This article is based on a paper that can be found on SSRN by clicking here. The data and analyses described in this article, as well as additional research relating to the role of lawyers on bank boards, are set out in greater detail in the full paper.

Banks are subject to a broader range of risks than most nonbanks, requiring their directors to possess special skills to effectively manage that risk. In “normal” times, those risks—which include credit risk, liquidity risk, and regulatory risk, among others—can affect how well a bank performs. In “turbulent” times, the impact on performance can be even greater, particularly important today in light of the two “once in a century” crises—the 2008 financial crisis and the current pandemic—that have occurred within 12 years of each other. (Note: The terms “bank” and “banks” in this article refer to institutions that are identified as financial institutions within Standard Industrial Classification (SIC) codes 6000–6999, including commercial banks, investment banks, and insurance companies.)

Effective risk management involves more than curbing downsides.

Due to risk’s effect on performance, virtually any action by a bank’s managers can be reduced to a risk decision that increases or decreases bank value. As a result, managing bank risk requires a continuous reevaluation of the problems and opportunities that affect how a bank performs. Bank managers use a range of tools to assess risk-taking and, as needed, to adjust their bank’s operations to reflect an optimal risk-and-return balance. Bank regulators, by contrast, have a more limited set of tools, primarily the adoption and implementation of risk regulation. That regulation includes rules designed to constrain excessive risk-taking (for example, heightened bank capital requirements following the 2008 financial crisis have increased a commercial bank’s equity cushion and, with it, the cost of investing in riskier assets), but often without a full understanding of how a particular bank board operates. The challenge for regulation (and regulators) is to manage a bank’s risk-taking, perhaps by reducing risk, while being flexible enough for the bank’s directors to pursue risky projects that can enhance bank value.

The three little risk managers

Bank risk regulation often focuses on managing “bad” risk—the probability of a loss that hurts bank value and the cost to manage that risk. Yet, effective risk management involves more than curbing downsides. It also facilitates taking on “good” risk—opportunities that are uncertain but may still be profitable in the future. The challenge for a bank’s managers is to find the bank’s optimal risk-and-return tradeoff.

To illustrate, recall the story of the three little pigs. The first two pigs built houses of straw and sticks, spending the extra time to play and relax. The wolf arrived, huffed and puffed, and blew the houses down, and both pigs ran to the third pig’s house for safety. The third pig used bricks, which required a great deal of time, effort, and expense. The wolf huffed and puffed again, but the brick house remained standing, and all three pigs were saved. The moral of the story—to work hard and prepare for the worst—is familiar to most of us.

Note the story’s focus on “bad” risk: the losses the two pigs suffered due to the wolf. It implies that their only alternative was to build with bricks. What the story fails to ask is what would have happened if the wolf never showed up? In that case, instead of a story about hard work, it might have been a story of waste. The first two pigs would have been smart to build only with straw and sticks, spending the extra time (and money) to pursue something more valuable. Bricks would have been unnecessary, and without the wolf, the third pig’s efforts simply would have been wasteful. Even if the pigs were aware of the wolf, the likelihood of it appearing would have been difficult to gauge. That difficulty would have been costly—the cost of underanticipating risk and later being eaten, or overanticipating risk and spending too much time, effort, and expense to build an unnecessary brick house.

Thus, the ability to assess and respond to risk is valuable. If the three pigs could accurately gauge and manage wolf-risk, they might have found a different, optimal risk-and-return tradeoff. For example, they might have used a mixture of straw, sticks, and bricks to build all three houses—sturdier than straw and sticks alone, but less expensive than using only bricks. The result: in ordinary “no wolf” times, the brick-house pig would have been better off than before, spending less on building his house, and in turbulent “wolf” times, the straw and stick pigs would have been better off as well, being more prepared for the wolf’s visit. That ability to balance risk and return—managing the downside of “bad” risk but also being flexible enough to assume “good” risk—is at the heart of an effective risk-management process.

The challenge of bank governance

Take, for example, the current requirement that a commercial bank create a specialized board committee to oversee its risk-management practices. Rule changes after the 2008 financial crisis expanded the risk-management responsibilities of a bank’s board, including new independence requirements to ensure directors fulfill their enhanced oversight function. Today, regulation requires a majority of the committee’s members to be “independent”—nonexecutive directors with limited economic ties to the bank—with at least one member experienced in identifying, assessing, and managing the risk exposures of large, complex banks.

As fiduciaries, a bank’s directors are obligated to reflect their shareholders’ interests in their decisions.

The question is the extent to which those rules are likely to improve a bank’s risk management. Regulation that focuses on a director’s independence potentially does so at the expense of his or her substantive expertise. Independent directors—precisely because they are independent—may lack the knowledge needed to be effective. After all, those who best understand how to manage a bank may also be closest to the bank and therefore lack the arm’s-length distance needed to qualify as “independent.”

Moreover, as fiduciaries, a bank’s directors are obligated to reflect their shareholders’ interests in their decisions. Shareholders have incentives to increase the risk a bank incurs—potentially gaining a substantial upside if the bank’s assets appreciate, while being exposed to limited downside due to their limited liability. Consequently, shareholders (and their boards) have an incentive to engage in what economists call “asset substitution”—substituting riskier assets for safer ones, with the expectation of higher returns. For that reason, relying on a bank’s board to manage risk, without also taking account of the board’s decision-making process, may have the unintended consequence of skewing the bank toward greater risk-taking. At the least, it calls into question whether regulating director independence is a sufficiently reliable means to manage risk.

One-size-fits-all regulation typically treats the board as a “black box,” without reflecting the give-and-take needed for informed decision-making. More to the point, bank regulation says little about the process a bank’s board should follow to implement an effective risk-management strategy. For example, regulation does not address how a bank’s directors should collect and assess risk-related information, although that process is critical to how the bank manages risk. To that extent, board composition, and the skills directors bring to their jobs, may be as important as—perhaps more important than—director independence.

Lawyers as risk managers

Those directors’ skills may explain the precipitous rise of lawyer-directors at banks over the past two decades (1999–2017). As we describe for the first time in a recent paper on which this article is based, in 1999, only about 40 percent of banks had a lawyer on the board. Today, it is more than 70 percent, a staggering 73 percent increase in lawyer-directors. This novel evidence is based on a data set of lawyer-directors in banks that covers the period from 2000 to 2017 and includes 12,343 bank-years of observations.

What explains this shared choice among banks?

As we describe in more detail in our paper, lawyer-directors at banks are associated with efficient changes in risk management and significant increases in bank value. Most important, banks with lawyer-directors assume more risk in ordinary (noncrisis) circumstances and less risk when a crisis arises—braking and accelerating a bank’s risk-taking in ways that make the bank more valuable. Consequently, the benefits of having a lawyer-director are particularly great in banks that are weathering a financial crisis. In addition, lawyer-directors enhance the value of having other experts on the board, perhaps by facilitating communication among expert and nonexpert directors.

Lawyer-directors can help their colleagues understand legal and regulatory problems and act as a bridge between experts and nonexperts to resolve them.

As a result, and as we describe below, the rise of lawyer-directors reflects a sea change in bank governance. Stakeholders appear to value lawyer-directors who facilitate how banks manage risk and return. In the past, Ronald J. Gilson has described a lawyer as “a counselor, planner, drafter, negotiator, investigator, lobbyist, scapegoat, champion, and, most strikingly, even as a friend.” We now add to that list a lawyer’s expertise as “risk manager.”

Could the value-enhancing results be replicated by a lawyer who advises the board but is not a bank director? We think not. Lawyer-directors are more likely than outside counsel to attend board meetings and have access to information needed to advise the board properly. They may also become aware of new information at an earlier stage, enabling them to flag concerns as they arise. In particular, as we discuss below, they can assist their colleagues better to understand legal and regulatory problems and, as necessary, act as a bridge between experts and nonexperts to resolve them. Directors and managers are also more inclined to follow the advice of a colleague who shares equal responsibility for its outcome. That may be particularly true of lawyer-directors in light of the higher standards to which courts have held them.

Where are the lawyers?

Certain bank characteristics are more likely to be associated with a lawyer-director. They include banks that are underperforming, large and complex banks, banks that face greater litigation and regulatory risk, and banks whose CEO is also a director.

Banks with higher market values are more likely to have at least one lawyer-director. For instance, a 1 percent increase in value translated to a 19.7 percent increase in the likelihood of a lawyer on the board. Conversely, banks with upward trends in value were less likely to have a lawyer-director. For instance, when a bank’s value was on the rise, a 1 percent increase in that rise translated to a 13.3 percent decrease in the likelihood of having a lawyer-director. Considered together, these findings suggest that adding a lawyer to the board reflected recent underperformance by the bank that had not improved—perhaps with the expectation that the lawyer-director would address the bank’s problems and improve value. It is doubtful that higher value resulted in a lawyer-director being elected, because when there was improvement (an upward trend in bank value), lawyers became less likely to be on the board. The same dynamic may explain why banks were more likely to appoint a lawyer to their board during a crisis. Banks, for example, were 10.5 percent more likely to appoint a lawyer-director to their board during the 2008 financial crisis (in comparison with noncrisis times)—another indication that adding a lawyer-director is associated with a drop in performance, but with the goal of improving value over time.

Bank size and revenue growth, which are proxies for complexity, are also associated with having a lawyer-director. Specifically, when a bank’s size increased by 1 percent, the bank became 24.9 percent more likely to have a lawyer on the board. This suggests that the benefits of having a lawyer-director are greater when the bank is large or complex—in other words, when managing bank risk may become more difficult. Lawyer-directors were also associated with banks with higher levels of litigation. That is unsurprising in light of the special legal expertise that lawyer-directors bring to decisions about lawsuits.

Effective risk management is not simply risk reduction but rather a means to determine the bank’s optimal risk-and-return tradeoff.

Interestingly, a bank was also more likely to have a lawyer-director when the CEO served on the bank’s board. There may be several reasons for this association. CEO-directors, for example, may be more interested in including legal expertise on the board, perhaps as one means to reduce the risk of future litigation. Alternatively, the association may reflect the value of having a lawyer-director with advocacy skills when the CEO is also a director. Predictably, a CEO-director—due, in part, to his or her superior knowledge of the bank—will influence the board’s approach to risk management. The result may be a less informed risk-management process, particularly since the CEO’s view of risk is likely to affect whatever information the bank’s board receives. Lawyer-directors can help balance that influence since, being trained as advocates—to ask questions, to critically analyze opposing points of view, and to persuade others of their position—they are less inclined to defer to the CEO (or any other single source of information). Doing so is more likely to promote discussion at board meetings and a more informed decision-making process.

In short, our findings seem to suggest that lawyer-directors are special because they are associated with better risk management, resulting in an increase in bank value. As we describe next, lawyer-directors appear to be especially capable of adapting to different circumstances. Specifically, a lawyer-director is associated with efficient changes in risk that occur between when a bank is in a Financial Crisis (2007–2009) or operating as usual in Normal Times (covering all other years in our panel). (Note that all italicized terms in this article are defined in our paper.) The result is a higher market value when a lawyer is on the board.

Lawyers, bank risk, and bank value

To demonstrate the relationship among lawyer-directors, bank risk, and bank value, we examined the impact of having a lawyer-director on bank risk. We used a matching methodology, comparing the risk of banks with a lawyer-director (the “treated” banks) to the risk of a set of “control” banks that shared core characteristics with the treated banks (such as bank size, value, risk, and the ownership percentage by institutional shareholders) but did not have a lawyer-director. This methodology helps mitigate the challenge of endogeneity—the possibility that correlation could be mistaken for causation. The intuition is that comparing banks with a lawyer-director to banks that share essential, observable characteristics, but do not have a lawyer-director, decreases the likelihood of significant differences in unobservable factors that may bias our estimates.

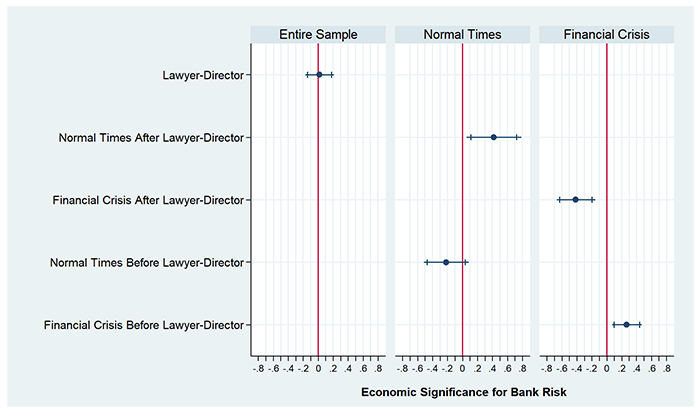

We performed this analysis for the four- and five-year periods following the initial year in which the matched, treated bank first elected a lawyer-director. For brevity, since the results for both periods were similar, Figure 1 below shows only the results for the five-year period.

This figure plots the estimates for matched panel OLS regressions of bank risk on the main interactions of dummy variables for lawyer-director, Normal Times, and Financial Crisis over a t ± 5 estimation window (where t=0 is centered on the year the bank appointed a lawyer-director). The blue circle marker denotes the coefficient estimate, and the accompanying horizontal line (with end caps) depicts 95% (90%) confidence intervals. We embed a red vertical line centered at zero to indicate statistical significance at the 5% (10%) level.

At first glance, the results in the first panel of Figure 1 are puzzling. Looking at the Entire Sample, it appears that the average effect of a lawyer-director on bank risk is insignificant in the five years after he or she joined a board. Recall, however, that effective risk management is not simply risk reduction but rather a means to determine the bank’s optimal risk-and-return tradeoff. This raises an intriguing possibility—namely, that higher and lower levels of risk under different circumstances may have canceled each other out. This could explain the statistically insignificant average effect of lawyer-directors on bank risk over the Entire Sample.

Further examination confirmed this possibility. We divided the bank data in the Entire Sample between Normal Times and Financial Crisis, as reflected in the middle and last panels of Figure 1, using a triple interaction analysis where Financial Crisis equaled one during 2007 to 2009 and Normal Times included all other years. What we found was that the insignificant average effect of lawyer-directors on bank risk over the Entire Sample (2000–2017) was attributable to the canceling-out effect of having lawyer-directors during both noncrisis and crisis periods. When it was business as usual, having a lawyer-director was more likely to be associated with an increase in risk. During the 2008 Financial Crisis, however, having a lawyer-director was more likely to correspond to a reduction in risk. Together, the two periods canceled out the lawyer-director’s overall effect on bank risk during 2000–2017. In terms of economic significance, the presence of a lawyer-director was associated with a 42 percent increase in bank risk during Normal Times, and a 41 percent decrease in bank risk during the Financial Crisis, in each case within the five-year period after a lawyer was added to the bank’s board, relative to banks without a lawyer-director.

A lawyer’s skills are more likely to matter the most when a bank’s risk-taking has gone awry.

Consequently, the results in Figure 1 suggest that lawyer-directors contribute to efficient changes in bank risk. When greater risk-taking made economic sense during Normal Times, banks with lawyer-directors were more likely to assume more risk. Conversely, when it became optimal to reduce risk during the Financial Crisis, banks with lawyer-directors were more likely to do so. As noted before, this may explain why banks with higher market values were more likely to have at least one lawyer on the board.

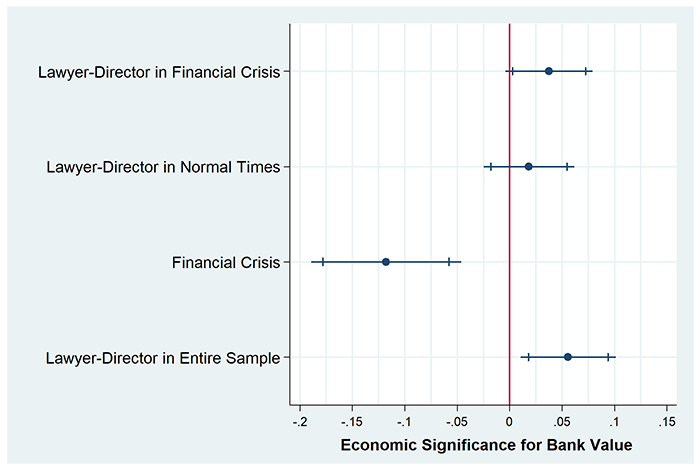

More fundamentally, having a lawyer on the board promotes (rather than only being associated with) increases in bank value. For example, as we describe in our full paper, in the first year after a lawyer-director joined a bank, the bank’s value increased by 5.7 percent relative to the sample mean. Similarly, compared with the sample mean, bank value was 3.1 percent and 3.7 percent higher for banks with a lawyer-director in the third and fifth year after the lawyer joined the board compared with the third and fifth year before he or she joined. Accordingly, adding a lawyer-director appears to contribute to higher bank value and, as described before, it does so (at least in part) through the lawyer’s contribution to the efficient management of bank risk under changing circumstances.

In that light, a lawyer’s skills are more likely to matter the most when a bank’s risk-taking has gone awry—that is, in situations when the bank needs to act swiftly to rein in excessive risk. Figure 2 below confirms this intuition by exploring the effect on bank value of having a lawyer-director during a Financial Crisis.

This figure plots the estimates for pooled panel OLS regressions of bank value, scaled by its sample average, on dummy variable interactions of lawyer-director and Financial Crisis from 2000 to 2017. The blue circle marker denotes the coefficient estimate, and the accompanying horizontal line (with end caps) depicts 95% (90%) confidence intervals. We embed a red vertical line centered at zero to indicate statistical significance at the 5% (10%) level.

Why the lawyers?

Of course, some of a lawyer’s skills spring from his or her substantive knowledge of the law. Unsurprisingly, lawyer-directors are better positioned than nonlawyers to assess and manage litigation and regulatory risk. Lawyer-directors can help weigh whether a particular litigation strategy will fail or succeed and then determine a strategy to manage that risk. This skill has become more valuable as banks have come to face greater litigation after the 2008 financial crisis. Regulatory risk is also greater after the 2008 financial crisis, with new requirements and new areas of focus continuing to emerge. This unique expertise seems to account for an important source of bank value, especially during and after the 2008 financial crisis.

Lawyer-directors are facilitators trained to ask “digestible” questions that can be understood by nonexperts.

Lawyers, however, bring more than legal knowledge to the board. Lawyers are trained to be advocates in the boardroom by promoting more-informed decision-making and minimizing the likelihood of biased “group thinking.” For example, as we described earlier, advocacy may help explain why a bank is more likely to have a lawyer-director when the CEO is on the board. Lawyer-directors may be expected to demand more evidence than other directors before making a decision. This is in line with other economic research showing that having competing sources of information can enhance the quality of the decision-making process.

Lawyer-directors are also facilitators, trained not only to ask questions but to ask “digestible” questions that can be understood by nonexperts (such as juries and witnesses). To do this, lawyers must be able to convey complex information through heuristic shortcuts, such as hypotheticals and analogies, which make information more easily accessible to a broader audience. By breaking down—and challenging—complex information, lawyer-directors are well-positioned to invigorate the board’s decision-making process.

We see this in how lawyer-directors interact with other experts on the board. Generally speaking, a bank’s value is more likely to be higher when it has directors with a diverse set of educational and professional skills (“intellectual diversity”). However, when we assess the value to a bank of different educational backgrounds (identifying directors who have law, M.B.A., M.S., or doctorate degrees), we see evidence that most of the positive value associated with intellectual diversity is tied to the effect of lawyer-directors. (The analyses of intellectual diversity are in our paper.) Part of the value may be attributable to the special skills we noted earlier, such as managing legal and regulatory risk. Part of it, however, may be tied to the lawyers’ skills as facilitators. Lawyer-directors enable banks to more fully benefit from an intellectually diverse board. They may do so by helping bridge the information gap among expert and nonexpert directors, as well as among different types of experts. The result is a board that is better able to incorporate expert and nonexpert views into its decisions, assess the risks facing the bank, and promote more-informed decision-making.

The value of thinking like a lawyer

To date, proposals to include experts on bank boards have largely focused on one kind of expertise—financial skill. This is understandable in light of concerns that many directors were unable to evaluate the subprime-mortgage assets that banks created and owned during the 2008 financial crisis. Our analysis, however, suggests that focusing only on financial skill is too narrow. Other types of expertise may be as relevant for today’s banks. In fact, legal expertise may be more relevant in light of the legal challenges banks have had to navigate.

The point is that board expertise is essential, but regulation that focuses on certain types of expertise may cause a bank to favor some skills over others that will benefit the bank even more. Moreover, as the current pandemic shows, what expertise a bank is likely to need will tend to change over time. Rather than imposing fixed requirements, encouraging a board that is composed of directors who are better able to manage through different crises over time is likely to be more valuable.

A lawyer’s ability to enhance the board’s decision-making process goes beyond technical expertise. Lawyers are trained to assess risk and, through their clients, are able to gain a broader perspective on how businesses operate and how risks can be managed.

The same is true for requirements regarding independence. A director’s substantive experience—his or her “way of thinking” about risk and risk management—may be just as important as whether he or she is independent. In that respect, the emphasis on independence is both too broad and too narrow. It is too broad because it makes it more difficult for some directors with industry-relevant expertise to join a bank’s board. It is too narrow in that it fails to promote those characteristics that are more likely to make a new director a valuable part of the board’s decision-making process. One can argue that, by restricting the universe of eligible directors, an independence requirement actually encourages a black-box approach to risk management. Narrowing the pool from whom bank directors can be selected may inadvertently promote more similarity in thinking. Consequently, regulation that treats the board as a black box—without taking account of the benefits of a diverse board in promoting informed decision-making—may result in boards that act more like a black box, paradoxically resulting in a risk-management process that is less effective.

More is needed. A lawyer’s ability to enhance the board’s decision-making process goes beyond technical expertise. Instead, it reflects a combination of the experience and practice that lawyers gain throughout their careers. Lawyers are trained to assess risk and, through their clients, are able to gain a broader perspective on how businesses operate and how risks can be managed. Those strengths are valuable for banks, reflecting the real-world expertise and practical reasoning that lawyers bring to bank boards.

Scott B. Guernsey is an assistant professor at the Haslam College of Business, University of Tennessee.

Saura Masconale is an assistant professor and director of outreach at the Center for the Philosophy of Freedom, University of Arizona.

Simone M. Sepe is a professor of law and finance at the James E. Rogers College of Law, University of Arizona, Université Toulouse 1 Capitole, and Toulouse School of Economics.

Charles K. Whitehead is the Myron C. Taylor Alumni Professor of Business Law at Cornell Law School.