Why do some states adopt lawyer regulation that protects the public while others do not? Using debates over lawyer insurance requirements and in-depth examinations of seven states with different regulatory outcomes, this article concludes that if the organized bar does not support lawyer regulation that protects the public, the public’s interests are unlikely to be represented in the regulatory process.

This article was adapted from a longer paper originally published in the Georgetown Journal of Legal Ethics (Volume 33, Issue 4, Fall 2020). You can view that paper here. All citations can be found here.

States vary in their willingness to regulate lawyers for the benefit of the public. In 48 states, lawyers are not required to maintain insurance to compensate victims of lawyer malpractice. Only two states—Idaho and Oregon—impose such a requirement.1 In virtually all states, nonlawyers are prohibited from giving legal advice in personal plight areas, even though many people cannot afford a lawyer. Only three states—Arizona, Utah, and Washington—allow licensed nonlawyers to provide such advice.2 Likewise, only two states—New York and New Jersey—impose discipline on law firms,3 even though a firm’s senior lawyers and ethical infrastructure affect lawyer conduct. Why do a few states, on some occasions, regulate the legal profession in ways that protect the public, while most others do not?

Using debates over malpractice insurance requirements, this article explores some of the reasons for the differences in the states’ willingness to regulate lawyers in ways that favor the public’s interests.

This article seeks to identify conditions under which some states will adopt more public-regarding laws—even in the face of lawyer opposition—while others are unwilling or unable to do so. To explore that question, the article looks at a single issue: how states have addressed lawyer professional liability (LPL) insurance and concerns about uninsured lawyers. While many states require doctors and other members of licensed occupations to carry liability insurance, the vast majority of U.S. jurisdictions do not require lawyers to do so. In some states, more than 40 percent of solo practitioners are uninsured.4 When uninsured lawyers make mistakes, their victims often cannot find another lawyer to represent them in a malpractice case.5 This is because many victims can only afford to sue on a contingent fee basis. If there is no insurance, there are usually no other assets available to compensate the malpractice lawyer. Consequently, victims often cannot recover from uninsured lawyers for the injuries they sustained.

In fact, most lawyers in private practice are insured.6 Yet without an insurance requirement, insured lawyers may be drawn into malpractice suits because another attorney involved in the matter may be uninsured.7 Uninsured lawyers can undermine the individual client’s trust in lawyers when a client discovers she has no meaningful recourse against an uninsured lawyer. Public trust is also undermined when the news media reports about clients who cannot recover for the harm caused by those lawyers.8

So why are some lawyers uninsured? Some lawyers fear that having insurance encourages malpractice lawsuits. For example, in a survey of more than 1,000 Nevada lawyers, more than 50 percent agreed or strongly agreed that having insurance encourages malpractice lawsuits.9 Other lawyers do not want to pay for it, often because they work part-time or are essentially retired and are not earning much from law practice. A few claim they cannot obtain coverage or cannot afford it at the price at which it is offered.10

Consequently, instead of requiring lawyers to carry LPL insurance, some states have taken halfway measures endorsed by the American Bar Association (ABA). Seven states now require uninsured lawyers to provide written disclosure of their lack of coverage to clients. Yet even if clients read these disclosures, they are unlikely to understand their implications or to feel like they can switch lawyers. Nine other states post insurance lawyers’ information on state court or judicial websites. These disclosure regimes are inadequate to alert the public that lawyers are uninsured or of the potential danger of hiring an uninsured lawyer. They are largely “symbolic reassurance” that the public is benefiting from the law.11 Most other states have not acted to protect the public from uninsured lawyers.

Using debates over malpractice insurance requirements, this article explores some of the reasons for the differences in the states’ willingness to regulate lawyers in ways that favor the public’s interests. It employs case studies to identify possibly relevant factors,12 looking closely at how seven states—Oregon, California, Idaho, Nevada, New Jersey, Texas, and Washington—have handled the regulation of uninsured lawyers. In doing so, the article discusses the political culture of the states, the historical context in which the insurance issue arose, and the role played by the state courts, the legislature, and the bar. Through these case studies, it is possible to identify key factors that seem to indicate whether states will adopt public-regarding laws.

The courts as regulators? Capacity and incentives

While state courts are ostensibly responsible for much lawyer regulation, the organized bar—and not the courts—often takes the lead. Courts are busy with their main work—deciding cases—and lawyer regulation is not at the top of their agendas.13 They lack the time and resources to do their own fact-gathering on issues relating to lawyer regulation.14 Consequently, they often rely on lawyer organizations to bring ideas to them, study issues, make recommendations, and draft language effecting changes in lawyer regulation. In some states, statutes or court rules require participation by bar organizations in this process.15 Not surprisingly, the input from bar organizations tends to favor lawyers’ interests.

It is also not surprising that lawyers’ views of regulation prevail. They not only help set the agenda, frame the issues, and make concrete proposals, but they also have many opportunities to lobby judges to advance their interests: in the courthouse, in bar association activities, and in social situations.16 Moreover, as interest group theory predicts, few organized advocates represent the public interest on issues pertaining to lawyer regulation.17 Lawyer regulation generally is not an issue on which the public’s interests are effectively communicated to the courts.

While state courts are ostensibly responsible for much lawyer regulation, the organized bar—and not the courts—often takes the lead.

At the same time, courts tend to favor the legal profession’s interests due to an “ambient bias” in favor of lawyers.18 As Dennis Jacobs, former Chief Judge of the Second Circuit Court of Appeals explained, judges are “proud of being lawyers.”19 Judges are socialized in law school to “think like a lawyer” and typically practice law for several years before entering the judiciary. They “have a high regard for our profession, its processes, its culture and values, and its judgments.”20 As a result, judges identify with lawyers and “[o]n a subconscious level when judges face a question that will affect the legal profession, judges naturally react in terms of how it will affect ‘us’ more than ‘them.’”21

The concept of “capture” also helps explain why judges often defer to the legal profession’s interests. Capture occurs because repeated interaction with a regulated industry may cause the regulator to think like the regulated industry and fail to easily conceive of other ways of approaching its problem.22 As James Kwak notes, “cultural capture” occurs through shared identity, perception of status, and social relationships.23 It can produce the same outcome as traditional regulatory capture, that is, regulatory action that serves the ends of industry.24 Moreover, “the more complex and information-intensive an issue is and the less capacity the agency has to devote to the issue, the greater the potential importance of cultural capture.”25 Some factors that should make cultural capture especially influential are a high degree of similarity between industry representatives and regulators; an industry with a notable social purpose with which regulators can identify; an industry with high social, cultural, or intellectual status; many social connections between industry and regulators; and technically complex issues for which it is not clear how the benefits of policy alternatives are shared.26

It is not difficult to see how capture occurs in the courts’ regulation of the legal profession. State supreme court justices are dependent on the legal profession to gather facts and make recommendations concerning lawyer regulation. Judges—like all people—tend to identify with other people who are a lot like them, and they tilt toward helping people who are similar.27 As between the interests of lawyers and the public, judges are more likely to identify with lawyers, especially when there are rarely opposing interest groups that are advocating for the public’s interests.28 Their judgments are distorted in ways of which they are not even aware.29

Insurance requirements vs. insurance disclosure

LPL insurance is the primary—and often the only—way to compensate victims of lawyer malpractice. Yet LPL insurance is not required in most U.S. jurisdictions, largely because the organized bar has not supported such a requirement.30 Instead, the ABA has adopted a weaker measure that only requires lawyers to make disclosures concerning their insurance coverage.31 Disclosure is an inadequate substitute for an insurance requirement. Yet even disclosure is preferable to the approach in many states, which do nothing to enable the public to identify uninsured lawyers.32

Mandatory insurance. The debate over whether lawyers should be required to carry LPL insurance first arose in the 1970s.33 At that time, legal malpractice claims increased sharply, and it became harder—and more expensive—for lawyers to obtain LPL insurance.34 State bars in California, Oregon, Washington, and Wisconsin considered whether to require all lawyers to purchase malpractice insurance from state insurance funds that would be created in an effort to lower insurance costs and protect the public from uninsured lawyers, but only Oregon adopted this approach.35 In 1977, it required its lawyers in private practice to purchase insurance from its newly created Professional Liability Fund.36 Since then, at least 18 states have considered the issue and declined to require private practitioners to carry LPL insurance.37

LPL insurance is the primary—and often the only—way to compensate victims of lawyer malpractice.

The argument in favor of requiring insurance is primarily grounded in public protection. Clients with personal plight matters—for example, personal injury, divorce, or criminal cases—are usually represented by solo and small-firm lawyers, who are the most likely to be uninsured.38 If there is no insurance, plaintiffs’ malpractice lawyers will almost never take on the malpractice case39 because even if they prevail, the malpractice lawyers will not get paid their contingent fee as there is no money to pay the judgment. Some uninsured lawyers lack other means to pay judgments against them. If they have assets, they may have moved them into a family member’s name.40 As one lawyer explained, “[I]t does not make sense to chase [uninsured] lawyers for their condos and BMWs. They will file for bankruptcy.”41

Opponents of an insurance requirement claim there is no evidence that uninsured lawyers pose a significant problem for the public.42 But in fact, there are numerous cases in which uninsured lawyers cause significant harm for which they do not compensate clients.43

Opponents also argue that the cost of an LPL insurance requirement would prevent some lawyers from practicing law.44 In fact, lawyers can purchase $100,000 per occurrence/$300,000 annual aggregate coverage in most states for $3,000 or less annually,45 although the premiums are considerably higher in a few jurisdictions and specialties.46 This level of coverage would cover most claims.47 In Oregon, where insurance costs lawyers $3,300 annually for $300,000/$300,000,48 the requirement has not reportedly created a problem for lawyers. Idaho’s recent experience requiring lawyers to carry LPL insurance also suggests that lawyers who wished to practice in the state were able to secure insurance.49

Another argument against an insurance requirement—that it would force some uninsured lawyers who provide pro bono and low-cost legal services to raise their rates or discontinue their pro bono work50—appears overstated. A survey of New Mexico uninsured lawyers revealed that fewer than 18 percent performed any pro bono work, and it was unclear how much of that work was for persons of limited means.51 For lawyers who exclusively perform pro bono work, this problem can be addressed by exempting them—as they do in Oregon and Idaho—from purchasing insurance if they work through bar-approved pro bono programs that provide insurance coverage to volunteer lawyers.52 While there may still be a small number of lawyers who serve low-income populations, charge very little, and cannot afford LPL insurance, their clients might instead be afforded some protection through a client malpractice fund.53

Finally, the claim by some opponents that an insurance requirement would enable insurance companies, and not the courts, to determine who can practice law54 is vastly overstated. There are multiple insurance companies in every state that will write insurance for solo and small-firm lawyers.55 Only a small number of uninsured lawyers report they cannot obtain coverage.56 If states require lawyers to purchase LPL insurance and those lawyers cannot obtain it, they can seek to join law firms that provide insurance. They can also work in other settings (for example, the government, in-house) where insurance coverage is not required.57 And, of course, if insurance rates were to rise precipitously or the insurance market tightens significantly, states could revisit the insurance requirement.

Opponents of an insurance requirement claim there is no evidence that uninsured lawyers pose a significant problem for the public.

Insurance disclosure. Instead of an LPL insurance requirement, many states have settled on some version of an insurance disclosure requirement. Some states began to adopt disclosure requirements in the 1990s, and in 2002 the ABA proposed an amendment to Model Rule 1.4 that would require lawyers to directly disclose to their clients whether they maintain LPL insurance.58 The proposal was later withdrawn due to bar opposition.59 In 2004 the ABA instead adopted a weaker Model Court Rule on Insurance Disclosure, which requires lawyers to disclose whether they carry LPL insurance on their annual registration forms and provides for courts to determine how to make this information available to the public.60 Twenty-three states have adopted some type of disclosure requirement. The seven states with the strongest disclosure rules require uninsured lawyers to disclose directly to their clients—in writing—that they do not carry LPL insurance (“direct disclosure”).61 Nine states require that the insurance information be posted on state bar or judicial websites (“website disclosure”).62 Seven other states adopted very weak disclosure rules, requiring lawyers to disclose whether they are insured on attorney registration forms but only making this information available to the public if they call or write to regulators—or not disclosing this information at all (“weak disclosure”).63

The arguments in favor of insurance disclosure primarily are grounded in public protection and in the view that under the rules of professional conduct, insurance coverage is a material fact about which a client should be informed before retaining a lawyer.64 Proponents also hoped it would encourage uninsured lawyers to purchase insurance.65 The evidence is inconclusive as to whether it actually causes more lawyers to become insured.66 It is also doubtful that the current disclosure regimes do much to inform clients. In direct disclosure states, clients may never read the information provided by uninsured lawyers.67 As Omri Ben-Shahar and Carl Schneider note, there is substantial evidence that “people often overlook disclosures, ignore them when they notice them, [and] treat them perfunctorily when they read them.”68 Even if clients read the disclosure, it is unlikely they fully understand the implications of lawyers being uninsured.69 Clients may assume these lawyers have other assets if they need to sue.70 Moreover, direct disclosure is typically not required until the client engages the lawyer.71 Time constraints, social norms, and power imbalances may make it difficult for a client to change course once the client has orally agreed to hire the lawyer.72

States that disclose a lawyer’s lack of insurance coverage on websites theoretically enable clients to obtain this information before they contact a lawyer, but clients are unlikely to do so. Many solo and small-firm lawyers obtain new clients through word of mouth.73 Clients are less likely to perform extensive online research if a lawyer has been personally recommended. Even clients who perform an internet search may not consider checking whether a lawyer carries LPL insurance because the public generally believes that lawyers are required to maintain insurance.74 Members of the public are also unlikely to know that they can check a state court or state bar website to learn whether a lawyer maintains LPL insurance. This information typically does not appear when a lawyer’s name is input into an internet search engine (for example, Google). Even if individuals find the information, the potential implications of a lawyer being uninsured are not explained.75 Consequently, insurance disclosure rules do not enable the public to engage in truly informed decision-making when hiring an uninsured lawyer. They are an inadequate substitute for mandatory LPL insurance.

The politics of lawyer malpractice insurance: Case studies

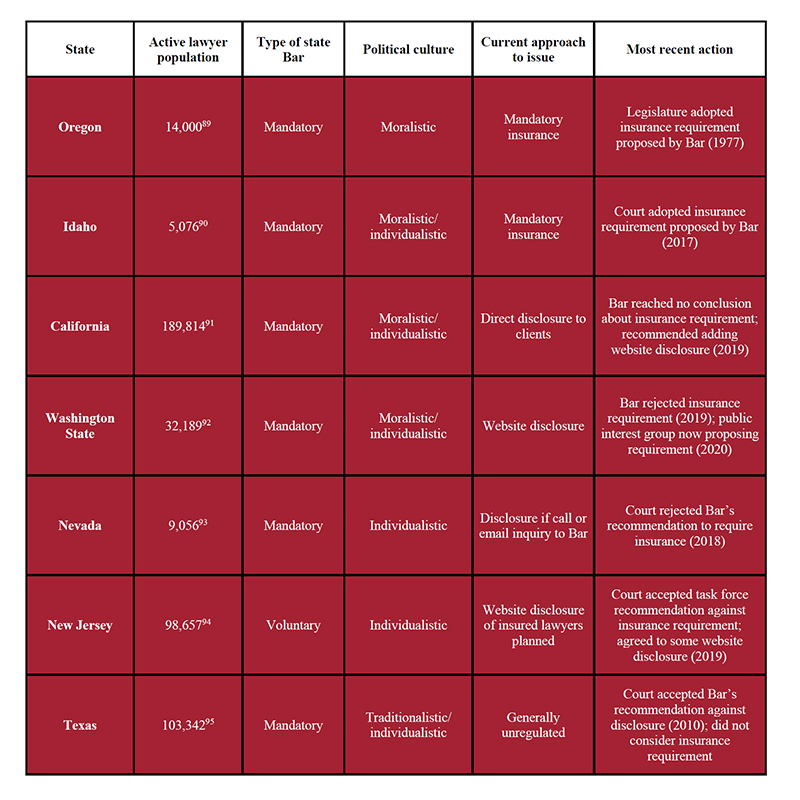

This section describes the circumstances under which some states have considered—and sometimes adopted—public-regarding laws concerning LPL insurance. It starts with Oregon, which adopted an insurance requirement more than 40 years ago.76 It then looks at six states that recently considered the insurance issue: California, Idaho, Nevada, New Jersey, Texas, and Washington. Idaho imposed an insurance requirement. California, Nevada, and Washington have disclosure requirements and recently considered requiring LPL insurance. New Jersey considered both approaches and settled upon a weak disclosure requirement. Texas never considered mandatory insurance and declined to adopt a disclosure rule.77 By shining a light on the states’ consideration of the insurance issue, we gain insight into when some states will adopt public-regarding laws and when others will instead protect lawyers’ interests.

Political culture

In looking at the LPL issue, it is worth noting that the number of Western states that have recently focused on the insurance issue may not be coincidental. States (and regions) are culturally and politically different.78 Political culture shapes government, institutions, processes, and policies in a variety of ways.79 Daniel Elazar identified three dominant cultures within the United States: moralistic, individualistic, and traditionalistic.80 Each is tied to specific areas of the country due to migration streams that carried people of different backgrounds across the country.81 In the moralistic political culture, which is found in Oregon and some other Western states, politics is viewed as a positive activity in which citizens have an obligation to participate, and, as Patrick Fisher writes, “[g]ood government is measured by the degree to which it promotes the public good.”82 Moralistic states have higher levels of political participation and are more likely to adopt political reforms and innovations.83 Individualistic political culture, which is associated with some of the Rocky Mountain, Midwest, and Mid-Atlantic states, is based on a more utilitarian view that politics should work like a marketplace and places a premium on limiting government intervention into private activities.84 Traditionalistic political culture, found mostly in the South,85 accepts the inevitability of a hierarchical society and tries to limit the role of government to maintaining the existing social order.86 While the political cultures are changing in some regions,87 they continue to help explain public policy variations among the states.88 They by no means, however, provide a complete explanation of when states will adopt public-regarding laws.

State-by-state comparison: LPL insurance requirements

Oregon: First mover on mandatory insurance

As Tom Lininger has noted, Oregon “has distinguished itself from the other forty-nine states in many areas of the law,” being the first in the nation to pass a bottle bill, establish a statewide system of land planning, permit physician-assisted suicide, and create a near-universal system of health insurance.96 It is therefore not surprising that Oregon was the first—and for many years the only—state to require lawyers to maintain LPL insurance. Nevertheless, Oregon’s decision in the 1970s to require insurance was unusual for two reasons. First, the Oregon Supreme Court did not play a significant role in the adoption of the requirement. Second, the insurance proposal was initiated by—and drew broad support from—the Oregon State Bar (OSB).

The justices of the seven-member Oregon Supreme Court are elected in nonpartisan elections to six-year terms.97 The Court claims the inherent authority to regulate lawyers under the state constitution, but it recognizes that the state legislature can also engage in lawyer regulation as long as it does not unduly burden the court’s judicial functions.98 In 1935 the legislature created the mandatory OSB as a public corporation.99 The OSB helps administer lawyer admissions and discipline in the state.100 Its Board of Governors, with the approval of the State Bar’s House of Delegates, has the statutory power to formulate rules of professional conduct for adoption by the Supreme Court.101 The Supreme Court does not “formulate” rule changes, but justices sometimes work with OSB committees that draft proposed amendments.102

The OSB’s members voted at its 1976 Annual Meeting to seek legislation authorizing the creation of a professional liability fund and to require all lawyers to purchase insurance from it.

By 1970, many LPL insurance underwriters in Oregon had pulled out of the market or were considering eliminating coverage.103 The OSB sent a questionnaire to 725 members and found that 84 percent of respondents favored a bar-sponsored plan for LPL insurance that would be mandatory for private practitioners.104 Many reported that their LPL insurance premiums had increased, and some indicated that their insurers were showing reluctance to renew coverage.105 At the OSB’s request following its 1972 Annual Meeting, the Oregon legislature amended the Oregon Bar Act in 1973 to authorize a mandatory professional liability program.106 The OSB’s members voted at its 1976 Annual Meeting to seek legislation authorizing the creation of a professional liability fund and to require all lawyers to purchase insurance from it.107 The Oregon legislature enacted such legislation in 1977.108 That same year, the OSB passed a resolution establishing the OSB Professional Liability Fund (PLF).109

The OSB viewed the benefits of mandatory insurance to include “greater protection to the clients and the public.”110 Yet, as Manuel Ramos observed, “[a]ltruism, or concern for the consumer, was not entirely behind Oregon’s decision establishing PLF.”111 By the mid-1970s, claims against lawyers had increased “dramatically,” only two commercial insurers wrote LPL coverage in Oregon, and Oregon lawyers paid “among the highest premiums in the country.”112 Oregon lawyers may have believed that the OSB’s assessment of $250 for six months—which was below the amount many lawyers were paying private insurers for LPL insurance113—would continue to be lower than if it were purchased in the commercial market. Moreover, as one member of the OSB Board of Governors observed,

[T]he importance of being covered by our own Fund cannot be overstated. It is a fund which is created by ourselves, governed by ourselves, for the protection of ourselves, and which relieves us of being bound to a commercial insurer. We now can control our own destiny regarding costs and coverage. . . .114

Idaho: Recent mandatory LPL adopter

While Idaho and Oregon share a border, they differ politically and demographically. The five-member Idaho Supreme Court is elected in nonpartisan elections for six-year terms.115 It is not known as an activist court and typically recognizes the legislature as the state’s main policymaker.116 Nevertheless, the Court claims the inherent authority to regulate admission to the legal profession. While noting that the legislature may “enact laws valid laws in aid of [judicial] functions,” it has rejected legislative efforts to relax certain bar admission requirements.117 Idaho’s legislature is part-time and rarely attempts to regulate the practice of law.118

Proposals for rule changes relating to lawyer regulation almost always come from the mandatory Idaho State Bar (ISB),119 which was formed by the state legislature in 1923.120 The ISB currently has more than 5,000 active members121 and is a “self-governing state agency” with responsibility for the administration of lawyer admission and discipline.122 Its governing body, the Board of Commissioners, has the authority to determine the requirements for admission to practice and lawyer conduct, subject to a vote of ISB members and the approval of the Supreme Court.123 The commissioners and a representative from each of the ISB’s seven district bar associations meet in October to vote on whether to circulate resolutions to the membership for a vote.124 In November the commissioners then embark on a “road show” during which they meet with each district bar association to discuss the proposed resolutions before the membership vote, which concludes in December.125

In 1993 the ISB’s membership passed a resolution directing its commissioners to study the feasibility of mandatory LPL insurance and to submit a proposal.126 The commissioners then formed a Malpractice Task Force, which in 1994 recommended the creation of a professional liability fund to which all active ISB members would be required to contribute for insurance coverage.127 The proposal met some opposition and the Task Force withdrew it to consider an opt-out provision for government lawyers, in-house counsel, and part-time lawyers.128 In 1995, the ISB’s Board of Commissioners voted to sponsor resolutions that would require lawyers to maintain LPL insurance provided through a bar-sponsored program.129 The ISB’s members rejected the resolutions by a vote of 67 to 451.130

Idaho’s legislature is part-time and rarely attempts to regulate the practice of law.

In 2005, in response to the ABA’s adoption of the Model Court Rule on Insurance Disclosure, the Board of Commissioners proposed a requirement that lawyers certify to the ISB whether they carried LPL insurance.131 The ISB members approved the resolution,132 and in 2006 the Idaho Supreme Court adopted a rule requiring lawyers to disclose to regulators whether they maintained LPL insurance.133 The information was not posted on the ISB website, but the public could contact the ISB to learn whether a lawyer was insured.134

The issue of mandatory LPL insurance arose again in late 2015 when an ISB commissioner raised the question of whether to propose a rule requiring lawyers to carry a minimum amount of LPL coverage.135 She did so because she had recently represented a client whose former lawyer committed malpractice but was uninsured.136 The commissioners researched the experiences in other states and talked with insurers.137 In October 2016 the commissioners and district bar presidents approved a resolution to require lawyers who represent private clients to submit proof of LPL coverage in the minimum amount of $100,000/$300,000.138 The proposal contemplated that lawyers would purchase LPL insurance on the open market.

A voter pamphlet mailed to ISB members in mid-October described the resolution in a single paragraph that focused on the issue of public protection. It noted that “[r]equiring attorneys to have minimum limits of professional liability insurance coverage would help to ensure the public as consumers of legal services are financially protected from attorney error.”139 During the November road show, lawyers were split on the resolution in the district meetings, but no organized opposition emerged.140 In early December, the resolution passed by a vote of 51 to 49 percent, with fewer than 25 percent of the active members voting.141 The Board of Commissioners then proposed the rule changes to the Idaho Supreme Court, which had not previously been involved in the initiative.142 The Supreme Court adopted the new rule with nonsubstantive amendments, effective January 1, 2018.143

Why was the ISB able to effect this significant rule change? The percentage of uninsured Idaho lawyers at the time of the vote was seemingly low.144 Moreover, the idea of an insurance requirement may not have seemed radical to Idaho lawyers. Idaho attorneys could obtain reciprocity to practice in Oregon without taking a bar exam145 but were required to obtain LPL insurance to be licensed there.146 In addition, prior to the road show, there was no task force report that might have attracted attention. The only media coverage of the issue during the short time between the Board of Commissioners’ October 2016 approval of the resolution and the membership’s early December vote appeared in the Idaho Bar Association’s magazine in November, which briefly described the resolution and announced that there would be a vote.147 Consequently, there was limited opportunity to mount any organized opposition before the vote. Nor was there a mechanism for disgruntled lawyers to appeal directly to the Supreme Court thereafter. The simplicity of the proposal also may have helped. Unlike the 1995 proposal, it did not involve the creation of a state professional liability fund.148 The relatively low cost of LPL insurance in Idaho also probably helped with passage.149 Finally, Idaho’s moralistic/individualistic political culture150 may have contributed to the result.

California: Efforts to move from direct disclosure to clients to insurance requirement

Like Idaho, California’s political culture is moralistic/individualistic.151 The seven justices of the California Supreme Court are initially appointed by the governor152 and are subject to retention vote.153 The Court claims the inherent and exclusive power to control lawyer admission and discipline.154 Yet it accedes to the legislature’s exercise, under its police power, of a “reasonable degree of regulation and control over the profession and the practice of law.”155 In fact, as explained below, the California legislature exercises an unusual degree of control over the State Bar.

California has a professional, full-time legislature with substantial influence over the bar.

The State Bar of California is a mandatory bar, formed in 1927 by the California legislature as an arm of the California Supreme Court.156 The requirement that lawyers belong to the State Bar is now enshrined in the state constitution.157 The State Bar has almost 190,000 active lawyer members.158 Changes to the Rules of Professional Conduct can be formulated by the State Bar Board of Trustees (seven appointed lawyers and six non-lawyer members) but must be approved by the California Supreme Court.159

California has a professional, full-time legislature with substantial influence over the bar.160 One way the legislature influences the State Bar is through the budget process; the State Bar is statutorily required to submit annually a proposed budget for legislative approval.161 For example, in 1985, due to the legislature’s displeasure with the State Bar over its political activities and its Bar-run lawyer discipline system, it declined to approve the bill needed to enable the State Bar to collect membership fees before the end of the legislative session.162 The legislature later voted in 1988 to create a new State Bar Court under the Supreme Court’s control to replace the State Bar in handling disciplinary matters.163

California’s initial consideration of how to regulate uninsured lawyers occurred in the 1970s, after many LPL insurers left the California market and the cost of insurance increased exponentially.164 In 1976, the State Bar president suggested in the California State Bar Journal the creation of a fund that would finance the actual cost of insurance, with all bar members participating in it.165 The public protection aspects of the proposal were reportedly “obscured by contests over whether it would serve all lawyers well and whether the compulsory aspects of the plan [were] legal.”166 In 1986, the legislature passed a bill requiring the State Bar to “develop rules and regulations providing that all active members of the State Bar shall possess professional liability insurance.”167 The governor vetoed that bill because it did not expressly exclude public agency attorneys and lawyers not engaged in law practice.168 In May 1987 the State Bar Board of Governors (the predecessor to the Board of Trustees) voted 16 to 4 to tentatively support a measure to require attorneys to obtain LPL insurance provided through an insurance liability fund.169 However, it soon became clear that the bill would not pass in the legislature due to opposition from local bar associations, insurers, and other constituencies, so the State Bar did not proceed with its final vote.170 As Terry Anderlini, former California State Bar president explained, “There were so many special interest groups lining up to say ‘no’ and no special interest group to push it.”171

Nevertheless, due to the legislature’s concern about uninsured lawyers, in 1992 California became the first state to require lawyers in private practice to disclose to clients in their written fee contracts whether they carried at least $100,000 of LPL insurance.172 The disclosure requirement lapsed in 2000 and was not immediately reenacted.173 After the ABA adopted its Model Court Rule on Insurance Disclosure in 2004, the State Bar, in consultation with the California Supreme Court, appointed a State Bar Insurance Disclosure Task Force to study the issue.174 In September 2007, after two public comment periods on proposed rules,175 the Task Force recommended to the Board of Governors that a lawyer’s lack of insurance should be disclosed directly to clients and should be posted on the State Bar’s website.176 At that time, five other states had direct disclosure requirements.177 By a 9-to-8 vote, the Board of Governors voted against the recommendations.178 There had been a tie, which was broken by State Bar president Sheldon Sloan, who opposed posting the insurance information online.179

The Task Force subsequently revised the proposal to drop the controversial provision about posting the insurance information on the State Bar website.180 In May 2008 the Board of Governors voted 16 to 4 to adopt a requirement that lawyers disclose directly to their clients in writing that they do not carry LPL insurance.181 At that time, State Bar president Jeff Bleich predicted that regardless of what the State Bar did, the Supreme Court was likely to adopt some kind of disclosure rule.182 He also noted that the compromise essentially reflected the old statutory system that lapsed in 2000.183 The California Supreme Court adopted the Bar’s proposed rule without change in 2009.184

In September 2017, as part of the 2018 State Bar Fee Bill, the state legislature enacted a requirement that the State Bar study LPL insurance for California lawyers, including the advisability of mandating insurance, and to report its findings by March 2019.185 Then Senator Hannah-Beth Jackson, a lawyer, introduced it.186 The Board of Trustees appointed a 17-member Malpractice Insurance Working Group composed almost entirely of lawyers.187 After studying the issue, the Working Group found that “legal malpractice insurance is readily available in California, and attorneys are able to obtain coverage at levels and with terms commensurate with their needs.”188 Nevertheless, it concluded that further study was required before a recommendation could be made about mandatory LPL insurance and suggested topics for study.189 It further recommended to the Board of Trustees that information about an attorney’s lack of insurance should be included on the State Bar’s website.190 The Board of Trustees forwarded these recommendations to the Supreme Court and the legislature.191 Whether further action will be taken remains to be seen.

Washington: Efforts to move beyond website disclosure

The Washington Supreme Court is known as an activist court192 that has broken new ground in the area of lawyer regulation. In 2012 it approved the licensing of nonlawyer legal services providers, known as Limited License Legal Technicians (LLLTs), for the benefit of the public, notwithstanding some strenuous lawyer opposition.193 Washington’s nine Supreme Court justices are elected to six-year terms in nonpartisan elections.194 The Supreme Court claims the exclusive and inherent power to admit and discipline lawyers.195 It rebuffed the legislature’s efforts to audit the Washington State Bar Association (WSBA) under state agency auditing statutes196 but has held that the legislature may enact laws that govern the entrepreneurial aspects of law practice.197 The part-time legislature198 has generally deferred to the Supreme Court in the area of lawyer regulation.199

The Washington Bar Association was originally formed in 1888 as a voluntary association.200 By 1930, some lawyers wanted a more formal structure, and in 1933 the legislature established the WSBA as a mandatory bar and a state agency.201 Today it is part of the judicial branch and administers the bar admissions process and the lawyer discipline system.202 The Board of Governors, which is the governing body of the WSBA, is elected by WSBA members, and the Board elects the president.203

Like lawyers in other states, Washington lawyers experienced high premiums and difficulty obtaining insurance coverage in the mid-1970s.204 The WSBA petitioned the Washington Supreme Court for a rule requiring all lawyers to carry LPL insurance, but then the only insurer writing such insurance in the state withdrew.205 Premiums again rose sharply in the mid-1980s, and in 1986 the WSBA began to consider establishing a professional liability fund and a bar-related insurance company.206 In 1986, the Board of Governors considered a motion to recommend to the Washington Supreme Court that it adopt an insurance program and professional liability fund, which would require Washington lawyers in private practice to participate in the fund, and provide coverage of $250,000/$250,000.207 After extended debate, the Board of Governors decided to submit the question of whether to adopt the insurance program and fund to the membership before making any recommendation to the Washington Supreme Court.208 The membership defeated the referendum by a vote of 6,971 to 1,693.209

The Washington Supreme Court is known as an activist court that has broken new ground in the area of lawyer regulation.

In 2004 Robert Welden, chair of the ABA Standing Committee on Client Protection and the WSBA’s general counsel, wrote to the Washington Supreme Court about the ABA’s Model Court Rule on Insurance Disclosure. Chief Justice Gerry Alexander responded that the Court would not consider adopting such a rule without first hearing from the WSBA.210 The WSBA began considering the issue and in July 2005 invited public comment on a proposed insurance disclosure rule.211 The Board of Governors subsequently voted 10 to 2 to recommend a disclosure rule that would require lawyers to annually certify insurance information to the WSBA and make it available on its website.212 The Washington Supreme Court adopted the rule effective July 2007.213

In 2016, after a Washington lawyer raised the issue of mandatory insurance with the WSBA’s president, the WSBA’s Board of Governors formed a working group to gather information about mandatory malpractice insurance.214 The Board was mindful of the disparity between the treatment of Washington lawyers and two other legal services providers—limited practice officers and LLLTs—who were required to carry liability insurance or to demonstrate financial responsibility to maintain their licenses.215 In September 2017, the Board of Governors formed a task force to recommend whether to proceed with a mandatory malpractice insurance proposal.216 The 17-member task force was composed predominantly of WSBA members but also included a federal judge, an insurance broker, two academics, an LLLT, and two nonlawyer representatives.217 In its March 2019 report, it recommended that the WSBA Board of Governors propose a mandatory malpractice insurance rule for consideration by the Washington Supreme Court that would require all Washington lawyers in private practice to maintain minimum insurance of $250,000/$500,000.218 In preparing its report, it had obtained assistance from ALPS, the WSBA’s endorsed professional liability provider, including estimates of the likely cost of the insurance.219 In May 2019, after the Board of Governors held a lengthy public hearing and received written comments, it rejected this recommendation by a vote of 9 to 5.220 The majority of the Board indicated they were reflecting the will of the State Bar members, who were “overwhelmingly opposed” to mandatory insurance.221

Kevin Whatley, a nonlawyer who had been the victim of legal malpractice by an uninsured lawyer, was outraged by the decision and decided to pursue the matter further.222 Whatley formed Equal Justice Washington to lobby the legislature for an LPL insurance requirement.223 In October 2019, Equal Justice Washington submitted a proposed amendment to Admission and Practice Rule 26 to the Washington Supreme Court, using the same language contained in the WSBA Task Force’s Proposal.224 In December 2019 the Court approved the suggested amendment for publication and invited public comment.225 It has received several comments, including a letter opposing the proposed amendment from the WSBA’s president.226 The WSBA proposed, instead, that the Supreme Court adopt a direct disclosure rule.227 The Court has not yet acted on either proposal.228

Nevada: Failure to move beyond limited insurance disclosure

Nevada came closer to adopting an insurance requirement, but it, too, ultimately failed. In recent years, Nevada has become one of the fastest-growing and most diverse states in the country.229 Its political culture is individualistic.230 Nevada’s seven Supreme Court justices are elected to six-year terms in nonpartisan elections.231 The court claims that “[a]uthority to admit to practice and discipline is inherent and exclusive in the courts.”232 The legislature has not challenged this assertion. Nevada’s part-time legislature, which meets every other year, is the fourth smallest in the country.233 There is a “mismatch between institutional capacity and the policy demands of a fast-growing, urban and diverse state,”234 which may help account for why the legislature has been relatively uninvolved in lawyer regulation.

In 1928 the legislature formed the mandatory State Bar of Nevada.235 After the legislature repealed the State Bar Act in 1963, the Nevada Supreme Court reconstituted the mandatory bar in 1965 as a public corporation under the supervision of the Court.236 The State Bar currently has more than 9,000 active attorneys, with more than 70 percent of Nevada lawyers living in Clark County (which includes Las Vegas).237 The State Bar is responsible for administering admissions and lawyer discipline.238 Its 15-member Board of Governors, which is composed entirely of lawyers,239 has the power to formulate rules of professional conduct, subject to approval by the Supreme Court.240 Most of the proposals for changes in lawyer regulation come from the State Bar.241

Nevada reportedly considered mandatory insurance in the 1980s,242 but no records could be located. The State Bar of Nevada again considered mandatory insurance in 2000 when a committee proposed to the Board of Governors that Nevada lawyers be required to maintain LPL insurance in the amount of $500,000.243 The Board sought input from the members and ultimately rejected the proposal in June 2000, concluding there was insufficient support among the membership.244 The Board of Governors instead appointed a new committee to explore alternatives to mandatory insurance,245 but it does not appear that the State Bar took any further action in the next few years.

After the ABA adopted its 2004 Model Court Rule on Insurance Disclosure, the Nevada State Bar Board of Governors debated the issue and concluded that they favored adoption of insurance disclosure.246 There is no indication that the Board sought the membership’s views.247 During an annual Nevada Supreme Court/Board of Governors meeting, Justice James Hardesty indicated it would be helpful if any such proposal included an analysis of the availability of malpractice insurance in Nevada.248 In its petition in support of the rule change, the State Bar reported that there were approximately 35 malpractice carriers on file with the Division of Insurance and reported anecdotal information about the cost of insurance.249 The State Bar petition to the Supreme Court asserted that disclosure “will reduce potential public harm and increase the public trust by allowing the public to make an informed decision when hiring a lawyer.”250 It further stated that the information should be available to the public but did not specify the manner in which it should be made available.251 In September 2005 the Supreme Court adopted an insurance disclosure rule that required lawyers in private practice to certify annually on their registration forms whether they maintain LPL insurance and the name and address of the carrier.252 Although the order further stated that the “information shall be public,”253 it was subsequently only made available by phone or email inquiry to the State Bar.254

Lawyer opposition from well-respected bar members contributed to the Court’s decision to effectively kill the insurance initiative.

Nevada again considered mandatory LPL insurance starting in 2017 after a prominent Las Vegas plaintiffs’ lawyer published an “open letter” to the Nevada Supreme Court and the Nevada State Bar Board of Governors in Vegas Legal Magazine.255 He decried the “hypocrisy” of not requiring lawyers to maintain liability insurance, especially when many other Nevada professionals were required to do so.256 The State Bar formed a Professional Liability Insurance Task Force composed entirely of lawyers257 to study whether lawyers “should be required to carry, or disclose whether they carry,” LPL insurance.258 The Task Force surveyed uninsured Nevada lawyers to learn more about them.259 It also conducted an “unofficial survey” of the public and found that respondents believed attorneys should maintain malpractice insurance.260 In addition, it met with LPL insurers who indicated they supported certain options being considered by the Task Force.261

The Task Force ultimately recommended that all attorneys engaged in law practice—except government and corporate counsel—carry a minimum of $250,000/$250,000 in liability insurance.262 The Board of Governors approved the proposal in November 2017 but voted to survey State Bar members to learn their views before submitting a petition to the Court.263 The survey they conducted revealed that more than 56 percent of the approximately 1,000 members who responded to the survey opposed direct disclosure, and many voiced concerns about an insurance requirement.264 Nevertheless, the Board of Governors petitioned the Supreme Court in June 2018 for a rule change to require lawyers in private practice to carry LPL insurance.265 The petition included a summary of the results of the lawyer survey.266 It also included a discussion of the likely cost of LPL insurance for uninsured Nevada practitioners, which it estimated would start low but rise after six years to an average of about $3,500 for Clark County lawyers and $3,100 for lawyers in the rest of Nevada.267

The Nevada Supreme Court then invited written comments from the bench, bar, and public, and held a public hearing.268 Written support came from a few individual lawyers and the Nevada Justice Association (the trial lawyers).269 Far more letters were written in opposition to an insurance requirement, including a letter signed by 127 members of the State Bar.270 At the public hearing in July 2018, the Court also heard “great opposition” from bar members.271 The Court subsequently rejected the proposed insurance requirement, stating that the bar had not provided sufficient data but without explaining what type of data was missing.272 Lawyer opposition from well-respected bar members contributed to the Court’s decision to effectively kill the insurance initiative.273

New Jersey: Some disclosure finally planned

The seven-member New Jersey Supreme Court has long been known for judicial activism, liberal reformist activities, and a commitment to individual and consumer rights.274 The governor nominates and appoints the Supreme Court justices, subject to confirmation by the state Senate.275 After the first seven-year term, the justice can be reappointed by the governor with the consent of the Senate, but thereafter the judge receives tenure until age 70.276 This provides the justices with a large measure of autonomy.277

The New Jersey Supreme Court claims the exclusive authority to regulate lawyers under the state Constitution,278 which vests the Court with “jurisdiction over the admission to the practice of law and the discipline of persons admitted.”279 The Court has shared its jurisdiction with the legislature “in the spirit of comity,” but it will not do so when the legislature enacts laws governing procedural matters or lawyer discipline.280 The legislature meets annually281 and occasionally passes laws affecting legal practice, but has generally steered clear of the areas of admission and discipline.282 In 1998 it passed legislation requiring physicians and podiatrists to carry malpractice insurance283 but did not impose such a requirement on lawyers.

New Jersey has no mandatory bar association to which its more than 98,000 admitted lawyers are required to belong.284 The voluntary New Jersey State Bar Association (NJSBA), formed in 1899, has more than 18,000 members, including paralegals and law students.285 The Board of Trustees, which is mostly elected by the members, manages the affairs of the NJSBA.286 It has no regulatory authority but often provides input during the rulemaking process. One indication of the Supreme Court’s view of the NJSBA’s role can be seen in Chief Justice Robert Wilentz’s statement in 1982, “I will not take any action which affects the Bar without giving you a meaningful opportunity to comment, discuss and argue.” He added, “I assure you that there are six justices determined to help me keep that vow.”287

The New Jersey Supreme Court has long been known for judicial activism, liberal reformist activities, and a commitment to individual and consumer rights.

New Jersey was a national leader in the area of attorney regulation in the 1980s and 1990s.288 It was on the forefront of efforts to protect clients with client protection funds, random audits, mandatory fee arbitration, and continuing legal education requirements.289 At times, the New Jersey Supreme Court was willing to disregard the NJSBA’s preferences in order to protect the public. For example, in 1984 it adopted a controversial rule that stated that a lawyer may not “knowingly fail to disclose to the tribunal a material fact with knowledge that the tribunal may tend to be misled by such failure.”290 The NJSBA asked the Supreme Court to withhold implementation of the rule,291 but the Court declined to do so. Similarly, in 1994 the Court sided with the New Jersey Ethics Commission’s recommendations to make lawyer discipline complaints public when a discipline complaint became formal and to eliminate private admonitions, notwithstanding the NJSBA’s “vehement opposition.”292

New Jersey’s experience with LPL insurance requirements began in 1970, when the New Jersey Supreme Court first required lawyers practicing in professional corporations to carry LPL insurance.293 In 1993 the Michels Commission, which Chief Justice Wilentz appointed to recommend changes to New Jersey’s ethics system, recommended that uninsured attorneys should be required to disclose noncoverage, but the Court rejected that recommendation without comment.294 Starting in 1997, court rules required all limited liability companies (LLCs) and limited liability partnerships (LLPs) utilized by lawyers to maintain liability insurance.295 In late 2003, as Assemblyman Jon Bramnick was poised to introduce a bill requiring New Jersey lawyers to carry LPL insurance, commentary appeared in the New Jersey Law Journal questioning whether the Court would uphold such legislation.296 The legislature never voted on the bill.297

The next year, when the ABA was considering adopting its Model Court Rule for Insurance Disclosure, the NJSBA’s Executive Director wrote a letter opposing such a rule. The main reasons were that it would “impose cumbersome and unnecessary requirements on lawyers,” and it might “open the door” to consideration of an LPL insurance requirement.298 During the 2006–2008 rules cycle, the New Jersey Supreme Court Professional Responsibility Rules Committee, which was composed of judges and lawyers, considered whether disclosure should be required but concluded it was not in a position to make a recommendation and sought more time.299 In late 2009, it recommended the formation of an ad hoc committee to gather data to consider the issues of mandatory disclosure and mandatory insurance.300

After two articles by private practitioners appeared in the New Jersey Law Journal calling for mandatory LPL insurance,301 in February 2014 the Supreme Court formed an 18-member Ad Hoc Committee on Insurance Malpractice chaired by a retired Appellate Division judge and mainly composed of lawyers.302 It included Robert Hille, the NJSBA’s designee who practices in the area of professional liability defense.303 The Committee also included one public member and an insurance industry member.304

In June 2017 the Ad Hoc Committee issued a 174-page report (plus appendices) recommending against mandatory insurance. It stated that the creation of a fund modeled on Oregon’s PLF would be “unworkable in the New Jersey marketplace.”305 It also concluded that a mandate “would be unfairly punitive” to solo and small-firm lawyers and attorneys engaged in part-time practice, presumably due to the cost.306 The Committee report further expressed concerns about insurers being able to decide who could practice law.307 Some Committee members were also concerned, based on communications with insurers, that insurers would withdraw from the market if LPL insurance were required.308 Instead of requiring lawyers to maintain insurance, the Committee recommended insurance disclosure to the Court and direct disclosure to clients.309

It is conceivable that the Supreme Court was persuaded that mandatory insurance was inappropriate in the New Jersey market because of the cost of LPL insurance there.

In November 2017 the Supreme Court invited written comments from lawyers—but not the public—on the Committee’s report.310 The New Jersey Association for Justice (the trial lawyers’ bar) wrote a letter supporting mandatory disclosure.311 Two lawyers in private practice wrote letters opposing mandatory insurance and direct disclosure.312 Hille, then the NJSBA’s president, also sent a letter stating that the NSJBA opposed both mandatory insurance and any disclosure requirement.313 He argued that NJSBA studies “show that malpractice insurance rates in New Jersey start at 33% higher than in Pennsylvania and 49% higher than in New York, due to New Jersey’s longer statute of limitations for malpractice claims and the potential of attorneys’ fee awards [to plaintiffs] under Saffer v. Willoughby.”314 At about that same time, state Senator Nicholas Scutari introduced a bill to require attorneys to carry LPL insurance that was referred to the Judiciary Committee, but no action was taken.315

These events must be viewed in the context of the 1996 decision in Saffer, in which the New Jersey Supreme Court held that a successful malpractice plaintiff could recover attorneys’ fees as compensatory damages in a legal malpractice case.316 Initially, insurers’ lawyers sought to repeal or limit the Saffer case through litigation because it increased the cost of malpractice claims.317 The NJSBA subsequently joined with the insurance industry in that fight. Since 2008 the NJSBA has lobbied in the New Jersey legislature to shorten the six-year statute of limitations for lawyer malpractice to two years and for legislative abrogation of the Saffer case.318 These efforts were supported by some other county and affinity bar associations in the state, and the insurance industry.319 They were opposed by the New Jersey Association for Justice.320

In February 2018 the New Jersey Law Journal published an editorial urging the Supreme Court to adopt the direct disclosure requirement.321 It was not until March 2019 that the Supreme Court issued a Notice to the Bar of its decision and planned next steps. The relatively brief notice stated that the Court agreed with the Task Force not to require lawyers to maintain LPL insurance.322 It then indicated that it would require insured lawyers to file with the Court certificates of insurance setting forth policy information, and would devise procedures to make that information available to consumers online.323 The Court stated that after considering the comments received on the direct disclosure proposal, it would withhold action on the recommendation until an unspecified later date.324 It has not yet published any disclosure rule.

It is conceivable that the Supreme Court was persuaded that mandatory insurance was inappropriate in the New Jersey market because of the cost of LPL insurance there.325 It is unclear, however, why this consumer-oriented court did not follow the Ad Hoc Committee’s recommendation for direct disclosure. The Court was in no hurry to form a committee to study these issues or to release its conclusions, and may have been affected by events that were playing out in the legislature. One New Jersey lawyer familiar with the matter suggested that the Court may have wanted to assure the NJSBA that it was not relentlessly pro-consumer, to the detriment of lawyers, especially when it knew that the NJSBA was still “pissed off” with the Court due to the Saffer decision.326 Or the Court may have wished to send that message to the legislature, which was considering shortening the statute of limitations for legal malpractice and statutorily abrogating Saffer. In any case, even in a state with a court that has previously adopted public-regarding laws in the face of lawyer opposition, the New Jersey Supreme Court declined to adopt strong public protection measures and has not yet promulgated a disclosure rule.

Texas: No progress on regulation

Texas differs from the other states discussed, not only in its geographic location but in its political culture, which is traditionalistic/individualistic.327 Moreover, unlike the previously examined courts, the nine-member Texas Supreme Court is elected through partisan elections.328 Money is especially important in those elections.329 Texas Supreme Court candidates raised more than $4.2 million during the 2016 elections.330 Lawyers are typically among the largest donors.331

The Supreme Court has claimed implied inherent authority to regulate the legal profession under the Texas Constitution332 and administrative authority to regulate it under the State Bar Act. It has also claimed that the authority to regulate the practice of law belongs “exclusively” to the Court.333 The part-time Texas legislature, which meets in odd-numbered years, is seriously underpaid and understaffed.334 Nevertheless, it exercises some oversight of the State Bar of Texas under the Texas Sunset Act, which provides for legislative’s review of state agencies every 12 years.335 Recent reviews have focused on improving the lawyer discipline system and State Bar governance.336

The Texas legislature formed the State Bar of Texas as a mandatory bar in 1939.337 The State Bar has more than 103,000 active members.338 It is a state agency with some responsibility for the administration of lawyer discipline.339 Its Board of Directors is composed of up to 30 lawyers who are elected for three-year terms, six persons who are not licensed attorneys, and four at-large directors appointed by the Bar president.340

In 1979, after LPL insurance premiums rose, the State Bar formed the Texas Lawyers’ Insurance Exchange as a bar-related mutual insurance company to provide lawyers with access to reasonably priced liability insurance.341 Texas lawyers, accountants, and other professionals later lobbied the state legislature in 1991 to pass the first LLP statute in the United States, which limited the vicarious liability of lawyers for tort claims so long as the LLP maintained a total of $100,000 of malpractice insurance.342 In 1993 a Texas trial lawyer published an article in Texas Lawyer calling for a requirement that all lawyers maintain professional liability insurance,343 but it does not appear that it spurred any official action.

Unlike the previously examined courts, the nine-member Texas Supreme Court is elected through partisan elections.

In 2007 Austin attorney Charles Herring Jr. wrote to the Texas Supreme Court asking it to consider forming a task force to study the 2004 ABA recommendation concerning insurance disclosure.344 He noted that a 2005 State Bar survey indicated that 63 percent of solo practitioners were uninsured.345 The Supreme Court then asked the State Bar president to consider whether Texas lawyers should be required to disclose the existence or non-existence of LPL insurance.346 In November 2007 the State Bar President appointed a Task Force on Insurance Disclosure.347 The Task Force found that 77 percent of bar members responding to a Task Force email survey opposed an insurance disclosure rule and that 65 percent of lawyers responding to a phone survey believed that lawyers should not be required to disclose.348 An April 2008 survey of the public revealed that 70 percent of respondents believed that lawyers should be required to disclose to clients whether they carry LPL insurance.349 According to one observer, in the midst of the process, the State Bar president added two anti-disclosure members to the Task Force “to kill the deal. That’s what the Bar leaders wanted.”350 In June 2008, the Task Force recommended by a vote of 6 to 5 that no insurance disclosure be required.351 The State Bar Board of Directors forwarded the Task Force’s report to the Supreme Court without making its own recommendation.352

Thereafter, the Grievance Oversight Committee (GOC), a body appointed by the Supreme Court and primarily tasked with reviewing the lawyer discipline system, spent nine months reviewing the insurance disclosure issue.353 It conferred with the Chief Disciplinary Counsel, the Commission for Lawyer Discipline, local bar leaders, bar leaders in three states that had not adopted the ABA disclosure rule, and members of the public.354 It also looked at the cost of LPL insurance and reviewed correspondence from lawyers opposed to disclosure.355 The GOC recommended in June 2009 that the Supreme Court adopt a disciplinary rule requiring disclosure if lawyers did not carry LPL insurance in the amount of $100,000/$300,000.356 This recommendation appeared two months after Elliott Naishtat, a state representative from Austin, introduced a bill providing for the promulgation of rules requiring uninsured lawyers to provide notice to clients that they are uninsured.357

The Supreme Court then asked the State Bar Board of Directors to take a position on the disclosure issue, which prompted further Bar study.358 Bar leaders held public hearings around the state, which were attended almost exclusively by lawyers.359 Once again, they found that lawyers overwhelmingly opposed the proposal.360 The Board commissioned a public opinion survey of 500 Texas residents that revealed 88 percent of respondents reported they would be less likely to hire a lawyer who did not carry LPL insurance and 64 percent believed that lawyers should be required to reveal this information.361 The Board also conducted focus groups with 37 members of the public, which revealed that 70 percent of participants initially believed that lawyers should be required to disclose, but after hearing arguments for and against disclosure requirements and further discussion, 54 percent indicated there should be disclosure.362 The focus groups were subsequently criticized, however, for the way in which they were conducted.363 Two citizens’ organizations wrote in support of a disclosure rule as did three former State Bar presidents.364 Nevertheless, in January 2010 the State Bar Board of Directors recommended by a vote of 39 to 1 against requiring disclosure.365 They further recommended that if the Supreme Court decided that disclosure should be required, it should be in an administrative rule and that the information should only be posted on the State Bar website, rather than through direct disclosure to clients.366

The Texas Supreme Court has a history of protecting lawyers, at least in the area of lawyer malpractice.

In his letter to the Supreme Court explaining the Board’s conclusion, State Bar President Roland Johnson stressed that Texas lawyers “overwhelmingly expressed their opposition to a requirement” and suggested that a disclosure requirement would confuse the public because of the intricacies of insurance.367 Johnson also emphasized that when the public was asked for things they looked for when hiring an attorney, “professional liability insurance is not even in the top 10 answers received.”368 He did not mention that the survey asked for open-ended responses and that many members of the public assume that lawyers carry insurance.369 The Johnson letter and accompanying executive summary are striking in that—apart from referencing public support for the idea—they do not mention any of the arguments in favor of insurance disclosure.

In April 2010 the Texas Supreme Court announced it would not adopt a disclosure rule.370 Chief Justice Wallace Jefferson wrote, “Having considered the State Bar’s recommendation and the materials supporting the recommendation, the Court will retain the status quo.”371 The Supreme Court noted “good arguments were presented on both sides.” It added:

Of course, we should be concerned if clients are unable to recoup sums occasioned by lawyer malpractice, or if the public would view the non-existence of such insurance a critical factor in the decision to retain a lawyer. But, as your process demonstrated, there is little evidence of either circumstance.372

In fact, the State Bar did not investigate whether clients were unable to recoup from uninsured lawyers.373 Like the State Bar, the Supreme Court also did not consider that when the public was asked to give open-ended answers about the factors that were important when selecting a lawyer, they were probably unaware that lawyers were not required to maintain LPL insurance. The Supreme Court also seemingly credited the argument “that the public may assume erroneously about mandatory disclosure that past insurance coverage is an assurance of future coverage,”374 even though that problem can be readily addressed in insurance disclosure rules.375

Why did the Court defer to the State Bar’s position, notwithstanding the Task Force’s close vote and the recommendation by the GOC to adopt a disclosure rule? The Texas Supreme Court has not historically been active in the area of lawyer regulation.376 Indeed, it has a history of protecting lawyers, at least in the area of lawyer malpractice.377 This orientation may be due, in part, to Texas’s traditionalistic/individualistic political culture and the fact that Supreme Court justices must raise more money for their reelection campaigns than justices in any other state.378 In addition, candidates want to do well in the State Bar’s judicial polls, which signal the strength of lawyer support for Supreme Court candidates.379 Candidates also rely on well-respected lawyers for endorsements that they advertise during their campaigns.380 Thus, Texas Supreme Court justices have significant incentives to maintain good relations with the bar.

When will states regulate to protect the public from uninsured lawyers?

What lessons can be drawn from these case studies? Each of the seven states has its own institutional relationships and rulemaking process. The reasons for some key events—including the state supreme courts’ decisions—are not fully known. But there are some similarities that suggest some tentative conclusions about when states will act to protect the public from uninsured lawyers.

It is worth pausing to ask: Where were the judges and where were the state legislatures in this process?

Bar support matters. The state bar’s willingness to endorse an insurance requirement seems to be crucial to the ultimate outcome. This can be seen in Oregon and Idaho—the only states that require LPL insurance—where the State Bars proposed mandatory insurance rules. In Oregon, many lawyers viewed the proposal as personally beneficial, because the PLF was expected to provide insurance at a lower price than they were paying on the open market. The legislature promptly enacted the OSB’s proposal. In Idaho, the ISB’s resolution to require LPL insurance barely squeaked by the membership in a vote of 51 to 49 percent. The Idaho Supreme Court, which traditionally adopts the ISB’s proposals, also did so in that instance. It is not always true, however, that states will adopt such rules whenever they are proposed by the organized bar. The Nevada Supreme Court rejected the State Bar of Nevada’s proposal to adopt an insurance requirement after it heard objections from rank-and-file members. When the state bar does not endorse such initiatives, however, the case studies (for example, in New Jersey and Texas) revealed that they do not become law.

Importance of individual lawyers. A second notable feature of most of the states’ experiences is that the impetus for examining the insurance issue came not from the courts but from individual lawyers. In Nevada, New Jersey, Texas, and Washington, the most recent calls to address the issue of uninsured lawyers came from individuals who did not hold leadership positions in the bar.381 In Idaho, a new ISB Commissioner raised the issue due to her personal experience with a victim of an uninsured lawyer.382 In California, a lawyer-legislator put the issue back on the agenda.383

What about the courts and state legislatures?

It is worth pausing to ask: Where were the judges and where were the state legislatures in this process?

Some courts may have failed to initiate action because they were busy with their main work—deciding cases—or because custom or law dictated such initiatives would come from the bar.384 Yet this is only a partial explanation. Public choice theory suggests that judicial inaction was predictable. Judges do sometimes initiate changes in lawyer regulation when it is in their self-interest. For example, justices have initiated efforts to address the problem of pro se litigants, who seriously burden the courts.385 But the issue of uninsured lawyers does not present a significant problem for the courts: these cases rarely make it to court at all, and they do not interfere with court administration. Nor is it a problem that has garnered much media attention. Furthermore, judges may anticipate that lawyers are likely to be divided on the issue of insurance requirements. Consequently, there is little reason for judges, as self-interested actors, to initiate steps to address it.

State legislatures have been mostly uninvolved in these issues.386 Legislators may have had little interest in spending time on legislation that would almost certainly be challenged in court (and possibly invalidated) based on courts’ assertion of their exclusive authority to regulate lawyers or on separation of powers grounds. It is also likely that state legislatures were not moved to take up this issue because constituents did not advocate for change and legislators did not wish to antagonize the bar. The exception is California, where the legislature has looked periodically at the issue and in 2017 ordered the State Bar to again study mandatory LPL insurance and other insurance issues. While the legislature’s top-down directive and its relatively tight time frame for the State Bar to issue a report may have contributed to the Working Group’s inability to make a recommendation on mandatory insurance, it at least squarely put the issue on the agenda.

Process matters—a lot. In Idaho, the Bar has the statutory authority to propose rules, and the Supreme Court mostly waits for it to do so. Likewise, in Nevada the common practice appears to be for proposals to emanate from the State Bar. In the latter, the regular process enabled a small group of leaders to petition the Supreme Court for an insurance requirement, notwithstanding significant member opposition. Yet some state bars are required to seek a membership vote on proposed rule changes;387 even where such votes are not required, bar leaders may put a proposed rule change to a membership vote for political cover.388 Membership votes to approve rule proposals can make the passage of public-regarding rules more difficult. Lawyers opposed to the measures can organize against them and help bring out the “no” votes, which happened in Texas. Exceptions may occur, however, in states like Idaho, where the process occurred so quickly that it may have been difficult to organize against the mandatory insurance proposal.

Cultural capture may help explain the courts’ decisions, especially when lawyers’ arguments were couched in terms of the impact of insurance requirements on their livelihoods.

Where the process permitted individual lawyers to directly advocate to the state supreme court—via public hearings or written comments—this also directly affected the outcome. Lawyers had no such opportunity in Oregon and Idaho, where LPL insurance is now required. In New Jersey, where the Supreme Court has thus far adopted an approach less protective of the public than its Ad Hoc Committee recommended, the Court indicated this was due to the lawyer comments it received. In Nevada, after the State Bar petitioned the Supreme Court to adopt an insurance requirement, the Court held a public hearing at which it heard significant opposition from well-respected lawyers, and then rejected the Bar’s proposed requirement. Cultural capture may help explain the courts’ decisions, especially when lawyers’ arguments were couched in terms of the impact of insurance requirements on their livelihoods.389

Bar leadership. The case studies further indicate that bar leadership matters. The Oregon State Bar’s leadership supported an insurance requirement, which they viewed as good for lawyers. In Idaho, the ISB commissioners assumed responsibility for studying mandatory insurance and then shepherded their insurance proposal to a successful conclusion. In Washington, bar leaders placed a strong proponent of mandatory insurance, a federal judge, an LLLT, a member of the OSB, and two public members on the Task Force that recommended the requirement.390 In Nevada, the Board of Governors petitioned the Supreme Court for an insurance requirement, even though they were aware that many members opposed it. Yet bar leaders in other states effectively undercut insurance initiatives. The president of the State Bar of Texas added anti-disclosure members to the Task Force later in the process, apparently to ensure defeat of a disclosure recommendation. The NJSBA opposed insurance initiatives through its designee on the New Jersey Supreme Court’s Ad Hoc Committee, subsequently wrote the Court to oppose the Committee’s recommendation, and seemingly succeeded in persuading the Court to hold off on a direct disclosure requirement.

Mandatory vs. voluntary state bars. The New Jersey experience suggests that the type of state bar association also may have affected the outcome. In states with mandatory bars, the organizations are usually public entities, their staff often performs some regulatory functions, and their mission typically includes public protection. In some states, their boards include nonlawyer members. Mandatory bars at least nominally have some obligations to the public. Voluntary state bar associations have no official regulatory function and are freer to function in a manner more akin to guilds. Even when they include public-spirited members, their boards may have more difficulty taking controversial positions because they want to maintain their voluntary members. In contrast to the mandatory bars in Oregon, Idaho, and Nevada, no voluntary state bar has advocated for an LPL insurance requirement.

Insurers. Another interest group—malpractice insurers—also influenced the outcome in some states. In California, insurer opposition to mandatory insurance in the 1980s effectively helped kill the legislature’s mandatory insurance initiative. In that case, commercial insurers wanted to maintain their insurance programs with voluntary bar associations. In New Jersey, commercial insurers assisted the NJSBA to help put the thumb on the scale against a malpractice insurance requirement. In contrast, in Idaho, Nevada, and Washington, a historically bar-affiliated insurer (ALPS), assisted with information gathering and supported some of the Bars’ initiatives to mandate insurance.391