After several years of weak demand following the Great Recession, it’s a good time for a fresh look at the strategic options available to Big Law and take into consideration many new entrants to the market that were not a competitive threat in 2009. Developing good strategy is hard work, particularly in a partnership because partner acceptance is critical to successful strategy implementation. Once a developed strategy is “adjusted” to achieve the necessary consensus, it’s often difficult to uncover the original intent of major strategic planks. It’s not surprising that many firm strategies are condensed into profitability goals and geographic preferences. In many cases, even though a formal strategy may exist, firms often default to opportunistic and incremental strategic actions based on serendipitous events. Put another way, if a good opportunity comes along, they will take it. This approach has merits but is perhaps better described as good tactics. In addition, a “watered down” strategy is always accepting of just about any reasonable tactical move.

One of the core elements of building a good strategy is a clear understanding of the playing field—a difficult task in such a fragmented legal market. In the United States, the market for outside legal counsel is estimated to be more than $275 billion, with the largest firm (by revenue) commanding less than 1 percent of total market share. The size and fragmentation of the marketplace, combined with clients’ willingness to disaggregate legal services, has attracted many new competitors that must be considered in every strategy. The bottom line: a law firm’s strategy must contemplate its own position relative to the competition, thereby making market segmentation a prerequisite to strategic planning.

How do we describe, or segment, this marketplace to determine the current positioning of a firm attempting to build a coherent business strategy? There are many ways to look at your competition and, by juxtaposition, your firm. Typical segmentation can be done by practice area, geography, industry knowledge, and perhaps an “expertise driven” versus a “process driven” approach, or what the consulting world might call “methodologies.” Quality is also potentially a key differentiator, but “quality” as a metric is often difficult to quantify. Others characterize the marketplace using financial metrics, such as revenue or profitability. Bruce MacEwen, president of Adam Smith Esq. and a well-known industry consultant, describes yet another approach. In his book, A New Taxonomy: The Seven Law Firm Business Models, MacEwen offers potential major firm archetypes—such as global players, capital markets, kings of their hill, boutiques, and integrated focus firms—as a means of differentiation.

How do we describe, or segment, the marketplace to determine the current positioning of a firm attempting to build a coherent business strategy?

As the above makes clear, law firms attempt to differentiate themselves from one another in a host of ways. For present purposes, the point is less which metric or method one operates under but rather which strategy of differentiation one uses. Just as a military general needs a map of the battlefield, law firm leaders—not to mention general counsel—can benefit from mapping the legal terrain of their marketplace. Moreover, and more urgently, because the traditional competitors are likely to be joined by new entrants to the industry, including the Big Four (see “The Reemergence of the Big Four in Law”), it’s important that firms understand where the competition is today, which direction those competitors are heading, and where new competitors are likely to emerge.

Axis of Differentiation

I suggest that market segmentation is best approached from the perspective of the client. Many factors go into a client’s decision regarding which firm to hire, but the most significant may be the value of compensation paid for the work done. In other words, the price a client is willing to pay for the work—from complex and sophisticated work to more routine, commodity-level work—is one of the most important factors differentiating one firm from another. The financial yardstick most readily available to make this measurement is a firm’s revenue per lawyer (RPL).

RPL is a difficult metric to adjust: You have revenue—typically cash—and you have lawyers—lawyer head count—and both are difficult facts to change.

Although RPL is an imperfect measure due to varying productivity levels and geographic dispersion, it’s a good place to start in assessing the client’s view of the relative value of legal expertise each firm provides. This measure is also helpful to firms that are attempting an exercise in differentiation because it is reasonably isolated from the manipulation that so often distorts other measures, such as profitability per partner, leverage, or net margins. For example, if you would like to increase the profitability-per-partner metric, redefine the number of lawyers you deem equity partners and profits increase. Likewise, capitalizing expenses rather than expensing them can improve profitability-per-partner as well as net margins. But RPL is a difficult metric to adjust: You have revenue—typically cash—and you have lawyers—lawyer head count—and both are difficult facts to change.

The second useful element of segmentation is a firm’s ability to “push” its value proposition into the marketplace. A small but highly valued firm may receive top dollar for the work it does but still have little impact on the overall market or its competitors due to its size. Today, market share is often overlooked because of the significant fragmentation in the legal market, but one doesn’t have to look far to see similar professional services markets where market share is critical because firms have more than 200,000 practitioners. Therefore, a useful second axis of differentiation is simply the size of the firm as measured by its total number of lawyers. This measure is also readily available.

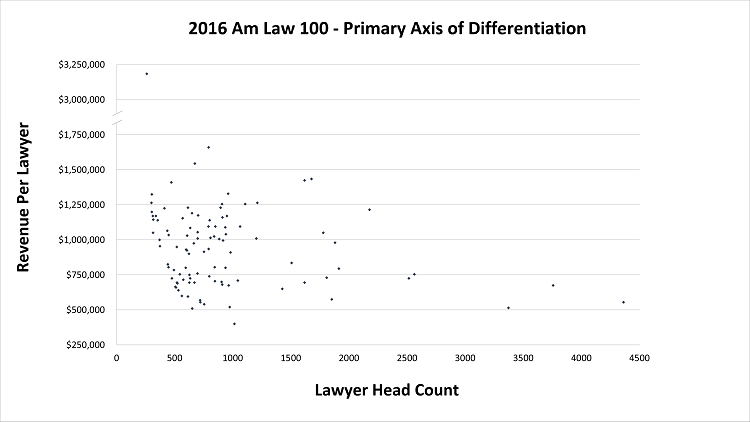

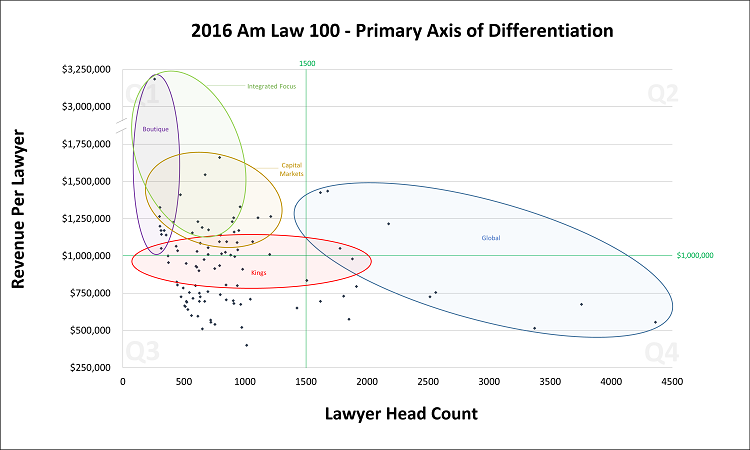

With these two measures—available for hundreds of U.S. firms—we can build a matrix that I call an “axis of differentiation” (Figure 1). Using the 2016 Am Law 100 firms as a starting point, we place RPL on the y-axis and the total number of lawyers on the x-axis to build a simple scatter plot of the relative positioning of each firm. We can then plot the firms’ relative position on the plot on the basis of these two metrics: RPL and lawyer head count.

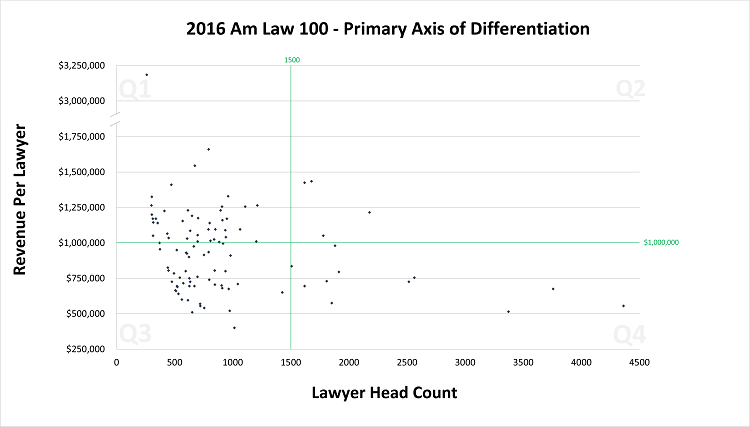

Of course, this depiction lacks context, which can be added by defining a “large” firm and a “high RPL” firm. By doing this, we can segment the Am Law 100 firms into four quadrants to provide meaningful differentiation among the firms in each group. These definitions need not be precise as they can be modified to further define your competitors. For illustrative purposes, we’ll define a large firm as one that has more than 1,500 lawyers and a high-RPL firm as having RPL greater than $1 million. Figure 2 displays these two parameters, therein creating four quadrants understood along North-South and East-West dimensions.

In the most general sense, a little less than half of the firms in the sample (45) have RPL of more than $1 million, leaving 55 firms with RPL less than $1 million. Meanwhile, 85 firms out of 100 have fewer than 1,500 lawyers, with just 15 having more than 1,500. Again, while the RPL and lawyer head count parameters are somewhat artificial, they nevertheless help provide context to the fact that significantly more firms have fewer than 1,500 lawyers, while RPL is more equally divided (see Figure 3).

Examining the firms in each quadrant, we start to see similarities in their businesses that are mirrored in their reputations and brands in the marketplace. No one quadrant is necessarily preferable to another in terms of a business model, but from a tactical perspective the operational metrics and behaviors are likely different in each quadrant.

In looking at each of these quadrants in more detail, it is important to stress again that no one quadrant or position is better or worse than the other. The quadrants are simply tools to help leaders understand their overall marketplace placement—and therein a tool for driving strategy. Put differently, the question one should be asking is, How did I get into the Northeast or Southwest? Was it part of overall strategic intent? Or was it simply a case of happenstance?

Each strategic planner can likely describe a profile or assign his or her own label to these four groups when characterizing the firms in each quadrant. One may also adjust the quadrants by changing the lines defining each quadrant for a specific strategic purpose. No matter where the lines are drawn, this axis of differentiation provides an effective way to depict the current competitive landscape as you prepare to address the key question at the heart of most planning: Where do we want to compete?

Analyzing desired market positioning with these metrics raises the question, Which quadrant is the best? This is where strategic thinking and each firm’s specific intent comes into play, because the correct answer is that a viable and profitable business can survive in any quadrant. That makes all the quadrants desirable—depending on your strategic objectives. In other words, there is no right or wrong answer. It is all about where your firm wants to compete.

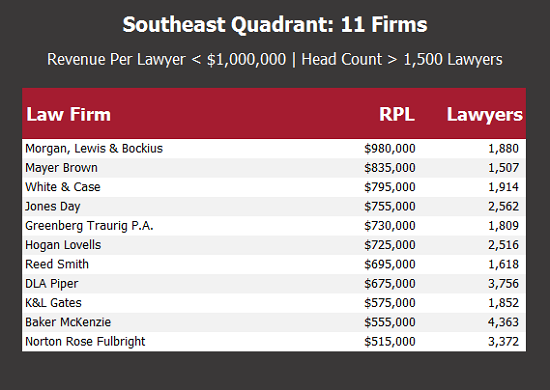

To illustrate this point, you might ask firm leaders, “If you could run a firm in any of the quadrants, which one would you prefer?” You would get preferences for each based on market knowledge, professional identity, ego, or any of a seemingly endless number of valid reasons. For example, some would like to be “big” or “everywhere” regardless of the type of work because it’s a lot of fun to travel to many different countries—the Southeast of the axis of differentiation (11 firms, or 11 percent of the sample)—even if that means RPL of less than $1 million. There is also prestige in managing a firm like this, and it matches the “bigger is better” point of view. For an empirical take on this phenomenon, see “Foreign Firms in China: Looking Beyond the Hype,” in which Rachel Stern and Su Li of the University of California, Berkeley School of Law argue that U.S. law firms often open, and keep open, outpost offices in China despite their relative unprofitability as the term global has become synonymous with sophistication and market dominance—and being global means being in China.

Interestingly, many firms in the Southeast that prefer that quadrant over the Northeast may believe there is not enough sophisticated, high-value work in the latter to sustain their relatively large practices over time. As one managing partner from a Southeast firm told me: “We want to be everywhere.” So they merged with several firms to increase their geographic scope even though the strategy might not drive up RPL.

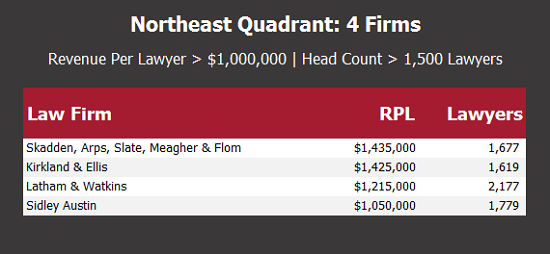

Offering a slightly alternative point of view are those preferring the Northeast quadrant. Firms in this area are often convinced not only that “bigger is better” (or at least that size has some relationship with value and client service) but that there is also plenty of high-end work to be taken from other firms to sustain their growth across a large geographic footprint. This last point is critical. To the extent that the firm’s strategy is to remain in the Northeast quadrant, growth in lawyer head count—whether via geographic expansion, a merger, or some other means—without a corresponding growth in RPL risks moving the firm into the Southeast. While it is difficult to draw causal conclusions from this data, one can postulate that those in the Northeast quadrant are most likely making an internal calculation that RPL and lawyer head count are positively and linearly correlated. Of the four quadrants, the Northeast may be the hardest to break into, with only four firms (and 4 percent of the sample) occupying the space.

Different from those in the East quadrant are those in the West quadrant—firms with fewer than 1,500 lawyers. Southwest leaders, which represent the plurality of the sample (44 firms), may like their geographic markets, which are typically limited, and value serving midmarket clients with regional relationships that have probably endured over decades. A critical question is whether firms in the Southwest quadrant are there out of choice—it is their explicit strategy—or whether they are in the quadrant because they are unable to break into the North or the East.

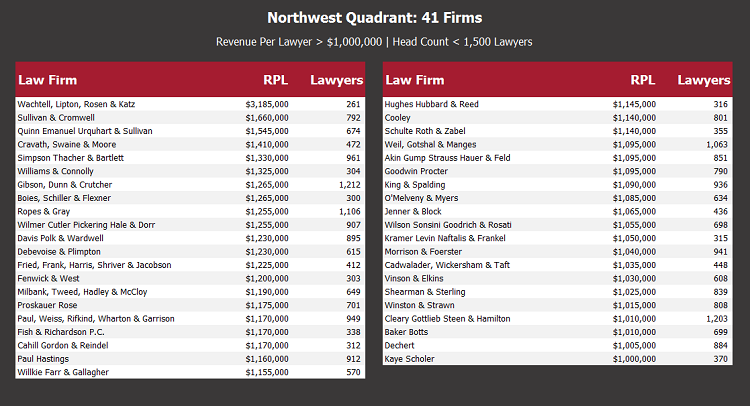

The Northwest quadrant firms, which are the second most common in the sample (41 firms), are typically engaged in critical, high-end work for a limited number of often global clients. These firms tend to have a much narrower practice focus that is as deliberate as it is critical to maintaining their brand.

No matter which perspective dominates your firm’s thinking, strategic planners will find it helpful to ponder this question—Where do we want to compete?—from different angles when it comes to identifying the market position of any firm, where they see the future of their own firm, and where they see the future of the industry. It also allows strategic planners to contemplate the tactical actions required to move from one quadrant to another and to assess the feasibility of such a move. Above all, the ability to understand both current market position and desired future positioning helps management make tactical and strategic decisions that move the firm in a direction with strategic intent rather than drifting along, as so many firms do, from year to year.

Differentiation of the New Taxonomy

Another way to develop the context around differentiation is to overlay Bruce MacEwen’s law firm business models on this landscape (Figure 4). MacEwen describes “global players” as firms with a geographic presence spanning over three continents, deep capabilities across economically privileged countries, and comprehensive practice offerings. These firms, he notes, are complex to manage and often experience cycles of large demand swings. His “capital markets” firms are headquartered in global financial centers, have a history of being tethered to a major bank/investment bank, and enjoy high margin practices, with growth most likely resulting in financial dilution. “Kings of their hill” firms are typically headquartered in nonglobal cities, cater to sophisticated upper- and middle-market corporations, and know their home turf very well through long-term personal relationships. “Boutique” firms do one thing exceptionally well, which could be high- or low-end work; are typically led by charismatic leaders; and are easy to brand even while focus is often difficult to maintain. Lastly, MacEwen defines “integrated focus” firms as those designed to serve a target market with a clear value proposition to clients, often with an industry orientation.

In his book, the results of a survey of lawyers identifying their own firms by name and categorized by model yielded the following placement of firms with somewhat predictable results.

Figure 4

New competitors necessitate new strategies?

With this framework in mind, firms should consider several factors when answering the question, Where do we want to compete? Some considerations are internally driven by the culture of the firm and the personal preferences of its ownership and leadership. Other considerations are driven externally and are primarily defined by the competition. But so far we have considered only other competitors from the Am Law 100. Competition should be defined more broadly to include others, such as Am Law 200 firms, “new” entrants that may not even be law firms, and the major accountancy networks, which are now growing quickly in the legal marketplace outside of the United States. Consideration should be given to not only where they compete now but where they are most likely to compete in the future.

The Am Law second 100 firms are predominantly resident in the Southwest, and when added to the 44 Am Law 100 firms in that quadrant, that space starts to look crowded. The newer entrants in the marketplace, such as legal processing outsourcers, virtual law firms, and organizations providing technology-oriented legal services, are taking advantage of clients’ willingness to disaggregate legal work in favor of lower costs and “process-oriented efficiencies” to capture a measurable percentage of a worldwide marketplace estimated to be more than $500 billion. They range in scale from small to very large and will probably first appear as competition to traditional law firms in the Southwest and Southeast quadrants of our axis of differentiation.

The most significant new entrants are likely the Big Four accountancy networks, now building large legal and professional services networks in Europe, Asia-Pacific, Latin America, and Africa. Their participation in the global legal market is well documented by David Wilkins and Maria Jose Esteban in “The Role of the Big Four Accountancy Firms in the Reconfiguration of the Global Market for Legal Services” (Harvard Law School Center on the Legal Procession Working Paper, 2016-01). The question for U.S. firms is twofold: Will they eventually compete in the U.S. market and what type of work would they likely choose as an entry point? The recent takeover of General Electric’s tax department (600 lawyers and accountants) by PwC provides some insight to this question. U.S. firms with a significant presence worldwide have been dealing with these questions outside of the U.S. market for several years.

Strategy over time

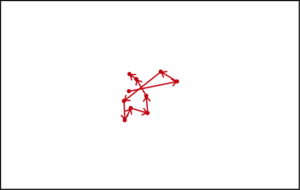

Global law firm leaders have a lot to think about as they craft strategies for their firms, and this framework can be a good starting point for those discussions. If you want to know how you arrived at your current location, plot the movement of your firm on the grid over the past 10 years. For many firms, strategic intent is obvious; for others, less so. To that end, the plots below each represent a single firm plotted on the axis of differentiation over a 10-year period, from 2006 to 2016. Each point represents the firm’s positioning on the axis in a given year, and the arrows represent the direction of movement between the years. Taken together, the plots provide insight into strategy over time, which arguably is an even more important metric than where your firm stands in any particular year. It is essential to note what these charts can and cannot reveal. They can tell us what happened based on the data. They cannot tell us what was in the heads of the leaders of the firm. In other words, they cannot tell us whether the picture revealed was the goal or a case of (nonstrategic) happenstance.

If you want to know how you arrived at your current location, plot the movement of your firm on the grid over the past 10 years.

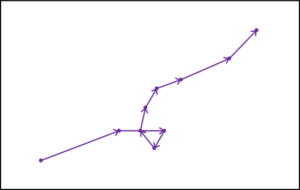

Figure 5 is a firm that appears to be in generally the same space in 2016 as it was in 2006. Without knowing the intent of the firm, one can logically infer a strategy of stability and maintenance simply by looking at lawyer head count by RPL over a 10-year period. The firm did not get much bigger in size, nor did its RPL grow significantly. This is no small task given that the period under examination involves the global financial crisis (GFC) and the massive impact that had to the entire legal services market (including massive downsizing across the industry). To be sure, we would still need to understand the firm’s actual strategy—for instance, was the stability the chart suggests the firm’s real strategic intent or was it simply an inability to gain traction in any direction? The axis of differentiation cannot answer that question, but it does provide a solid starting point for examining questions of firm strategy.

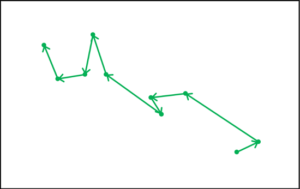

Figure 6 paints a different strategic picture from that of Figure 5. The firm depicted in Figure 6 appears to have employed a strategy of focus, significantly shrinking the size of the firm while increasing the sophistication of the work it does with a corresponding increase in RPL. Indeed, over the 10-year period the firm in question reduced its lawyer head count by approximately 40 percent while increasing RPL by roughly 30 percent. Again, whether this was happenstance or strategic requires more research, but it is hard to deny the clear movement toward the West quadrant.

Unlike the stability depicted in Figure 5 and the RPL growth in Figure 6, the firm in Figure 7 is merrily cruising along, gaining scale and sophistication, save for a brief interlude during the recession of 2008–2010. Indeed, apart from the shock felt across the legal services industry during the GFC, the firm has no sharp increases or decreases in either lawyer head count or RPL in any one year. To the extent that the firm’s strategy was to continue to move toward the Northeast quadrant, the numbers appear to support a job well-done.

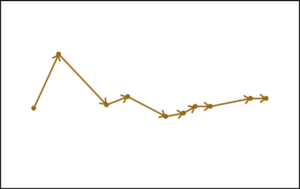

Finally, the Figure 8 firm appears to see scale as the most important aspect of its strategy. Over the 10-year period, the firm grew its lawyer head count by 65 percent while RLP remained flat.

Strategy for the future

Where can we go from here? If the data was available, plotting this segmentation specific to a geographic market would be the most useful to determine desirable moves within that market. Clearly, when looking at this data on a global basis, it is difficult to see the difference between running a law firm in the United States versus Eastern Europe or Latin America. Some firms may need to explore only one quadrant in the U.S. market and further subdivide that quadrant to gain additional clarity within their preferred area of concentration. However one does it, the critical takeaway is, If you were running a law firm, where would you want to be and how would you get there?

This type of information is useful not only to law firm leaders building strategy but to lateral partners contemplating a move to a new firm as well. Understanding the target firm’s strategy and competitive positioning should be of paramount importance since many laterals seem to move from one firm to another with the intent of gaining a better “platform” for their practices. This perspective may also be helpful to law students deciding what type of a career they would prefer. This article has largely focused on questions of strategy based on analysis of lawyer head count and RPL, but underlying all this are real firms and real lawyers. Whether you are a law student deciding which firm to join or a seasoned lawyer looking for a new firm, the questions addressed above go straight to the heart of the vitality and culture of any law firm. And you ought to make sure you know where the firm is—and where it is going.

At the time of writing, Robert J. Couture was the executive director of McGuireWoods, a law firm headquartered in Richmond, Virginia. He is currently a senior research fellow at the Center on the Legal Profession.