This article is derived from a more expansive work later published in The Business Lawyer, volume 75, issue 1 (Winter 2019/2020). The full paper is also available on the Social Science Research Network here. Comments are welcome.

Law firms don’t just go bankrupt—they collapse. Dewey & LeBoeuf. Heller Ehrman. Howrey. Brobeck Phleger & Harrison. Thelen. All these firms and many others have blown up with extraordinary force and speed. Some large law firms have survived more than 100 years and then fallen to pieces in a matter of months or even weeks.

The force with which law firms shatter is amazing because it has no parallel in other kinds of businesses. Amazon lost money for more than 20 years. Chrysler filed for bankruptcy seven years ago. Yet both companies—like countless others that suffered financial problems before them—are still shipping goods and churning out cars. Law firms show no such resilience. No large law firm has ever managed to reorganize its debts in bankruptcy and survive. And the pressures that bring law firms down are often surprisingly mild. Most collapsed firms crumpled when they were still current on their debts and earning a profit. Law firms die with extreme ease and astonishing speed.

Why? Drawing on a review of every large law firm collapse in the past 30 years, I argue that the answer lies in the unusual way that law firms are owned. Unlike Amazon and Chrysler, law firms tend to be owned by their partners rather than by investors. And this makes the partners unusually sensitive to decline. As a firm’s profits drop, the decline can feed on itself and turn into a self-reinforcing spiral of partner withdrawals.

Law firms die with extreme ease and astonishing speed.

Partner ownership encourages a cascade of partner withdrawals for two reasons. The first is that, as owners of their firms, partners get paid in profit shares rather than fixed salaries or wages. This makes partners acutely sensitive to problems in a firm because it links their individual compensation to the fortunes of the firm as a whole. For some partners, at least, a decline in profits means a decline in pay. As profits drop, some of a firm’s partners will inevitably start to leave for better-paying opportunities elsewhere. But this causes profits to drop even more, which drives even more partners to leave. Profits then decline still further, causing even more partners to leave, and so on, until the firm finally collapses. If partners were paid in fixed salaries, they would not care about the declining profits. But because they are paid in profits, departures become self-reinforcing. As each partner leaves, the benefits of staying decline for all those who remain.

The second problem is that because partners are owners of their firms, they face crushing personal liability when a firm finally dissolves. All the compensation partners receive in the months leading up to bankruptcy can be clawed back as a fraudulent transfer, for example, and the partners’ capital investments in a firm can be taken away as well. Partners who stay too long may even have to give up billings they generate after the firm dissolves. All these liabilities flow directly from partners’ status as owners. The staff and associates face none of these liabilities. And unfortunately, these liabilities encourage partners to leave, because the only way to avoid them is to be among the first to withdraw.

Therefore, the net effect of partner ownership is to make law firms remarkably fragile. As we pick through the burnout ruins of firms like Dewey & LeBoeuf, it becomes obvious that partner ownership exposes law firms to the same horrifying logic of withdrawal that animates bank runs. A law firm can collapse, in other words, because partner ownership can drive a run on the partnership.

The pattern of collapse

Although the death of a large law firm tends to come as a shock to the people who work for it, law firms actually collapse in surprisingly predictable ways. Every large law firm blowup has followed the same basic pattern. This pattern emerged from a review of news and litigation records I conducted for every major law firm collapse since 1988. I reviewed 37 firms in all, starting with Finley Kumble (aka “Finley Crumble”) in 1988 and ending with Bingham McCutchen in 2014. The list of firms includes marquee names like Dewey & LeBoeuf, Heller Ehrman, and Coudert Brothers, and slightly lesser known but still important firms like Darby & Darby, Adorno & Yoss, and Lord Day & Lord.

At the time a typical partner run commences, the firm is still generating a large profit, but profits have diminished relative to a previous high. This decline in profits is significant, but not catastrophic, and the firm is still easily current on its debts. The firm’s management is struggling to hold partner draws steady at the previous high, however, and the firm increasingly borrows from banks and starts to run down capital reserves to generate extra cash.

The partner run commences with the departure of a senior rainmaker. The departure might happen for a purely random reason—the rainmaker might die, for instance, or leave for government service. Or the rainmaker might exit after his or her defeat in a power struggle—perhaps even a power struggle over how to improve the firm’s poor performance. The departing rainmaker will take along a group of other partners and associates who also service his or her clients.

Within a few months after the senior rainmaker’s departure, another, slightly less senior rainmaker will also leave, again with an entourage of partners and associates in tow. This rainmaker’s exit will be followed within about a month by still more departures, also in large clumps as practice groups decamp for other firms.

The departure of all these marquee partners will leave the firm with fewer client revenues, even as it has the same office leases, pensions, bank loan payments, and other obligations that still have to be paid. As more partners leave, the firm will borrow more and more money to keep partner compensation on a level plane. Senior partners remaining with the firm will also attempt to renegotiate their compensation. They will make large, sometimes outrageous demands, knowing that the firm may have no choice but to agree, since it cannot survive if they depart. As more partners leave, the firm’s financial position will worsen. Besides taking clients, the departing partners will also often withdraw their capital from the old firm, leaving the firm short on cash even as the demands on its cash increase.

At some point in the spiral of departures, the firm will trip a series of covenants in its bank loans and lease agreements. By this point the firm will have substantial borrowings from a single bank—most likely Citibank (See this issue’s Speaker’s Corner to hear from the chairman of Citi Private Bank’s Law Firm Group). These borrowings will be secured by a general lien on all the firm’s assets. The covenants will require the firm to maintain a minimum number of partners or to avoid more than a certain number of partner departures in a fixed period of time. When these covenants have been tripped, the lenders will seek to renegotiate, often demanding accelerated payment or new covenants in exchange.

At some point the firm will begin merger negotiations with a healthier firm. If the negotiations succeed and the merger occurs, the firm will be saved. If the merger negotiations fail, the firm will die. And when it does, the end will come swiftly. The management committee will call a meeting of the partners to announce that the game is up, and the partners will vote to formally dissolve. The associates and staff will be stunned (see “Caught in the Collapse”). Unlike many of the partners, relatively few of the staff and associates will have left of their own accord prior to the dissolution.

Strangely, the firm may still be profitable on the day of its dissolution. Although it will have distributed more profit than it actually earned in the months prior to collapse, it will still be earning a significant accounting profit up through the very end, and it may even remain current on its debt payments.

After the firm has dissolved, its creditors may force it to enter bankruptcy. Because the firm will have few physical possessions, its major assets will consist of claims against others, most notably the former partners. Although the shield of limited liability will protect the partners from general personal liability for the firm’s debts, this shield will be useless against a variety of indirect claims that flow from the partners’ status as owners and come out of the laws of fraudulent transfers, preferential transfers, and unfinished business. The value of all these claims, if pressed to their limit, would be enough to push many of the partners into personal bankruptcy. Fortunately for the partners, however, the bankruptcy trustee or creditors will settle these claims for a fraction of their value. The creditors will recognize that although the legal merits of their claims may be strong, the obstacles to collection are profound. The partners will be widely dispersed across multiple states and foreign countries, making litigation extremely expensive. And even if the creditors obtained judgments, collection efforts would yield little since the partners would be capable of declaring personal bankruptcy and might have sheltered many of their assets in estate-planning devices.

Nevertheless, the partners’ fate will not be happy. Most of the partners will have left the old firm not because they expected more money but because the spiral of departures left them with no choice but to leave. And although some of the partners may have gained a raise by leaving, much of the value of these raises will have been eaten up by liabilities.

The puzzles

The spiral of partner departures that drives a firm into collapse might seem obvious—even ordinary. But if we approach it carefully, it looks quite puzzling. It is not clear why the partners would leave in the face of decline because the employees of other kinds of businesses don’t leave in the same way. During the two decades that Amazon lost money, the employees didn’t leave—they flocked to the firm en masse. And even when Delta Air Lines and Chrysler went bankrupt, almost all their employees stuck around.

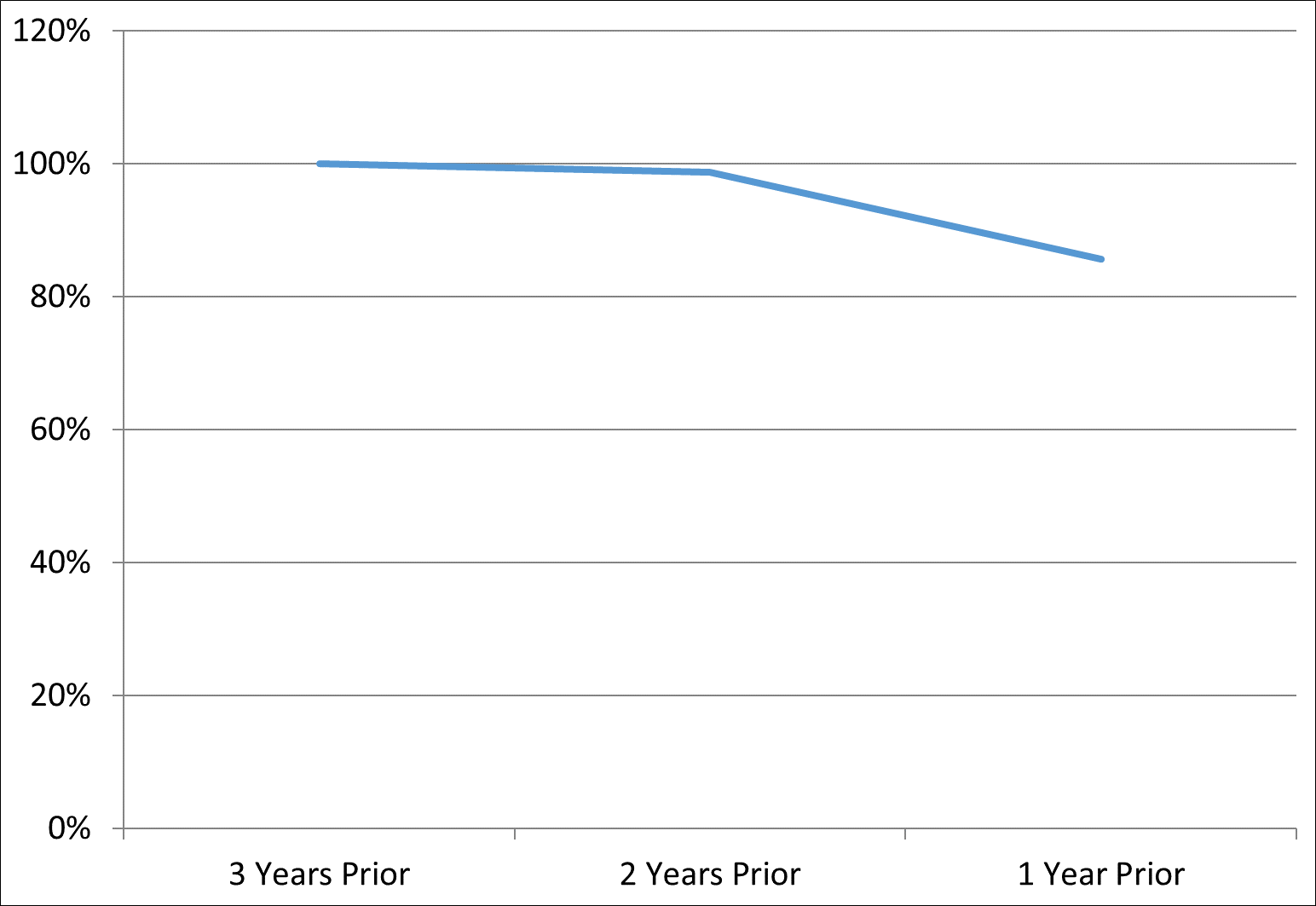

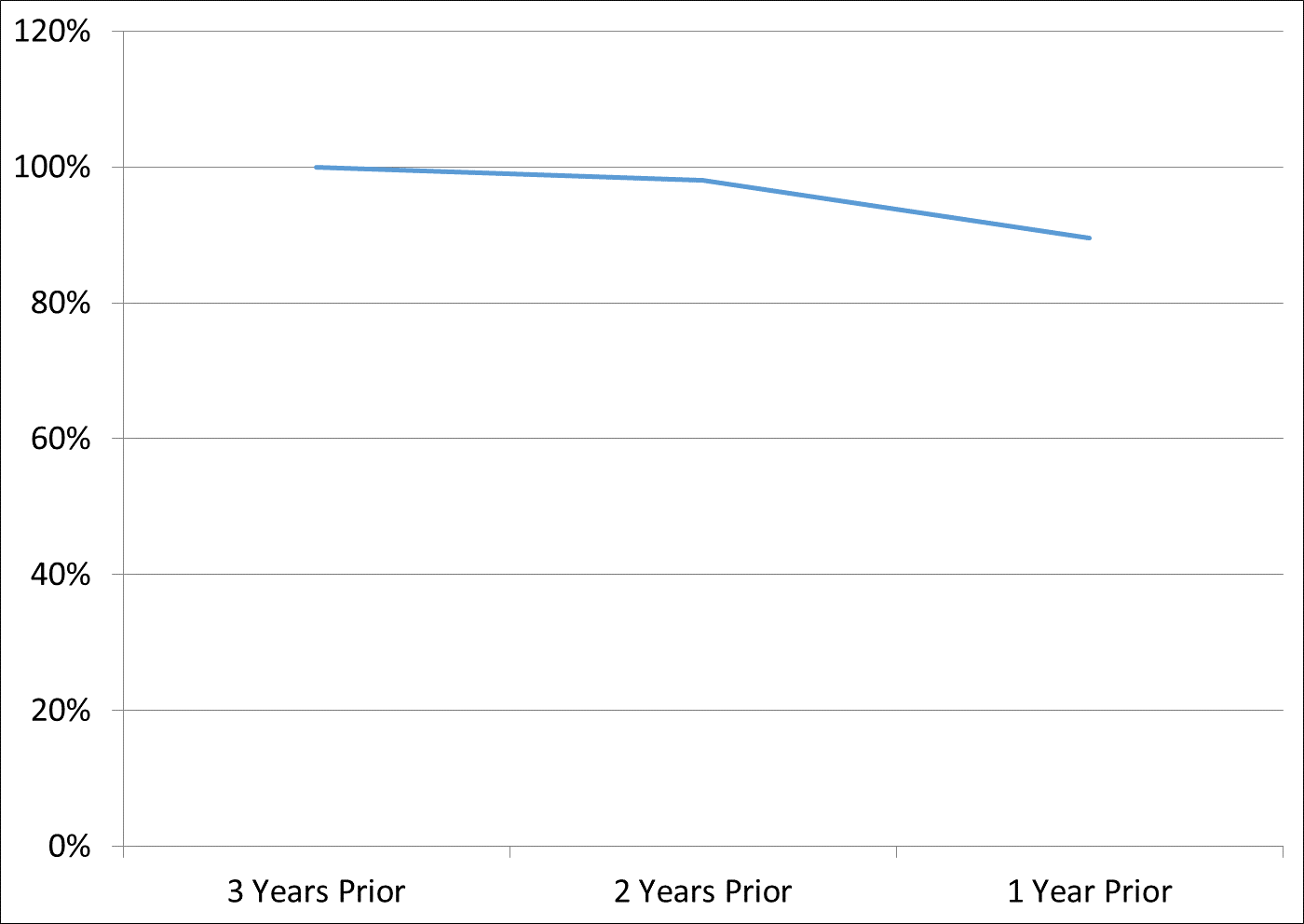

Another puzzle is why the intensity of law firms’ declines was so out of proportion to their financial distress. Figures 1 and 2 (below) use data from the American Lawyer’s annual ranking list to show that the finances of defunct firms declined only slightly in the years just prior to the collapse. Things got worse at these firms, but they weren’t nearly bad enough to put an ordinary company like Amazon or Chrysler out of business—or even into bankruptcy.

And another puzzle is why law firms should experience financial distress at all. Law firms’ capital structures are freakishly robust. Since a law firm is owned by its partners, its largest expense—partner compensation—is not technically an expense at all and doesn’t even have to be paid. Profit distributions are purely discretionary. This leaves law firms with huge amounts of revenues that they can theoretically divert to any expense they wish, including the repayment of debt. Far from being fragile, law firms would seem to be almost unbreakable.

Partner ownership and partner runs

But, of course, law firms break anyway—often with astounding force. And so there must be something else going on. Since the problem cannot be mere financial distress, it must instead be a deeper structural weakness that other businesses don’t share. And that weakness is a vulnerability to a partner run.

A partner run takes its force from the peculiar way in which law firm partners decide to leave or stay. That is, every day a law firm partner compares the costs and benefits of leaving to those of staying, and then chooses the option that offers the greatest benefits net the expected costs. On most days, the choice is implicit and unthinking. But on the day a partner starts to seriously contemplate leaving, the choice becomes quite deliberate.

In the United States, the costs of leaving tend to be low because of our peculiar professional ethics rules. Unlike legal ethics rules in the United Kingdom and elsewhere, the American Model Rule of Professional Conduct 5.6(a) says, in essence, that a firm cannot ask a partner to sign an agreement not to leave. The rule prohibits, among other things, the competition of covenants and the retention of partners’ capital contributions. The net effect of these restrictions is to make leaving comparatively easy.

What ultimately drives a partner run, though, is not just the low cost of leaving but the way that successive partner departures tend to reduce the benefits of staying for the partners who remain. As more partners leave, the advantages of staying decline. This is a direct consequence of partner ownership.

Partner departures across time

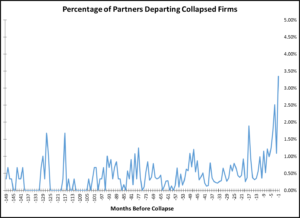

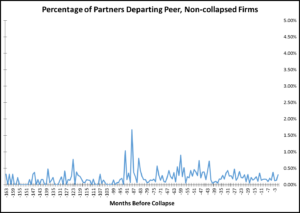

Partner departures ramp up exponentially as a firm starts to collapse. The top figure (figure 3) uses data from the American Lawyer on partner movements to show the average percentage of partners who departed collapsed firms in each month prior to collapse. The bottom figure (figure 4) presents the same data over the same time periods for healthy non-collapsed peer firms with similar profits per partner. In both graphs, time 0 represents the date a collapsed firm ceased operations.

Residual risk bearing

Ownership links partners together because it transforms the firm’s partners into its residual risk bearers. The partners win or lose if the firm’s profits go up or down. Since partners are paid in profits rather than in fixed wages or a cash bonus, the value of their shares in the firm fluctuates with everything that affects a firm’s profitability. Even events entirely outside an individual partner’s control—a spike in electricity rates for the office space, say, or an increase in market rates for associate bonuses—can reduce the pool of profits and the partner’s take-home pay.

The partners’ status as residual risk bearers is important because it sensitizes the partners to one another’s departures. If one partner’s departure makes the firm less profitable, the remaining partners bear the loss. If partner A leaves and profits drop as a result, the compensation of partner B will automatically have to be cut. This in turn will make partner B more likely to leave for another firm as well. And, of course, once partner B heads out the door, the profits might drop still further, putting partner C on the edge, too. The result is a run on the partnership.

When a partner decides whether to leave or stay, the benefits of staying depend heavily on whether other partners stay as well.

The key to a run on the partnership, in other words, is that when a partner decides whether to leave or stay, the benefits of staying depend heavily on whether other partners stay as well. The benefits of staying are a function of a firm’s profits. And the firm’s profits are a function of whether other partners are choosing to stay. The more partners who leave, the less attractive staying becomes. And when staying becomes less attractive, even more partners leave, and so on until the firm falls apart.

Partners would not run like this if they did not own their firms. If partners were ordinary employees rather than owners, they would be paid in wages or performance bonuses that did not fluctuate with profits. And the partners’ compensation would therefore be basically independent of the firm’s overall profitability—and the number of other partners who have left. As other partners depart and the profits decline, the remaining partners compensation could stay basically the same, just as it did for the employees of Amazon and Chrysler when those companies were losing money. If a law firm were not owned by partners—if, like Amazon and Chrysler, it were owned by investors—then the drop in profits caused by a partner’s departure would be borne by the investors rather than the remaining partners. One partner’s departure might reduce the firm’s profits, but there would be no reason for any other partner to care about it, and it would not increase the odds that other partners would withdraw as well.

Thus a run happens whenever successive waves of partner withdrawals make a firm less profitable. This is the central reason law firms collapse. But we should be cautious, of course, to assume that every departure makes a firm worse off. Some departures actually improve a firm’s bottom line by saving the firm the cost of the departed partner’s compensation and administrative expenses. If the firm loses less in client revenue than it saves in compensation and administrative expenses, then the firm might actually be better off when a partner leaves. This is why firms occasionally fire their underperforming partners.

But even though some departures can make a firm better off, other departures can be devastating. The biggest problem is that many of a firm’s costs tend to remain fixed even after a partner leaves. Even if a firm saves the cost of a departed partner’s compensation, it may not be able to fully cover the drop in client revenues by saving money in other areas. The firm might still have to pay the rent on the departed partner’s corner office, for example, and pay bank debts and pension obligations, which stay the same regardless of how many offices at the firm have the lights on.

In Howrey’s last full year of operation, the firm paid out more than $113 million to departed partners even as the firm took in only $262 million.

Partner departures can also hurt for other reasons. One problem is a kind of selection bias in partner withdrawals. In general, the partners who leave first tend to be the ones who are most underpaid, since they are the ones who find it more appealing to leave than to stay. But the underpaid partners are precisely the ones who do the most to benefit the firm’s bottom line. Partner departures can also hurt a firm by siphoning away its capital. Model Rule of Professional Conduct 5.6, which requires a firm to return capital to partners as they depart, can bleed a firm to death. In Howrey’s last full year of operation in 2010, the firm paid out more than $113 million in capital to departed partners even as the firm took in total revenues of only $262 million.

Another cause of declining profits is the renegotiation of remaining partners’ compensation. As the pie shrinks, everyone who remains inevitably wants a larger slice in order to keep his or her total takeaway the same. These demands for more pay tend to be credible because a dollar of compensation at a collapsing firm is actually worth less than a dollar of compensation at a healthy firm, due to the risk of personal liability on a firm’s collapse. Partners can thus seriously threaten to leave unless they are paid even more than their market value. But all these demands for more pay ultimately drive more lawyers from the firm because the division of profits is a zero-sum game: more money for one partner means less for another. And the partners who lose become more likely to leave.

Personal liability

Profits are not the only thing partners lose as a firm declines. Their status as owners also exposes them to significant personal liability. This is the second reason ownership drives partners to run, because the only way partners can avoid personal liability is to get out early.

Fraudulent transfer liability for compensation. The most serious liability comes from the doctrine of fraudulent transfers, which allows a creditor to void any payment a firm makes after it becomes insolvent if the firm does not receive something of reasonably equal value in exchange. Basically, fraudulent transfer doctrine prevents a debtor from giving away its assets to its friends on the eve of bankruptcy. A law firm partner’s status as an owner exposes his or her compensation to fraudulent transfer doctrine because it turns the compensation into a profit distribution rather than a wage. Since partners are owners, their draws are distributions of profits, not payments of wages or salaries.

Under well-established principles of bankruptcy and state law, a profit distribution is a fraudulent transfer because it doesn’t technically have to be paid. Like Apple, which sits on tens of billions of dollars in retained profits, a law firm could, in theory, choose not to distribute profits if it wished. And so any decision to pay profits basically amounts to a gift, making it recoverable by creditors under fraudulent transfer law. Profits stand in contrast to wages because wages become a contractual obligation once an employee has earned them. Profit distributions are optional; wage payments are not. Hence profit distributions are voidable under fraudulent transfer doctrine, whereas wage payments are not.

The threat of losing pay to fraudulent transfer law encourages partners to leave early because the sooner they leave, the less of their pay will be eaten up by fraudulent transfer law. If a judge rules in bankruptcy that a firm became insolvent one year prior to dissolution, partners who stayed on through the moment of dissolution will have to return an entire year’s worth of pay to the firm’s creditors. Partners who left 10 months prior to dissolution, however, will only have to return two months of pay. And partners who left more than a year prior to dissolution will not have to return anything at all. The lesson is to leave early.

The only way partners can avoid personal liability is to get out early.

Preferential transfer liability for capital contributions. Model Rule of Professional Conduct 5.6 requires a law firm to repay a partner’s capital contribution when he or she withdraws, so when a firm starts sinking, many partners start leaving in the hope that they can grab their capital before the firm goes completely underwater. But a partner has to act quickly, because the bankruptcy code’s doctrine of preferential transfer stands ready to catch anyone who waits too long. The purpose of preferential transfer doctrine is to prevent a debtor from paying some of its creditors in full on the eve of bankruptcy when others will be paid only in part later on. It does this by letting a bankruptcy trustee void an overly generous payment to a creditor if the debtor made it at a time when the debtor was insolvent. Preferential transfer law encourages partners to leave early because partners who get their capital out before the firm becomes insolvent are allowed to keep their capital, whereas partners who get out after insolvency lose it. Partners who get out early enough may even be protected by the statute of limitations. The lesson, once again, is to get out quickly.

Unfinished business liability. The saddest source of liability is the so-called unfinished business, or “Jewel,” doctrine. This doctrine has vague origins in the Uniform Partnership Act (UPA) and the Revised Uniform Partnership Act (RUPA), but it finds its clearest foundation (and its colloquial name) in Jewel v. Boxer, a 1984 California Court of Appeals opinion involving the breakup of a small law firm. The Jewel doctrine says that partners who remain with a firm up through the time of its dissolution must share with the firm the proceeds of any work they perform after dissolution on matters that belonged to the firm at the time of dissolution. Jewel liability is not merely an obligation to help a firm collect on billings accrued prior to a partner’s departure; it is an obligation to share new billings for work a partner does after the firm dissolves. The rule has been applied widely to all types of dissolved law firms. It reaches not only firms organized as general partnerships but also firms organized as limited liability partnerships, professional corporations, and limited liability companies. Jewel claims were often among bankrupt law firms’ largest assets, and settlements commonly reached millions of dollars.[1]

The logic of the Jewel rule is to protect the partners from one another. In the absence of the rule, the argument goes, partners could back out of their partnership agreements and take partnership profits for themselves by absconding with valuable business. Forcing partners to return fees to their old firms is supposed to ensure that all the partners share the fruits of partnership business on the terms dictated by the partnership agreement. It stops the partners from stealing opportunities from the firm.

This makes a good deal of sense, but in practice it encourages a race to the exits. This is because Jewel has been interpreted to flip on like a switch at the moment of dissolution: it applies to partners who stay until dissolution, but not to partners who leave just prior. This creates terrible incentives. Partners who stay until dissolution face millions of dollars in liability, while partners who leave one day prior to dissolution walk away completely free. Although Jewel was designed to punish partners for leaving early, it actually punishes them for leaving late. The lesson of Jewel is to get out before the firm dissolves.

In Comparison

The reason law firms are so fragile is that their structural makeup encourages partners to leave in spiraling cycles. Ownership exposes partners to the risks of declining profits and serious personal liability, and the best way to avoid those risks is to get out early in the cycle of decline. The result is a race to the exits.

Ideally, we would be able to test this ownership-based theory experimentally or statistically, by comparing firms that are owned by partners to firms that are owned by others, and asking which were most likely to collapse. But that isn’t possible, because Model Rule of Professional Conduct 5.4 effectively requires every firm in the United States to be owned by its partners. The best way to validate this theory about the connection between ownership and collapse is thus to look a little more widely for comparisons. We may not be able to compare partner-owned law firms to investor-owned law firms, but we can look around for other comparisons.

Associates and staff. One comparison is the associates and staff of a law firm. It is often said that law firms are fragile because “their assets go down the elevator every night.” But some assets are more likely to come back up the elevator than others: associates and staff tend to stay at comparatively high rates even as the partners leave. Although associates and staff seem to leave at higher rates in times of decline, they primarily leave on the heels of the partners they work for. They do not appear to go in search of other jobs as quickly as partners do.

One explanation is that associates and staff have fewer options in the labor market than partners do. This may be true, and if so, it would tilt the associates and staff in favor of staying. But, of course, there is another explanation as well: the associates and staff are not owners. They might lose their jobs, just as partners might if the firm dissolves. But unlike partners, associates and staff will not have their pay cut as the firm declines and they won’t get sued if they stay too long. This makes staying until they get laid off much more attractive.

Accounting firms. Accounting firms are also owned by their partners. Arthur Andersen, the partner-owned accounting firm that audited Enron, collapsed and went into liquidation with astonishing speed after it was charged with a crime in connection with the Enron scandal. And Andersen was not the only accounting firm to blow up like a law firm. In early 1990, Laventhol & Horwath was the seventh-largest accounting firm in America. But later that year, the firm collapsed and filed for bankruptcy in a pattern virtually identical to that of many law firms: the firm dissolved after about a quarter of its partners fled in a six-month period in response to a decline in profits.

Shareholders in investor-owned companies. Law firm partners also stand in interesting contrast to investors who own ordinary industrial companies. Like law firm partners, investors in an ordinary company also have an incentive to run, since they, too, will suffer when profits decline. Unlike law firm partners, however, investors in an ordinary company cannot run because the corporate charter prohibits them from withdrawing unilaterally. Shareholders in an ordinary company like General Electric can sell their shares, but they cannot actually take back their money from the firm. They cannot unilaterally ask GE to give them back the portion of its factories, brand names, and cash that corresponds to their shares.

The only way for GE shareholders to get their money back is to pay themselves a dividend, but this is subtly different from a law firm partner’s right to exit. Dividends in ordinary companies have to go to every shareholder at the same time and on the same terms. No shareholder can individually get out on his or her own. There is thus no reason for investors to race to leave because everyone has to leave simultaneously. The terrible inertia of individual decision making disappears.

[1] For examples of settlements of unfinished business claims, see Order Granting Motion by Liquidating Debtor for (1) Approval of Settlement of Claims Against Covington & Burling LLP and IP Shareholder Defendants Under Bankruptcy Rule 9019, (2) A Finding of Good Faith Settlement Under California Code of Civil Procedure § 877, and (3) Leave to File Second Amended Complaint, In re Heller Ehrman LLP, No. 08-32514 (Bankr. N.D. Cal. Aug. 11, 2011) (approving a $4,996,213 settlement for unfinished business claims); Order Pursuant to Rule 9019 of the Federal Rules of Bankruptcy Procedure Authorizing and Approving a Settlement Agreement Between the Plan Administrator and Baker & McKenzie LLP, In re Coudert Brothers LLP, No. 09-01150 (Bankr. S.D.N.Y. Aug. 20, 2010) (approving a $6,650,000 settlement for unfinished business claims); Order Approving Settlement Agreement with Morgan Lewis & Bockius LLP & Finding That Settlement Is in Good Faith at 4, In re Brobeck Phleger & Harrison LLP, No. 03-32715 (Bankr. N.D. Cal. Nov. 10, 2004) (approving a $10,200,000 settlement for unfinished business claims).

Dewey & LeBoeuf

Partner ownership seems to be one of the key factors in explaining why law firms collapse with such unusual force and speed. But does it really change anything about how we understand law firm blowups? Usually, we explain the bankruptcy of a business such as Chrysler or Delta Air Lines as a simple combination of declining revenues and increasing costs. Do partner ownership and the notion of a partner run add anything to our understanding that mere financial distress does not?

To see why it does, consider the collapse of Dewey & LeBoeuf, still the largest law firm bankruptcy in history. Many people—including the Manhattan district attorney—have attributed Dewey’s sudden and astounding collapse to the fraud of its managers. How else, one might ask, could such an old, prestigious, and profitable firm have fallen apart so swiftly? A focus on partner runs actually provides an answer. Although the firm’s managers may well have been telling lies, the swiftness of Dewey’s collapse has parallels even in firms where the managers were not telling lies. Partner ownership creates a set of incentives that might have pushed Dewey to a swift and deadly end even if its managers had been completely honest.

Partner ownership also gives us a new perspective on the role of debt and fixed salaries. It has often been said that the cause of Dewey’s collapse was its tendency to pay fixed salaries to partners who were recruited laterally from other firms. News reports tell us that Dewey made too many compensation guarantees, and when the partners who received these guarantees failed to perform, the firm didn’t have enough money to go around. Dewey was, on this telling, no different from Chrysler or Delta Air Lines or any number of other bankrupt businesses that took on too many costs without enough revenues.

This story makes intuitive sense, but a focus on partner ownership would tell the story rather differently. Guaranteed partner salaries alone could not have driven the firm to be incapable of paying its debts because, as we have already seen, partner ownership gives law firms freakishly robust capital structures. Even at the time of its death, Dewey, like every other law firm in America, had many partners who were still being paid in profit shares rather than fixed salaries, so it had huge free cash flows over which its managers had total discretion. Although Dewey’s managers chose to pay out these cash flows as profit distributions to partners, they could in theory have used them instead to pay the fixed salaries, as well as debts, utility bills, and any number of other contractual commitments that might have come up. Far from being insolvent, Dewey remained profoundly profitable—at least as an accounting matter—almost up through the day of its dissolution. The focus on fixed partner salaries is also a bit naive because it ignores the extent of other salaries in the firm. Every law firm—including healthy ones—has many people who usually get paid in salaries. These people are called associates and staff. The addition of a handful of salaries for the partners thus could not, by itself, have bankrupted the firm. Something else must have been at play: the tendency of partners to run in the face of declining profits.

In a law firm, debt tends to be a lagging, rather than a leading, indicator of decline.

Also, a focus on partner ownership gives a clearer picture of why exactly Dewey started paying all these fixed salaries. News reports have told us that all the fixed partner salaries were given out as recruitment incentives to partners coming laterally from outside the firm. But in fact, most of the salaries went to partners who had already been at the firm for years. And we can now see why these partners wanted the fixed salaries so badly. It wasn’t just that the partners were greedy; it was that they were seeking shelter from the risk that the firm’s profits would decline. By demanding to be paid in salaries rather than profit shares, some of the partners were trying to transform themselves from owners into creditors. They were hoping to avoid the slide profits that inevitably hurt the owners of a firm in decline. And from the perspective of the firm’s managers, fixed salaries made sense, because they knew that paying salaries was the only way to keep many partners at the firm. If partners were paid in profits, they would leave, making the firm even less profitable and even more precarious for everyone who remained. The popularity of salaries among Dewey’s elite is proof of the importance of ownership in pushing a firm to collapse. It shows us how precarious ownership can be in a time of decline.

Dewey’s experience with fixed salaries is more broadly typical of other collapsed firms’ experiences with debt. A salary is a kind of debt because it represents a contractual obligation that has to be paid in a fixed amount at a fixed moment in time. Debt, like partner salaries, is often said to be the main cause of law firm collapses, for the same reasons it is said to make businesses like Chrysler and Delta Air Lines insolvent. But this isn’t exactly right, because law firms’ capital structures are so robust that the firms rarely become incapable of paying their debts until almost the moment of their death. And so debt plays a different role in law firms than in other businesses. In a law firm, debt tends to be a lagging, rather than a leading, indicator of decline. Firms often take on large amounts of debt only after profits have begun to decline, mostly as a way of desensitizing their partners to profit declines. When a firm’s profits are declining, the management can conceal the decline and therefore keep the partners from leaving by paying partner draws with borrowed money. At Finley Kumble, which in the late 1980s became the first large American law firm to collapse, many of the partners realized how serious the firm’s distress was only when they received their K-1 partnership tax returns at the end of the year, which showed how much of the distributions they received over the prior year had been funded with debt. Debt surely made things worse at Finley Kumble. But the firm took on the debt only after the firm’s profits were already declining and its partners were departing.

Debt is so unimportant in a law firm that we can imagine a law firm collapsing even without any financial debts at all. If profits declined enough, partners could start to leave the firm in a self-reinforcing spiral even if the firm never took out a loan and never fell behind on its debt payments. A firm’s partners could leave simply because profits were dropping.

Perhaps the most important lesson a theory of partner runs can teach us about the Dewey collapse is to show why financial distress was so much more destructive at Dewey than at other kinds of businesses. Many businesses lose money, but almost none blow up like Dewey & LeBoeuf. And Dewey didn’t even lose all that much money. Dewey was, as we have seen, technically profitable almost until the end. To understand why Dewey collapsed, we have to go beyond mere financial stress and understand how that financial stress became magnified and distorted by the force of a partner run. Financial stress might have pushed Dewey off a cliff, but it was the weakness of Dewey’s ownership structure that caused it to shatter when it hit the ground. Other businesses are made of rubber, but Dewey was made of glass.

Why some firms live while others die

The forces pulling law firms apart are not irresistible. Most firms manage to survive them because most of the time, they enjoy a kind of equilibrium in which partners are inclined to stay at their current firms. A firm begins to collapse only when partners fall out of this equilibrium. The key to figuring which firms will collapse is to identify the forces that tilt a firm out of equilibrium and start the snowball of partner departures rolling.

Although elite law firms have almost all become much larger, most of the collapsed firms expanded with a speed and aggressiveness that was unusual even among their peers.

Financial stress. Although financial stress is not the only cause of law firm collapse—one of the lessons we learned from Dewey—financial stress does matter, albeit in a surprising and unconventional way. Firms collapse not because their profits decline in absolute terms, but because their profits decline in relative terms. Since they pay their partners in discretionary profit distributions rather than fixed wages or bonuses, they have enormous free cash flows that they can use for almost any purpose, including the repayment of debts. What really matters, therefore, is not a firm’s overall profits but its ability to convince its partners to stay. And this depends not so much on a firm’s absolute profits but on its relative profits—i.e., its ability to pay its partners more than its competitors. The relative nature of profits is so important that a firm could theoretically collapse even at a time when its profits were increasing if the profits were not increasing fast enough to keep pace with competitors.

To be a bit more precise, what truly matters is the change in relative profits. Some law firms will always be more profitable than others. This is just a fact of life. But most firms nevertheless remain stable because the market for partners usually sits in an equilibrium in which each lawyer settles at the firm that offers him or her the best deal. Partner runs commence when the market falls out of this equilibrium because a firm has changed its profitability relative to competitors.

Knowing the importance of relative profits is useful because it tells us that law firm collapses should actually be surprisingly unrelated to large, industrywide shocks like financial crises and recessions. A truly widespread event may diminish the profits at every firm, but partners will start to move around only if profits diminish more at one firm than another. Slowdowns in demand for legal services will drive firms to collapse only when they damage those firms relative to their competitors, perhaps because one firm is more exposed to a particularly slow practice area than other firms. For this reason, a truly industry wide decline like the ones now afflicting newspapers and recorded music would not necessarily cause individual law firms to collapse. If crises and recessions cause firms to collapse, it is only because some firms are more heavily damaged by the declines than others.

Jenkens & Gilchrist, a Dallas-based national law firm, is illustrative. The firm collapsed in 2006 after three partners in the firm’s Chicago office were sued for selling fraudulent tax shelters. The liability ultimately became a major financial problem: $81.55 million in the final settlement. But the firm could easily have remained solvent in the face of this liability if it could have kept its partners. But, of course, the firm could not hang on to its partners because the liability was unique to Jenkens & Gilchrist. None of the firm’s competitors shared this huge loss, so none of the competitors’ profits were diminished. This made Jenkens & Gilchrist’s partners easy picking for headhunters. Jenkens & Gilchrist spiraled downward in a classic partner run, declining from 600 lawyers when the liabilities first emerged in 2001 to 281 lawyers when the firm finally closed its doors five years later.

Expansion. Although it is difficult to pinpoint a single event that causes the most partner runs, the most important event seems to be expansion. Although elite law firms have almost all become much larger in the past 40 years, most of the collapsed firms expanded with a speed and aggressiveness that was unusual even among their peers.

Expansion poses a number of risks, each of which can worsen a firm’s relative performance and drive its partners to leave. One risk is the cost of investing in new office space and partners. Brobeck Phleger & Harrison nearly doubled the number of its attorneys from 1997 to 2000, and it invested in a beautiful new office to contain all these new lawyers. But the beautiful office brought some very ugly costs. Brobeck earned about the same amount of revenue in 2002 as it did in 1999, but its real estate costs had ballooned from 6.6 percent of revenues to 15.2 percent. Although the firm could easily have paid these costs if it had suspended profit distributions, the decline in profit distributions was not sustainable because it pushed the partners to run in early 2003.

Client loyalty. The placement of client loyalties is also important. If clients are loyal to firms rather than to individual partners, partners will be less likely to leave and the firms will suffer less damage when they do. Often, however, firms fail to cultivate firm-level client loyalties, and when this happens, a lot can depend on how widely the loyalties are distributed among the partners. When client loyalties are concentrated in a handful of big rainmakers, it can be either good or bad for a firm. On the one hand, the concentration of client loyalties in a few big rainmakers can benefit a firm by making it robust to the departure of everyone other than one of the key rainmakers. Since no one but the rainmakers can take the firm’s clients away, no one but the rainmakers can damage the firm by leaving. On the other hand, if one of these rainmakers decides to leave, the result can be disaster. Altheimer & Gray, an 88-year-old Chicago firm, tells the tale clearly. The firm spiraled downward in a matter of months in the early 2000s after Gery Chico, the firm’s charismatic chairman and central rainmaker, stepped away to run for the U.S. Senate in 2002.

Bonding capital. Partner ownership places huge strains on partners’ financial ties to a firm during times of decline by reducing the partners’ compensation as other partners leave. Weak financial ties can force a firm to depend instead on informal nonfinancial ties. A firm can start to rely on what a sociologist might call bonding capital—the investment in relationships that inculcates feelings of friendship, loyalty, and trust. Firms are less likely to collapse when bonding capital is strong. If partners respect and value their colleagues, they will tend to stay even as their pay gets cut. If bonding capital is especially strong, partners may even cease to think in terms of money at all and might instead prioritize values and people. Ties of trust can be especially important because they can make it possible for partners to rely on one another in times of stress. In May 2014 the chairman of Patton Boggs slowed down a partner run—and may have saved the firm—by asking each of the remaining partners to commit to stay (around 90 percent agreed). These commitments were never written down, and would have been unenforceable even if they were, but the partners had enough trust in one another that they were able to stay long enough to complete a merger that saved the firm.

Size. Another risk factor is size, thought its effect can be ambiguous. A larger size decreases the odds of collapse by reducing the proportional significance and diversifying the risk of withdrawals. In a firm of three partners, the death or departure of just one partner is catastrophic; in a firm of 1,000 partners, it is meaningless. In other ways, however, a larger size can make collapse more likely. One of the biggest problems is that size can inhibit the sense of identity and the bonding capital that binds partners to a firm.

Possible solutions

When the combination of bonding capital and financial capital fails, the resulting run on a partnership can be terrifying. How, then, can a run be stopped? And how can a firm protect itself from ever suffering a run in the first place?

The first solution is for all large law firms to amend their partnership agreements to waive liability for Jewel-style unfinished business claims. Recall from above that a desire to avoid unfinished business liability can push partners to race for the exits to avoid getting stuck in a firm when it finally dissolves. Courts clearly permit firms to waive unfinished business liability, but amazingly none of the large firms that have collapsed in recent years have properly done so. An unfinished business waiver is effective only if it happens early, because if a firm waits until after a bankruptcy determines the firm to be insolvent, the waiver will be deemed unenforceable as a fraudulent transfer in bankruptcy. Brobeck, Thelen, and Heller Ehrman all learned this lesson the hard way. Another strategy for reducing unfinished business liability is not to dissolve at all. Since unfinished business liability applies only to a firm’s partners at the moment of a firm’s dissolution, a firm can avoid unfinished business liability by simply not dissolving. Perhaps for this reason, Bingham McCutchen has still not dissolved, more than two years after the last lawyers left the firm.

In addition to waiving unfinished business liability, law firms should also amend their partnership agreements to delay paying out capital to departing partners. The Model Rules of Professional Conduct permit a firm to delay capital repayments to withdrawing partners by making the payments incrementally over several years. Delaying repayments can prevent a firm from bleeding to death as departing partners ask for their money back. Firms should be aware that there is a downside to hanging on to capital payments, however—if the firm ultimately does collapse, the partners will never get their capital back.

Firms should also consider recharacterizing their partners’ compensation as salaries and bonuses rather than as profits. This might make compensation less vulnerable to recovery as a fraudulent transfer in bankruptcy, since the compensation would become a contractually required payment in exchange for labor rather than a discretionary distribution of profits. To be clear, this is an untried strategy, but it might be worth a shot.

If management sees a run starting, another solution is to talk with partners directly and get their informal, verbal commitments to stay. Model Rule of Professional Conduct 5.6 prohibits partners from signing agreements to stay, but the partners can nevertheless give handshakes agreeing to not leave. And a handshake, though softer than a contract, is surely better than nothing at all.

Investor ownership would powerfully diminish the risk of a run by diminishing lawyers’ sensitivity to decline.

Another tried-and-true strategy is to merge with a healthier firm. Virtually every collapsed firm has gone to its grave only after failing to find a merger partner. Heller Ehrman, for example, was publicly reported to have seriously discussed mergers with at least three firms—Baker & McKenzie, Winston & Strawn, and Mayer Brown—and it probably held conversations with many more. Other firms, like Patton Boggs, have found saviors to keep them alive. In Patton Boggs’ case, the savior was Squire Sanders. The point of these deathbed marriages is not to build abstract “synergies” but to restore confidence. A merged firm has more partners to absorb the damage of departures and cover fixed costs. Struggling law firms are similar in this respect to struggling banks. At the height of the financial crisis in 2008 and 2009, almost every struggling bank desperately sought a merger partner. This is how we ended up with the odd combination of Bank of America and Merrill Lynch. A merger is a classic way to stop a run.

Beyond these solutions, which are all within the control of a firm and its management, there are also broader solutions in public policy that would require a reform of existing law. One public policy solution would be to eliminate the rules requiring law firms to be owned by their partners. England, Wales, and Australia all recently began permitting law firms to be owned by investors, and in these countries investor-owned law firms now take a large share of the market for personal injury litigation and other types of personal legal services (see “How Regulation Is-and Isn’t-Changing Legal Services”). Investor ownership would powerfully diminish the risk of a run by diminishing lawyers’ sensitivity to decline. The risk of runs alone might not be a sufficient reason to permit investor ownership. But it is one reason and should become part of a more complete analysis of investor ownership.

Another solution is to permit restrictions on partner withdrawals. This is perhaps a more realistic possibility than investor ownership. The United Kingdom has long allowed restrictions on partner withdrawals, and elite corporate firms in the United Kingdom frequently retain partners’ capital contributions on withdrawal and force them to sign noncompete agreements as a condition of admission to the partnership. These withdrawal restrictions raise the cost of withdrawal, making departures less likely even when profits decline. It is perhaps no coincidence, then, that no large law firm in the United Kingdom has ever collapsed. Like investor ownership, though, withdrawal restrictions have many drawbacks. Although withdrawal restrictions would reduce the odds of runs by making it costlier to withdraw, they would also lock lawyers into unhappy work relationships and prevent clients from hiring the lawyers of their choice.

The ties that bind

When we look closely at the swift and violent collapses of law firms like Dewey & LeBoeuf and Heller Ehrman, one fact becomes undeniable: this is not normal. Many businesses suffer financial problems, but almost none blow up with the extraordinary force of law firms. If we want to understand why a law firm collapses, we need to understand not just why it suffered financial problems but also why it was so fragile in the face of these problems.

My answer is structural. Law firms are fragile because (1) they are owned by their partners and (2) these partners can freely withdraw. Partner ownership weakens a firm because it forces the remaining partners to suffer when another partner withdraws. Partner ownership creates financial incentives that encourage partners to follow one another out the door.

There are several ways to stop these financial incentives from wrecking a firm, but one of the most important is to strengthen nonfinancial commitments. Informal bonds like friendship, loyalty, and trust can hold a firm together even in the face of financial decline.

Partner ownership thus presents a paradox. Even as it weakens financial ties between partners and their firms, it can strengthen nonfinancial ties. At its best, the experience of working together as co-owners can cultivate a sense of friendship, loyalty, and trust. The lawyers who run law firms can sometimes feel like more than just employees—they can feel like true partners, bound together by values and deep commitment. The trouble, though, is that partner ownership does not merely cultivate values like friendship, loyalty, and trust; it also depends on them. Without these values, the financial incentives created by partner ownership can become too weak to sustain a firm. Partner ownership cuts the steel chains of contract and replaces them with leather cords of friendship and loyalty. These leather cords can bind strongly. But if these cords are ever cut—if all partners care about is money—then partner ownership, instead of binding a firm together, can become the very force that blows it apart.

John Morley is a professor of law at Yale Law School. Questions and comments can be directed to [email protected].