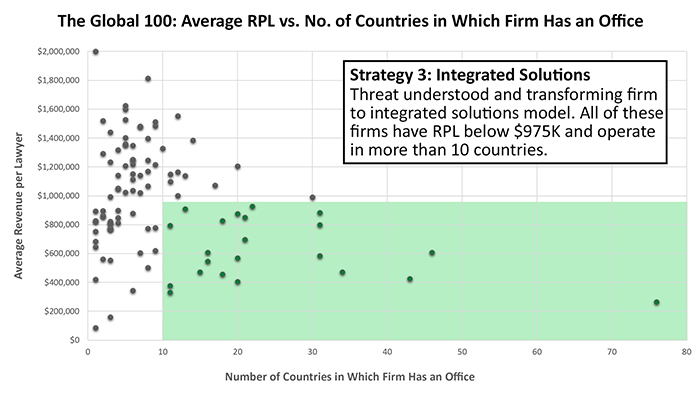

Strategy 3: Transforming the firm to provide multiprofessional integrated solutions

The final cohort are firms with a broad geographic presence that typically have lower RPL, with a profile of “run the business” work for clients. They plan to expand their professional practice offerings to better compete, which often means hiring billable professionals who are not lawyers to deliver integrated solutions. These firms are adding new project managers, client managers, industry consultants, technology experts, and data scientists to build out a fully capable delivery team. It is important to distinguish between an “integrated solutions” approach and simply providing multidisciplinary practice expertise. With an integrated solutions approach, the law firm is the organization with the sole contractual responsibility to deliver a solution and solve a problem, much like a general contractor on a construction project. All the professionals and activities are procured, coordinated, and managed by the prime contractor (in this case, the law firm). On these teams, lawyers’ time can often be 10 percent or less of the billable project work. This contrasts with a more typical approach where the law firm may work with other professionals, but the client is the systems integrator. These firms are providing integrated teams because in their field of practice, the lawyers are typically the first ones called by a client to help, and rather than allow downstream implementation work to be captured by others, they perform that work with their own professionals, supervised and monitored by the experts who built the original plans and made the recommendations.

Figure D

These firms are also hiring from the Big Four and other consultancies to immediately gain access to the unique skills required for successful delivery in this model. Importantly, engagements of this type also allow new business relationships to be developed outside the legal departments (typically an operational line of business executives) where the implementation/operational responsibility resides within the client organization. Many of these firms also recognize that new partner skills are required to deliver integrated practice offerings and have identified project management, client management, and solution selling as critical skills for successful partners when offering an integrated solutions approach.

The following quotes illustrate the thinking of these firms:

- “We have lost good partners to Big Four. They will move up the value chain (no question) and eat our lunch.”

- “We now offer consulting capabilities, specifically on regulatory issues in banks and financial institutions. We are building advance solutions using consultants, lawyers, project managers, lower-cost lawyers, and technology.”

- “In the United States, the ABA is not doing law firms any favors with Rule 5.4 because they are not learning how to compete with integrated solutions being offered by the Big Four and other consultancies.”

- “We need partners who are not lawyers to compete.”

- “Law firms who partner with the Big Four risk losing the relationship. We now have access to new buyers: operations/line of business executives. This is where the money is.”

Figure D (above) shows the positioning of these firms.

One additional strategic observation

One additional strategic approach had nothing to do with the Big Four entering the legal marketplace. These firms, with a high RPL and operating in a limited global footprint, have decided to build fully integrated, multiprofessional delivery teams because they sensed a client need combined with a business opportunity. Typically these practices are focused on a single practice area (like regulatory compliance) or industry and have a global delivery mission. These firms typically begin with one focused area of practice where they have current expertise and fully expect to expand this model to other practices over time. At this point these are not intended to be pilots but an expansion of their ability to provide clients a more complete set of professional services with multiple practices. This model is similar to the integrated practice approach described in strategy 3, where the client relies on the law firm to provide all the professional expertise necessary to solve their problems and take operational measures to implement recommendations. These firms are depicted in Figure E.

Figure E

Implications

There are two sets of implications one can draw from all this. The first contains the new questions that arise from this research. Namely, what subsequent research might best complement this analysis? What types of professionals are helping to shape these strategies in law firms and in the Big Four? How should we think about international exposure and its impact on law firm strategy? How do the strategic responses to the Big Four among elite global law firms compare with the responses of smaller, more regional firms?

No matter which strategy a firm chooses to pursue, all come with inherent risks and rewards that must be balanced with the benefit of their partners in mind.

However, perhaps the most significant question is the impact this has on the profession itself. Throughout the research process it also became clear that these changes in the legal marketplace will also provide different career opportunities and experiences for lawyers. Working on a very large team of professionals in which the legal expertise is but one element of the services necessary to help the client—whether it is primarily a law firm, an accountancy, or a consulting firm—is an entirely different experience from the typical “big law” life. In discussions with a former senior partner of a large firm, now at one of the Big Four, he described his experience as “refreshing” (perhaps because his objectives are now revenues, not hours and rates). “At the accounting firm I have a higher level of contact with the client, and the client focus is intense. My expertise and knowledge base has expanded dramatically because of exposure to an extraordinary number of experts that are part of the team … we have over 200,000 professionals at this firm. The teamwork is much more institutionalized, significantly helping out the younger professionals because they aren’t reliant on one or two partners for their mentoring. Also, upward mobility seems greater because the partners retire much earlier than in law firms, opening up opportunities for rising stars.”

Not everyone will have such a delightful experience, but there is no question that the environment and opportunities could be very different as this delivery model of integrated solutions expands.

The second set of implications relates to what is happening on the ground operationally—what steps elite law firms are and are not taking in response to the Big Four movement in the legal market. No matter which strategy a firm chooses to pursue, all come with inherent risks and rewards that must be balanced with the benefit of their partners in mind. Those pursuing a partnering strategy with other entities must take into consideration the risk of potentially subverting their client relationships by introducing new (and highly competent) strategic advisors to their clients, or perhaps losing some of their best professionals to enticing offers from their new business partners. Firms that choose to remake their businesses into an integrated solutions firm may be underestimating the effort of the transformation process, both technical and cultural, required to “cross the chasm” (per Geoffrey Moore, author of Crossing the Chasm). The firms who have evaluated (no matter how rigorous or trivial the evaluation may have been) the Big Four threats and determined that no threat exists also must be cognizant that there is a vast corporate history of organizations underestimating new competitors. Lastly, those who have failed to recognize or acknowledge a changing legal marketplace and have made no strategic adjustments may find themselves in an unfamiliar world. Like the cartoon character Mr. Magoo, who despite extreme near-sightedness and a stubborn refusal to admit any problems gets himself out of tricky situations through sheer luck, all things may work out just fine. Or not.

The most concerning observation is that a significant number of firms have given little or no thought to this competitive threat.

In each case, leadership should consider the question “What if we’re wrong?” If the choices made and decisions implemented are based on faulty data or an overzealous expectation of the firm’s ability to execute, what then? What is plan B? A good leadership team must not only make these critical decisions but also plan for alternatives if things don’t go as intended. To paraphrase the Prussian field marshal, no battle plan survives beyond the first contact with the enemy. Contingency plans must be in place and readily implementable. It may be that the most valuable strategic characteristic of any professional services firm is the ability to change rapidly.

Final thoughts

This research represents the actions of 20 firms within the Global 100 and thus serves as informational data for others contemplating their strategic choices. Interviews with 20 different firms could yield a different story, but the logical thinking of the firms interviewed that have given the issue serious consideration is not happenstance. The most concerning observation is that a significant number of firms have given little or no thought to this competitive threat, and many of the interviewees expressed this concern. Serious critical thinking that analyzes the situation and concludes that no changes are necessary based on their strategic analysis is admirable. Ignoring the question is also quite understandable because the actions driven by a conclusion of threat will require significant action, including the risks of making consequential operational and cultural changes. After all, if you’re unsuccessful in a transformation, it’s easy to conclude that doing nothing is preferable to failure. A difficult call, indeed.

Robert J. Couture is a senior research fellow at the Harvard Law School Center on the Legal Profession and a former executive director of McGuireWoods, a law firm headquartered in Richmond, Virginia. Questions and comments can be directed to [email protected].