Brand in the legal industry is often an underutilized and neglected asset. Brand plays a hugely important role in developing and maintaining a successful law firm.

In every buying decision, both the firm brand and the individual practitioner or team brand come together, to differing extents, to offer a promise to the client: the promise of quality, of specialized subject matter expertise, of an expected price or a certain style of working. These expectations are set through a mixture of historical experiences of working with (or against) the firm and its lawyers, from peer opinions, and from the manner in which the law firm presents itself at marketing and business development touch points.

The more the firm’s people—those who represent and promote the firm every day—are equipped to reinforce the strengths of the firm, the stronger its brand will be. A strong brand leads to opportunities and a more sustainable future. A firm with a strong brand will receive more inquiries, and its approaches to prospects will be greeted more warmly.

A brand takes years, and often decades, to build in such a slow-moving industry as law. Buyers are inherently risk averse, and as a result many are resistant to making changes in their legal advisor. Buyers need convincing if they are to move from safe, historical choices to newer, different options. But the market is starting to be disrupted, clients are more willing to try something new, and some firms are already feeling the pressure. This comfortable existence is not going to last.

Law firms need to take control of their destiny, become more current in their brand proposition, and fight to protect their market share. Few firms pay attention to their real brand position in the market, choosing not to invest in understanding how they are perceived and being left in the dark as to what threats may lie ahead and what barriers may stand in the way of reaching their desired market position.

A firm with a strong brand will receive more inquiries, and its approaches to prospects will be greeted more warmly.

This article explores the role of brand in the legal industry, how the firm and individual lawyer brands interact, and ways in which clients distinguish firms from one another, thereby forming the basis on which firms can build differentiation. It also looks at the competitive landscape and the challenges of building a stand-out brand in such a crowded industry—and how this differs around the world. The article also examines the accounting industry to learn from the world’s leading professional services brands and how the science of marketing segmentation could be deployed to enable firms to gain competitive advantage. And it offers practical tips to custodians of legal brands to help them facilitate the success that each of their firms deserve.

Over the past 10 years, Acritas has been conducting a global telephone survey of senior legal buyers at large organizations. In total, more than 20,000 individual contacts have been interviewed. By keeping core questions consistent, along with the geographic and sector spread of interviews, Acritas is able to benchmark trends year to year with statistical confidence. Data of this scale and quality is unrivaled in the legal industry. This article draws on many of the research findings observed.

The Takeaway

Take control of your brand. How the market perceives you and how widely you are known will play a significant role in determining the opportunities presented to you and your firm. Determine how well known your brand is among your target market of clients and prospects. Understand your current brand drivers and what needs to change to reach your aspirational brand. Move in the direction of clients’ evolving needs rather than hanging on to the past. Address the weaknesses inherent in the industry. Your brand will play a large role in determining your future success. Take care of it.

Brand as a strategic tool

Brand is more than vanity; it is a strategic tool that can help drive growth, profitability, and overall firm performance. To understand the role of branding, it is important to start with the fact that a brand exists for every firm. A brand enables people working at a law firm to have a collective identity. This identity is likely to go way beyond a name alone and will usually be associated with one or more different attributes, which can be positive and/or negative. For example, “Best at M&A, but Expensive,” “International and Large,” “Aggressive Litigator,” and “Regulatory Experts” are all brands. These perceptions are generated by external stakeholders. Sometimes they may be inaccurate. Sometimes they may be spot-on. And often they are somewhere in between. The point is, however, that the collective perception of your target market is brand. And in a crowded market such as law, this collective identity will determine your short-term success.

Brand should be an ongoing investment.

There are critical points in a firm’s evolution where it is particularly important to pay attention to your brand. These usually relate to some kind of change where the market needs to be updated to realize the full potential of your new offering and how it can meet clients’ needs. Examples of triggers include a new office location, a new practice area or product, mass lateral hires, a new system, or a merger.

For firms that are constantly developing their practices, brand should be an ongoing investment. To evolve the market position to a new level requires serious investment and a smart, long-term brand strategy.

Major events can also be a trigger to reposition your firm as responding to a change in the market. Examples include the start of the recession and the recent Brexit vote. Many firms across the world have used Brexit to reinforce their English law capabilities and offered guidance to clients and prospects in how they can navigate the likely consequences.

Qualities of a leading brand

A leading brand has a number of different qualities. All qualities are important in their own right, but it is the commingling among them that ultimately defines the overall brand.

- Brand power—the firm is well known and recalled spontaneously above others. This is important because you want your firm to be one of the first to pop into a client’s head when a legal need arises.

- Brand affinity—the recognizable qualities of the firm are appealing to its target market, and the firm’s value proposition is a likable one.

- Brand consistency—the firm has an authentic brand promise and delivers a consistent experience across all its practices and offices.

- Brand advocacy—clients are proud to use the firm and will recommend it to their peers.

- Brand differentiation—the firm is seen as distinctive from other firms, which allows it to stand out and rise above the market.

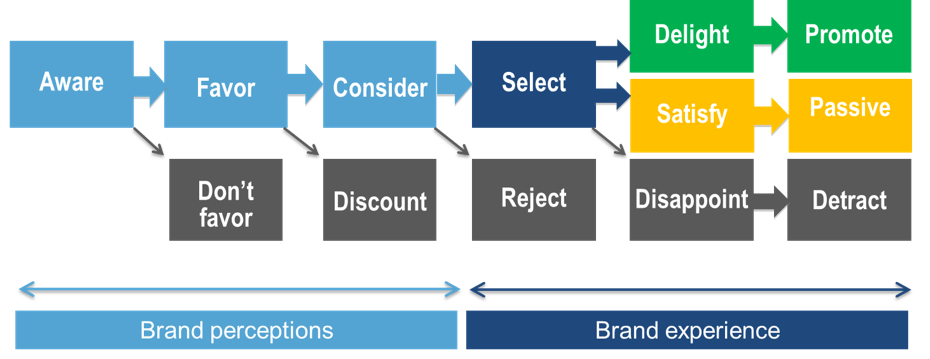

The brand cycle

As the relationship develops between a prospective client contact and a firm, it moves through different stages. The ultimate goal is to move a contact from being cold and unaware of the firm to being an active client and advocate. Unfortunately, the movement isn’t in one direction, and a less-than-satisfactory experience can cause a contact to drop outside of the cycle or, at worst, become a detractor (someone who shares negative opinions of the firm). It is important to remember that contacts are individuals, and even if they are not a key client now, or in a senior position, they may move to become an important contact. Therefore, at all times the client experience should be carefully watched over. As with all of us, a negative experience can taint the perception of a brand for many years. It is better to turn business down than to deliver an inferior brand experience.

Brand drivers: Six factors

Awareness. The drivers of top-of-mind awareness are most often related to client contact. A regular work flow will mean client contacts regularly receive work communications, such as e-mails or phone calls—this all helps to ensure the firm remains top of mind. Having said that, the average client works with 16 firms, so this will not automatically ensure you are top of mind every time a piece of work comes up. The client is not going to call all 16 firms. This is where effective marketing and business development activity can help to keep the firm top of mind, relative to the other firms on the roster. Substantive knowledge-based marketing is most effective in the client’s eyes, but the more subconscious effects of advertising, sponsorship, and press coverage can also be effective, even though the client may not recognize or value this activity.

Networking is another effective route at driving up awareness, particularly with noncurrent clients. This includes meeting at industry conferences or seminars and keeping up connections with alumni or personal contacts in the industry. Networking, in its broadest sense, accounts for 11 percent of awareness recalls.

![Drivers of awareness. Q: What made [firm] come to mind?](https://clp.law.harvard.edu/wp-content/uploads/2022/10/Figure2-1-2.png)

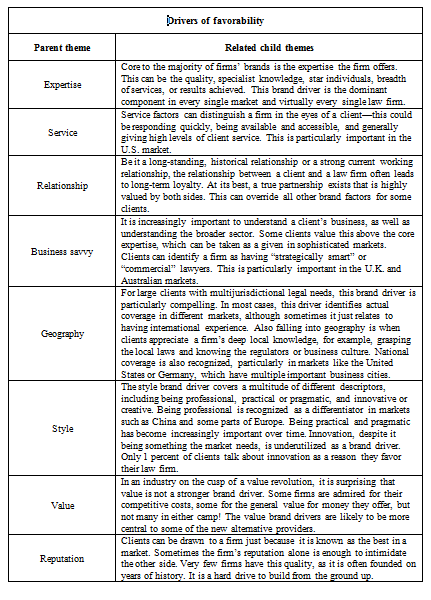

Favorability. The drivers of favorability, affinity, or simply “likability” are more complex. Having analyzed more than 50,000 reasons that a client has favored a particular law firm over the past decade, eight overall “parent” themes have consistently emerged, which each break down into a number of “child” themes. Most law firms have similar brand drivers. Very few deviate from the typical pattern, which provides a huge opportunity to stand out and drive competitive advantage—to be the Ritz-Carlton of hotels, the Goldman Sachs of investment banking, or the Starbucks of coffee shops.

It is interesting to note that the drivers of “favorability” map almost identically to the drivers of “recommendation,” which as identified earlier is the ultimate goal for every client contact. Therefore, why clients and prospects favor your firm is critical to unlocking your brand power.

![Drivers of favorability and recommendation. Q: What drives your favorable perception toward [firm]? Q: What does [firm] do that makes you highly likely to recommend it?](https://clp.law.harvard.edu/wp-content/uploads/2022/10/Figure3-1-2.png)

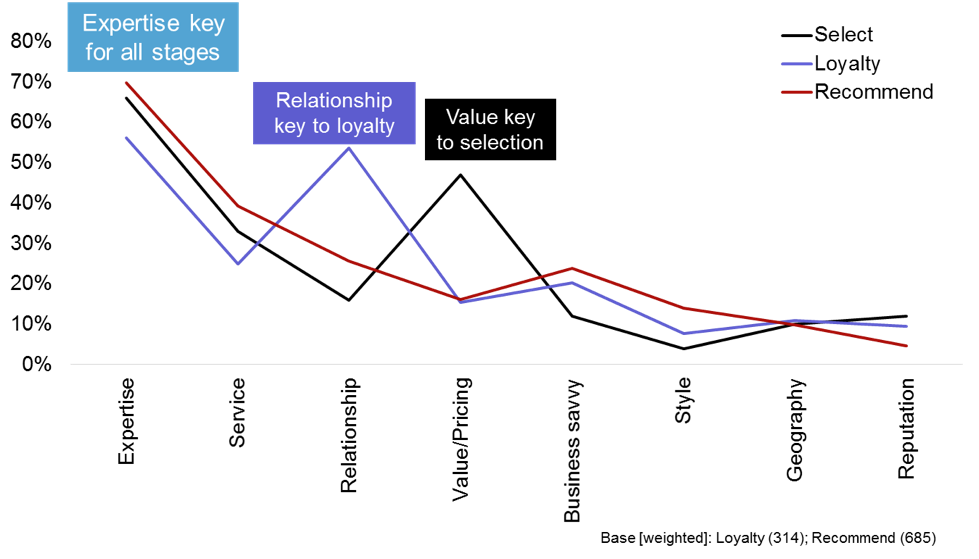

Consideration. Drivers of consideration, the stage that follows favorability in the brand cycle, vary according to the work type. If there is a multijurisdictional component, then international reach becomes the dominant driver, followed by expertise and relationships. For top-level M&A or litigation, however, the expertise and experience the firm is perceived to have is key, closely followed by relationships.

Selection. When it comes to looking at drivers of selection, suddenly value for money moves up to become the second most dominant factor. Clients have generally established who has the expertise and experience to do the job, so it now comes down to who can deliver the best value—or the price-to-quality ratio Starbucks required for the work.

Satisfaction and loyalty. The later stages of brand relate to the actual brand experience. This is where drivers of satisfaction and loyalty come into play. Starting with client satisfaction, being able to understand, manage, and meet expectations is one of the key enablers to delivering a “perfect 10” performance. Meeting expectations correlates more strongly than quality of legal advice with high satisfaction scores. Effective communication also correlates very strongly. It is extremely important that firms instill a process of formalizing client feedback to ensure that the brand experience matches up to the expectations formed during the early stages of the brand cycle. Without this feedback loop, issues can’t be addressed and service standards are unlikely to match the preferences individual clients have. For client loyalty, the strength of the relationship is key and features alongside delivering the expertise required; in other words, the firm has proven it can achieve the right results in the right way (see “Speaker’s Corner“).

Recommendation. As noted earlier, the drivers of recommendation, for promoters, match almost identically to the drivers of favorability. At the recommendation stage in the life cycle, “business savvy” plays a slightly stronger role than it does for the favorability stage. This includes understanding the client’s business and industry and generally being strategic and commercial. Likelihood to recommend is an extremely important metric and one that the leadership of law firms and client relationship managers alike should evaluate every year. It is a stronger indicator of future income and sustainable growth.

Marketing and brand development

Some firms are super brands. They have more well-known brands than their size should dictate. These firms tend to be recalled as much for their specific market reputation or marketing as they do for general client contact. The weaker brands, in contrast, are purely known for the client contact and aren’t getting that same marketing uplift.

Legal marketing encompasses a whole range of different activities (see “The Past, Present, and Future: Business Development in Law“). The highest level includes activities such as advertising, sponsorship, or press coverage. The midlevel includes knowledge-based activities such as legal updates and seminars. The ground level is the way lawyers interact with stakeholders and how effective they are at articulating the key positioning messages of the firm; in other words, “selling” the firm. The best approach is undoubtedly where all efforts are working together, reinforcing and demonstrating the same messages. This holistic approach ensures the brand message is being heard both directly and subconsciously, emphasizing authenticity—“we deliver what we promise.”

The larger and more complex the firm, the larger the marketing effort needs to be, although economies of scale do come into play. At some of the large global firms, marketing department sizes run into the hundreds. They have segmented the target market into a matrix approach and structure their teams along these matrices—marketing and selling along geographic and sector lines, as well as practices. Large marketing departments will also have niche experts in different marketing specialties, including communications, business development, clients, analysts, CRM, web, and, increasingly, heads of brand. All these specialists work together, following a defined marketing strategy and execution plan, under the guidance of the chief marketing officer and his or her senior team. They are professionals, creating the strongest possible brand platform for the lawyers to go to market.

The individual practitioner brand

Since 2015, we have been collecting individual lawyers whom clients perceive to be exceptional and exploring the reasons why.

The reasons clients favor particular “star” lawyers reflect almost exactly why they favor firms—with one key difference. When it comes to a stand-out individual, how commercially savvy he or she is plays a much greater role—whether the lawyer can deliver practical and pragmatic advice and be a business advisor rather than simply a legal expert.

One trend worth considering is that elite firms are now used less often for general day-to-day work, often because of price pressure. This means their lawyers have less contact with the client, which is diminishing their understanding of the client and the related business. This may have an impact on their ability to be commercial and strategic in their advice, sticking more to the pure legal aspects.

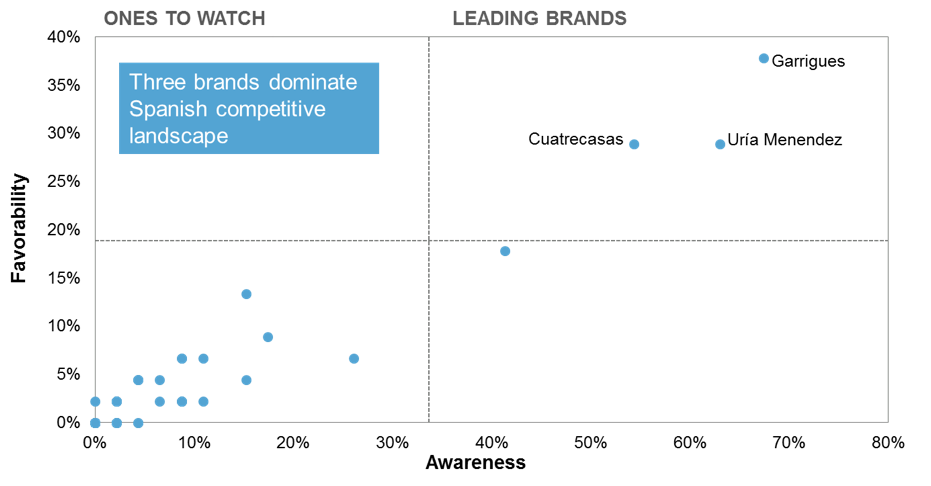

Differing brand density in differing markets—the United States and Spain

Over the past 10 years, Acritas has developed its own barometer—the Brand Density Index—to assess how fragmented a market is. By placing every brand mentioned in rank order, highest to lowest, we count how many firms it takes to get to 50 percent of the mentions. Spain has the lowest density, at 4 index points. The U.S. market has the highest, at 36 index points.

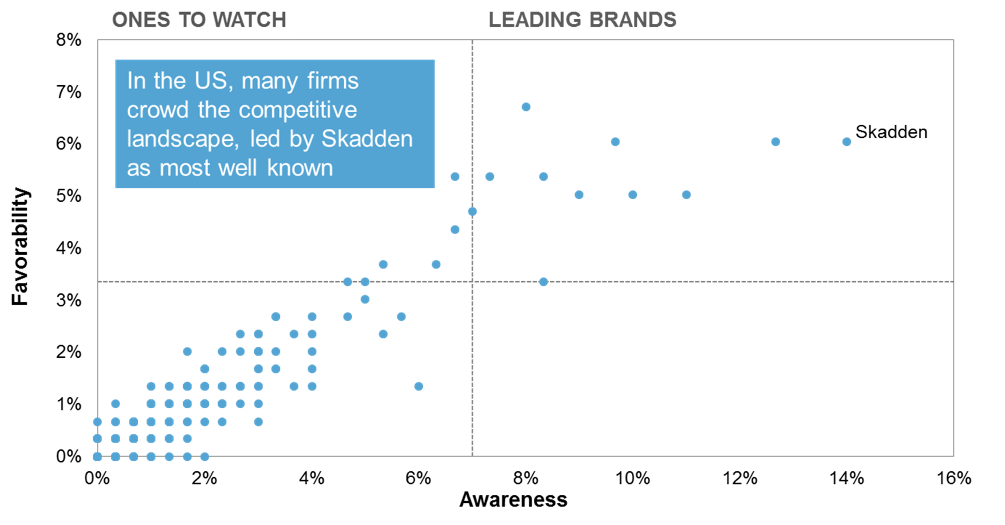

No single market is more fragmented than the U.S. market. This market is the most dynamic, and we have seen the competitive landscape change dramatically over the past decade. There are so many law firms fighting for recognition in clients’ minds, which is amplified by the fact that clients tend to use more firms in the United States than their counterparts do in the rest of the world. They are much more likely to pick and choose many different firms for all their different legal needs. When we look at the highest levels of spontaneous awareness—“the first five law firms to come to mind”—the most recalled firm in the United States is Skadden, with 12 percent of the 600 clients interviewed mentioning the firm. It is closely followed by many others, with more than 600 firms being mentioned in total. Interestingly, in 2007 Skadden achieved 19 percent spontaneous awareness, a huge lead over the second most recalled firm. However, this lead has gradually diminished over the past 10 years.

In Spain there is a vastly different picture. The competitive brand landscape is dominated by just three firms: Garrigues, Uría Menéndez, and Cuatrecasas. Garrigues, the most recalled brand, has an impressive 67 percent awareness, although this has also come down from what it was in 2008, when we first measured legal brands in the Spanish market. In 2008 Garrigues achieved 89 percent spontaneous awareness. As more firms pick up their game in their approach to marketing, it seems they are taking brand share from the traditional leaders.

Most countries tend toward the Spanish market shape, but not quite as extreme. For example, in China the brand density is 6, where King & Wood Mallesons leads with 61 percent awareness, and in Germany the brand density is 8 index points, with Freshfields Bruckhaus Deringer leading with more than 50 percent.

When results from all the different legal markets around the world are combined, the overall global picture is very different from what you find in any individual geographic market. It doesn’t feel “right” to many people when they first see the global landscape. The firms that dominate have the broadest geographic reach; the top five in particular have brand equity in each of the Americas, Europe, Africa, Middle East, and Asia Pacific. These firms lead and push most of the other firms back into the lower left quadrant, or the chasing pack. The brand density of the global market is higher than the United States, at 45.

Comparisons to other industries

In other professional services industries, the brand landscape is more like the Spanish legal market. A small number of dominant brands exists, reflecting market consolidation, polarizing typically around a few global players, a small number of more midmarket firms, and then lots of small firms, usually niche to a particular locality or service line.

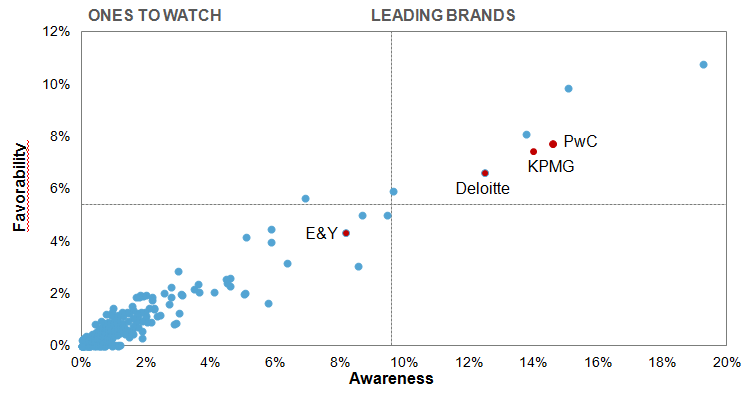

In the accounting industry, the Big Four dominate (see “The Reemergence of the Big Four in Law”). Their unmatched scale and international reach are critical to their brand success supported by an expert approach to all disciplines, including account management and marketing. There is much to learn from the models of the Big Four accounting firms, and therefore it is no surprise that law firms are hiring more ex–Big Four firms to help implement some of their approaches and drive change.

As the legal industry continues to consolidate, a similar pattern is likely to emerge for the legal competitive brand landscape at a global level, creating a more polarized picture. However, due to the nature of conflicts, it is unlikely it will ever be as low as four main players. Based on measuring trends over the past decade, we would predict between eight and 10. Few firms will be able to commit to the investments required to create a truly global presence and all the supporting IT systems needed to provide a seamless service.

Demand and supply side change

Consolidation is one of the main driving forces behind the change in the shape of the global legal market. Some regions have seen more dramatic change than others. Firms that have completed a series of mergers and combinations, effectively “buying in” brand equity, have sometimes seen big increases in their global brand rank as a result.

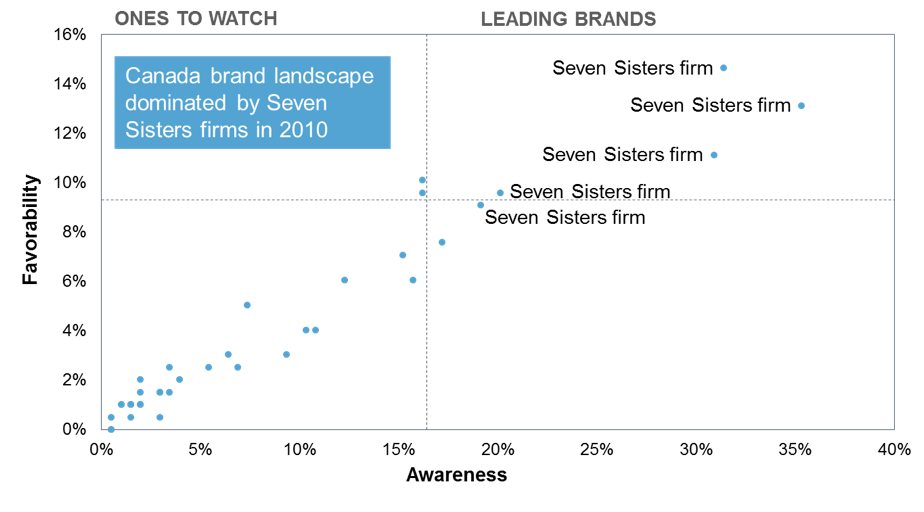

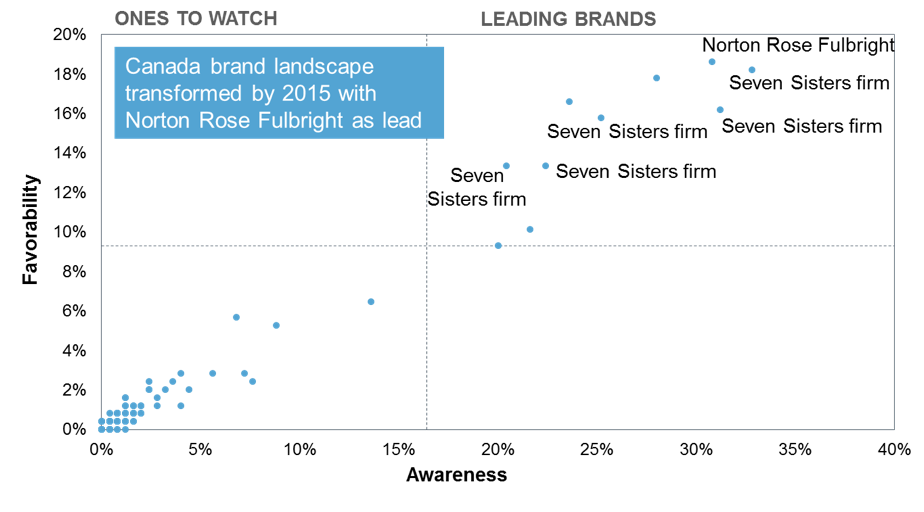

One of the most impressive of these landscape-changing mergers was Norton Rose Fulbright when it entered the Canadian market. It first combined with Ogilvy Renault to gain breadth and depth of services and coverage in the main cities. The firm then combined with Macleod Dixon, giving a “high-end specialist” feel to the Canadian presence as well as associated energy expertise to the Calgary presence. Two other factors helped this become a transformational play. It was the first Canadian firm to have a very international footprint— first to market always creates attention—and second, the marketing execution around the combination was extremely effective. The investment level included high and eye-catching adverts placed in key locations—for example, airports—drawing attention to the new firm among the intended target audience. Not one client or prospect of the firm was left uninformed about the new international services the firm could offer.

This literally catapulted the firm to disrupt the leading brands quadrant, traditionally owned by the reputable and long-established Seven Sister firms. Subsequent mergers—Dentons with Fraser Milner Casgrain, DLA Piper with Davis, and more recently Gowlings with Wragge Lawrence Graham & Co—have continued to reshape the brand landscape, which now bears little resemblance to 2008, when Acritas first measured the Canadian brand landscape. None of the subsequent mergers or combinations has yet been as transformational as the Norton Rose Fulbright move. Another interesting change is that some of the stronger national firms not traditionally included in the Seven Sisters grouping have also surged ahead into the leading brands quadrant, demonstrating how the market is looking beyond the more elite firms to gain more value from their legal spend.

When looking at the global brand landscape, consolidation has had a major impact. The global business law firms, such as Baker & McKenzie, DLA Piper, Norton Rose Fulbright, Hogan Lovells, Dentons, and King & Wood Mallesons, have all grown through a mix of mergers and combinations, mass lateral hiring, and general organic growth. These “megafirms” have been created to respond to clients’ evolving needs, as demand from multinational clients has become more multijurisdictional and more value conscious.

Some of the first international firms were perceived to be expensive, often lacked the breadth of services across smaller countries, and at times did not have the appetite to conduct more price-sensitive, less sophisticated work. These firms have seen their brands drop from positions that were far above the level their size should dictate. They were the original superbrands, and some still are, but their brand equities have dropped to be more in line with their size.

Globally, the more traditional elite firms have also tended to see their brands erode over time. Clients can no longer justify premium prices for much of their work. It should be noted, however, that in recent years some of the elite firms have attempted to respond to these market forces by investing in process efficiency, low-cost centers, and other forms of technological support. We do see evidence that those that innovate are seeing their brands beginning to grow.

One should also make clear that a small number of notable exceptional elite firms have not changed their way of working but have instead clarified their position as handling only the most elite work. In short, they are differentiating themselves by moving up the value chain by focusing only on highly sophisticated legal work. Arguably, only the genuine “best in class” firms can deliver on this strategy.

It cannot be stressed enough, as firms look at their strategy moving forward and how they reflect this in their investments and brand messaging, that the direction must align with the clients’ evolving needs. This is critical to achieving brand success.

Market segmentation

In consumer goods industries, market segmentation is an essential marketing tool. Customers are segmented on the basis of attitudes, behaviors, and needs, and then products and associated brands are fine-tuned to meet each group. Think about something like potato chips, with hundreds of different flavors, shapes, and levels of salt. All concepts are developed and market-tested to find the perfect offering and the group they most appeal to. Similarly, in aftershave or perfume, the brand is developed to match the scent, creating the right image, messaging, and ambassador to promote through.

In the legal industry the practice of segmentation isn’t particularly well adopted. Some firms segment by industry. This is a good start, but generally it is just in a marketing sense and does not usually pervade the structure or main governance of the firm. Once you work with the firm, the services aren’t necessarily different dependent on the sector being serviced. Can you imagine an organization like Thomson Reuters being able to serve the legal industry so well if it didn’t structure its organization by vertical? All its products and services for law firms and legal departments fall within the legal division, which in turn is broken into large law, small law, corporate legal departments, etc. A different product suite and marketing approach is adapted for each segment.

If law firms could start to segment their clients by considering their size and scope, needs, attitudes, and preferences, could they could steal a march on competitors by offering a proposition that better matched those clients’ needs?

Finding your perfect match

Your firm may be large enough to cover all segments, but this is most likely to result in developing a more general offering that appeals to all types of clients. To be able to hone your strengths to match a specific type of buyer is more likely to result in developing a proposition that fits more tightly to that specific buyer’s needs.

The first two steps for any firm evaluating its brand proposition have to be:

- Ascertaining what your clients and your people believe to be your strengths, particularly those that are more distinctive to you than other firms. It also helps to understand the types of characteristics your clients really value and any needs they feel currently go unmet, which your firm could look to address in the future.

- Establishing the clients you aspire to grow and attract more of

Ideally, there will be a match between your distinctive strengths and those that appeal to your focus segment of the market. If not, you have to either refocus on a slightly different segment or develop your strengths to better match the original segment.

One might define six types of purchasers of legal services:

- Modern buyer: more objective approach to buying, value conscious, likely to involve professional procurement, uses metrics to evaluate pitches and performance, expects alternative fee arrangements and added value services in the mix, has panels in place, may bundle multiple matters under one contract

- Traditional buyer: more relationship approach to buying, brand conscious, perception of quality paramount, focuses on results, tends to select firms matter to matter, less price sensitive

- Small internal department: likely to outsource broad range of work types, requires support in knowledge management and skills development, needs help in covering absences such as maternity, needs to be kept abreast of legal developments

- Large internal department: likely to outsource certain types of work, volume, very specialist, or to add capacity for large disputes or transactions

- Female buyer: interested in lawyers who are commercial in approach and have business understanding, expects strong communication, reporting regularly on cost, more price sensitive

- Global buyer: more sophisticated buyer of nondomestic work, able to segment work as to what requires real local presence, needs support in keeping abreast of legal and regulatory change across multiple markets, requires international client team approach

Future of brand in the legal industry

The past decade has produced some interesting trends in the competitive landscape in every jurisdiction. In general, elite firms have seen their brand halos diminish to have brands more in line with their rightful size. Firms that offer more competitive pricing, with “good enough” quality, have strengthened. Firms that have merged have sometimes created stronger brands by combining the brand equity of the legacy firms. Firms that have built serious and credible international platforms have addressed a largely unmet and growing need for multijurisdictional advice at all levels and seen their brands rise as a result.

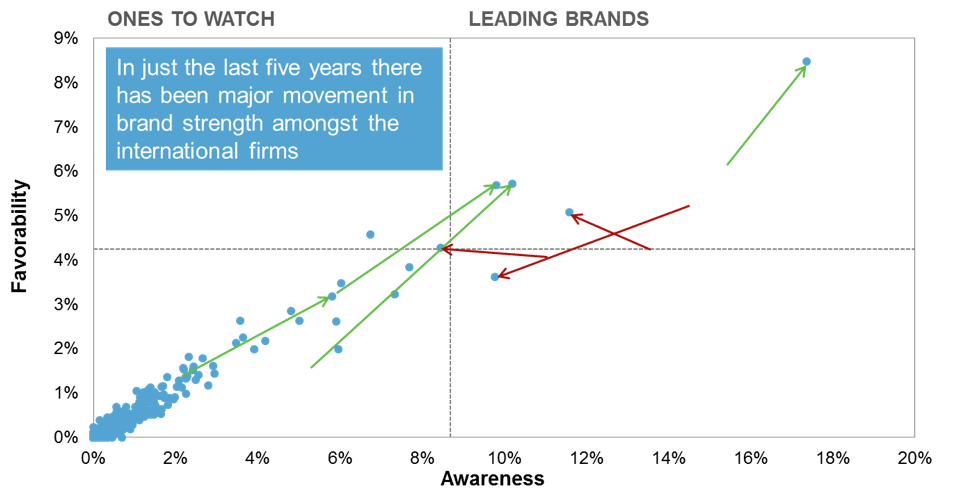

The map below shows the movement in the global competitive brand landscape over the past five years, from 2011 to 2015. The sample size, more than 1,000 on each occasion, was almost identical in terms of geographic spread, organizational size, and industry makeup.

By extrapolating the trends that have occurred in the past five years, we can gain a sense of the competitive brand landscape in 2020. This analysis assumes the market forces will continue, although perhaps at a slower rate. We have assumed clients will continue to push for more value from their law firms, organizations will continue to internationalize across more markets, regulation will continue to intensify, and law firms will continue to consolidate.

The extrapolation has allowed for the fact that many of the traditional elite firms are starting to respond to the drive for more value. It is expected that some of these firms will reverse their declining brand pattern in the years ahead. Some already have, and others have defined a more clear elite proposition, aiming only for the work that is worthy of a best-in-class investment.

To date, we have measured only the brands of law firms. Given the high rate of startup legal services providers disrupting the market, plus the established multidisciplinary professional services providers investing more in their legal services divisions, we will be capturing the most recalled and the most favored legal brands moving forward. It is important to broaden the lens and take all types of providers into the competitive set; after all, they are fighting for a piece of the same legal budget.

The map below shows a hypothetical competitive landscape, drawing on the data extrapolation and building in the predicted brand strengths of the Big Four accounting firms.

The under 50s

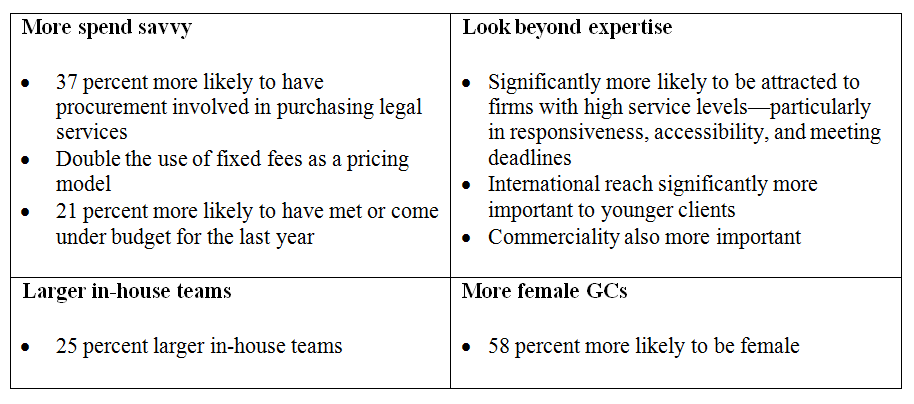

Perhaps a more interesting way of looking to the future is to ignore those over 50 and review how those under 50 currently see the competitive landscape and why. The buying behaviors differ by age group. Younger groups appear more spend savvy, look more broadly than the core expertise a firm offers, are more likely to be led by females, and are more likely to have larger in-house teams in place. The behavioral profile suggests buying will become an even more objective, value-driven process and clients will require much more systemized project management and specified service standards.

These demographic and behavioral differences influence the types of firms clients respect and are attracted to. While the over 50s see firms like Skadden, Wachtell, and Latham & Watkins as the ones to have the greatest board room credibility, the under 50s are most likely to list Baker & McKenzie and Clifford Chance at the top. Some of the differences in brand recall are because the United States has the oldest client profiles, whereas Asia has one of the youngest profiles, particularly China. But even within the United States, younger generations are drawn more toward firms like DLA Piper as being more in line with their buying needs.

In terms of industry differences, technology clients have a younger profile versus an industry like health care, which has one of the oldest profiles. DLA Piper and Baker & McKenzie are stand-out brands in the technology sector.

It is important for all firms to understand the demographic and behavioral profiles of their client base and then how their brand profile marries up. This should not be a one-off exercise. Regular reassessment is key as the pace of change in the industry speeds up.

Key success factors

Law firm leaders and chief marketing officers have tremendous responsibility as custodians of brands in setting the right strategic direction at the firm and ensuring the brand platform is optimized to deliver the intended results. While the market has not yet been hugely impacted by the disrupters, with a global average of 4 percent of total external budget going to alternatives, this figure is likely to increase dramatically over the next decade, threatening the existence of the many firms who are resistant to change.

The new alternative suppliers are not only doing things cheaper, they are also offering cost certainty and taking a big data, technology-driven approach, which will result in a more effective work product and better reporting, which, in turn, leads to continual improvement.

The market is also being infiltrated by large established organizations from different industries who have deep pockets and a greater willingness to make long-term investments. The Big Four accountancy firms are growing their legal operations across the world to be substantial competitors. And when artificial intelligence really comes into force, we will see large technology companies also competing for legal spend.

There is a window of opportunity for firms to take control. Traditional law firms have an enviable advantage. Clients don’t like change, they are risk averse, and they recognize and value the technical expertise law firms nurture, which costs time and money to build. This gives firms time to develop and hone propositions that will respond to the new pressures clients face and will lead to competitive advantage. But this is time limited. Clients’ patience will run out.

A leader’s role is to set the right vision for your firm, make it come to life, and communicate this to all stakeholders, including the people in your firm and the external market.

Building a successful brand

Five key success factors in developing a brand

- Begin with a clear vision of what the firm is—and what it could become.

- Develop smart strategies based on systematic listening to clients, your own people, using market intelligence and taking an honest view of genuine strengths.

- Have strong and diverse leadership to gain buy-in from the partnership and see through the execution of the strategy.

- Commit to the investment required—for the long term.

- Give the necessary support to the partners to change their behaviors to make the proposition authentic.

In developing a market-leading proposition, firms would benefit from ensuring the board (or the equivalent group that is developing and driving the firm’s strategy) is made up of perspectives as diverse as possible to ensure the firm is not suffering from a singular perspective: different ages, genders, ethnicities, and nationalities; people with industry experience; and other professionals including technology, strategy, marketing, finance, and HR. By bringing different natural skills sets together, the result will no doubt be superior, assuming a strong leader can take ultimate control.