Historically, innovation has been something of a blind spot for the legal profession. As David B. Wilkins, Lester Kissel Professor of Law at Harvard Law School and faculty director of the Center on the Legal Profession, often quips: “Law is a lagging—not a leading—indicator of change. After all, in the common-law world, you can’t say anything new unless you have proven definitively that someone else already said it. That’s called precedent!” Understandably, this aspect of legal work has not primed the law as a bastion of innovation. The profession’s long history as a highly regulated business—with lawyers controlling most of that regulation—is, of course, another contributing factor to its aversion to new ideas.

Yet, as we have documented elsewhere in The Practice (see “The Global Age of More for Less”), the world is undergoing massive shifts brought on by macro forces like globalization, the rise of information technology, and the blurring together of traditional fields of knowledge such as law and business. These changes are impacting the entire world economy, and there is little reason to expect that they would not also impact law. The legal profession is therefore facing a challenge. On the one hand, law has always been a conservative discipline, which has historically lent itself to stability (and this should not be too easily dismissed—quoting Wilkins again, it is called the “rule of law” for a reason). On the other hand, the massive changes taking place globally are driving new ways of thinking and new systems to go with it. The legal profession finds itself stuck between these two forces—continuity and change. Central to this challenge is how the profession might innovate in ways that align it with modern circumstance while also maintaining the values associated with its core principles.

Historically, innovation has been something of a blind spot for the legal profession.

The term “innovation” is often used without strict attention to its actual meaning; it’s more a buzzword meant to signal an embrace of change than a term rooted in what any given change entails. To help tackle this issue, this article brings the nebulous term of “innovation” down to earth by unpacking what it means on a conceptual level. We look at what innovation is—and isn’t—from two distinct vantage points. First, we speak with Jodi Goldstein, executive director of the Harvard Innovation Labs (for more on the “i-lab,” see sidebar below) to understand how an entity explicitly designed to nurture innovation operates and what characteristics successful innovators tend to have in common. We also hear from Barry Jaruzelski, senior partner with Strategy&, PricewaterhouseCoopers’s (PwC) strategy consulting business, and one of the original authors of the Global Innovation 1000 study, to consider innovation through an organizational lens. In the end, we aim to offer a multifaceted conceptual view of innovation and how individuals and organizations are grappling with it.

Defining innovation

Jodi Goldstein knows a thing or two about innovation. After beginning her career as a consultant at General Electric, she spent a few years at a venture capital firm investing in early-stage companies before earning her MBA at Harvard Business School in 1996. Goldstein spent the next 15 years on the management team of multiple tartups, including PlanetAll, Send.com, and Drync, among others. Then in 2011, Goldstein got in at the ground level of another new initiative: the Harvard Innovation Labs (“i-lab”).

Given all this background, and now as the executive director of an “innovation lab,” we asked her: What does innovation mean to you? As she explains, innovation ought not be a catchall term:

Everyone has their own interpretation of what innovation is, and from my perspective, it’s about more than just novel ideas. Innovation goes further. It’s about novel ideas that provide real value and can be executed. Think of the difference between invention and innovation. An invention is a novel idea, but there might not be a market for it. An innovation is a novel idea that solves a problem. So from my standpoint, and what I try to help our entrepreneurs solve for, is what value does an innovation provide? Is there a market? Is there a problem to be solved with that novel idea? Because ideas without a market and without a value proposition are useless.

Like Goldstein, Barry Jaruzelski has a unique perspective on the concept of innovation—particularly in the context of organizations. Jaruzelski has worked as a consultant around corporate strategy for more than 30 years. After earning his MBA at Columbia Business School in 1987, he joined the commercial consulting arm of Booz Allen Hamilton, which later became Booz & Company, which later became Strategy& when it was sold to the global professional services firm PwC. Since 2005, Jaruzelski has also authored the annual Global Innovation 1000 study, which tracks how top companies are innovating.

“I always say, ‘You ask 10 people and you’ll get 12 definitions of innovation,’” he jests. “It’s one of those frequently misquoted words, because it’s just become an explanation for everything. And by definition, it’s ‘good,’ even if we don’t quite know what it means.” Jaruzelski and his team view innovation much the same way as Goldstein and the i-lab—whether and to what degree a new service delivery method or a new product solves a customer problem. And, as Jaruzelski describes somewhat ironically, this is not necessarily a new way of thinking. “Some of it goes back to what the service industry used to call ‘business process redesign’ in the ’80s and ’90s,” he explains. “After all, a lot of what we talk about as innovation is just redesigning how we do workflow, how we build something in a factory, how we provide customer service, how we update a bank account, whatever it might be.”

That there is so much misunderstanding around what it means to innovate, Goldstein attributes more to human nature than anything else. “People are inherently risk-averse,” she says. To be a true innovator, she explains, one has to be able to overcome that innate fear of failure—because failure is part of the process. “You have to be relentlessly listening to the market,” she adds. “You could have the best hammer in the world, but if no one’s willing to buy it, and it doesn’t provide value, what does it matter?”

Technology and innovation are not the same thing

Goldstein’s distinction between the utility of an idea and the idea alone extends to technology as well. While technology is often linked to innovation, Goldstein is clear that the two are not the same thing. She notes that technology is often a tool in the process of innovation, but to be innovative, tools need context. Does a particular technology help you accomplish something you were unable to accomplish before? Is what it accomplishes more helpful than what came before it? “Innovation is not about technology,” Goldstein says unequivocally. “It’s about the problem and the solution.” As she explains, innovators succeed off an unbroken focus on the market and the needs of customers. Otherwise, the risk of solving a problem that does not exist is always looming. (For more on the distinction between innovation and technology, see “Designs on the Law” and the redesigning of Hogan Lovell’s associate review process.)

You ask 10 people and you’ll get 12 definitions of innovation.

Barry Jaruzelski, senior partner with Strategy&, part of PwC

Jaruzelski draws a similar distinction between innovation and science. “There’s often been this view that innovation and science are the same thing, and they absolutely aren’t,” he emphasizes. “Science is an input. It’s a shelf of things you could pull from to solve a problem, but some of the greatest innovations often just use existing science and know-how in a different way.” Jaruzelski points to how corporations spend money in research and development, estimating that for every dollar spent on research, there are typically five or six spent on development. “You can’t do the development if the research doesn’t exist, but the research might be five years old or 50 years old,” he says. “Look at Apple’s Macintosh. There wasn’t new science there; there was new customer understanding being applied.”

Jaruzelski and his team were particularly interested in finding what aspects of innovation could actually be measured, eventually homing in on the relationship between companies’ investment in “new science” and their performance. By analyzing patent activity and other available data, they noticed a direct correlation between number of patents filed and R&D spending, but this did not extend to performance. “What we found is there is no statistically significant relationship between the extent of patents and corporate performance,” Jaruzelski notes. “So, if you want more patents, spend more money—you will get more patents. You will not necessarily get more performance. There’s no relation.” He explains:

The reason is twofold: Reason one is patents are a bit like novels. Very few are bestsellers. Most novels sell less than 5,000 copies, and patents are not all that dissimilar. And reason two is that patents may be a reflection of science and advances in knowledge, but science doesn’t equal innovation, because often the fact that you can do something different doesn’t mean there’s a market for it.

Artificial intelligence is often an unfortunate example where new science is taken to be innovative irrespective of the problem under consideration. “Many people think, ‘I’ll just use AI and machine learning and apply it to this problem. And that, in and of itself, is going to be innovative,’” Goldstein remarks. “That only works if AI or machine learning is an enabler; if it allows you to find a solution that you wouldn’t otherwise have found.” Goldstein gives the example of how doctors determine the best antibiotic for certain infections. Whereas traditional methods are often based more on a combination of trial and error and professional experience, a new AI-enabled startup working with the i-lab is increasingly using sophisticated artificial intelligence methods that allow for more-precise diagnoses more quickly, and therefore more-targeted treatments. To Goldstein’s overarching point, AI was the necessary tool to improve a particular process—it was an innovation.

There’s often been this view that innovation and science are the same thing, and they absolutely aren’t.

Barry Jaruzelski

In the end, what matters most is not what the tool is capable of but its usefulness in solving a specific problem. A tool, process, or system is innovative if it is more useful—viz more cost-effective, more time-efficient, simpler and/or easier for users to navigate, or otherwise able to produce better results—than what people were using before. Thus, just because machine learning is relatively new and technologically sophisticated, it may not be innovative. The key to innovation is: Where does it get you?

The Harvard Innovation Labs

As executive director of the i-lab, it is part of Goldstein’s job to have this deep, nuanced view of innovation. The i-lab sits within Harvard but outside any one school, and all Harvard students are welcome—not just those from the business or engineering schools—which is important in creating what Goldstein calls an “authentic community for innovation.” Meant to provide students with the mentor support and physical space they need to see their ideas through, the i-lab also offers more-structured programming in the form of workshops, hackathons, entrepreneurs-in-residence, startup weekends, and more. Each year the i-lab sees roughly 10,000 students pass through, whether to attend a workshop, meet with an adviser, or just use the space. Typically, that number correlates to about 200 different ventures incubating at the i-lab annually and somewhere in the area of 1,200 in total since the i-lab first opened its doors, but Goldstein does not dwell on these figures.

“We focus on inputs, not outputs, and that’s really key,” says Goldstein. She explains:

It’s not about venture creation. It’s about education. So we want people to experiment. We want them to fail. We want them to push themselves out of their comfort zones. And with that, there must be no consequences for failure. There’s no grades associated with it. The students own all their own IP. We don’t take equity. Harvard does not want to benefit from any of the ideas that are coming out of the lab, and that creates alignment between myself and my staff and the students who are there experimenting. For so many of the students, they say it’s the one place on campus that they really feel safe. And in order to innovate, in order to really push yourself outside of your comfort zone, to be willing to fail, you have to have that psychological safety.

Goldstein cautions, however, that there is no typical i-lab experience. “What we understand about innovation is that there are no straight lines, and everyone is going to enter in a different stage of the journey,” she says. “And you know, I always laugh when students walk in, and they want the step-by-step process because that’s what they’re used to. But it doesn’t exist. We don’t ever want to create a step-by-step process for entrepreneurship and innovation, because that would be inauthentic.”

Nevertheless, when a student comes in looking to put an idea in motion, the i-lab takes a customized milestone-based approach. The first thing advisers at the i-lab will do is help students identify milestones and help them start to think through how they might reach them. And, while overall the i-lab aims to keep their touch light, they take a more heavy-handed approach when it comes to students’ accountability to their own goals. Advisers might ask: How are you doing? Have you validated the questions you had at the outset? Where did that lead you? Have your milestones changed? “We find this works very well because it’s not one-size-fits-all,” says Goldstein. “It’s very different from, say, a traditional accelerator program, where they’re picking people who are all at a similar stage of development, and they want to spit them out the other end in a similar place as well. And that’s not our goal.”

Challenges to innovating

Of course, innovation is not unique to startup companies. Indeed, a growing number of professionals and leaders in established organizations are keen to foster more innovation in their ranks. These organizations have already achieved a measure of success by virtue of their own existence, size, and impact—which is precisely why they face additional challenges when it comes to innovation. Goldstein notes larger organizations often tend toward incremental change. “That’s generally how the incentive structure is set up,” notes Goldstein. She explains:

The safety, the low risk of failure, the nondisruptive outcomes—these all appeal to organizations because they are built to make incremental improvements to what already exists. That’s why it is hard to disrupt organizations that have been doing something the same way for a very long time. It’s difficult for the people in organizations to get on board. They might impede innovation because they have been successful operating within that existing construct.

In this context, the values and function of the i-lab are very telling. As Goldstein remarks, they want students to feel safe to fail. They want them to innovate in a space that is insulated from the consequences of failure to free their creativity and willingness to experiment. (As “Designs on the Law” notes, these are all themes of design thinking, which is an often-utilized technique in innovation.) With no grading or pressure to leave the i-lab—there is no semester limit for students to use the space—they are ultimately accountable only to themselves. “Unfortunately, organizations are not structured that way,” shrugs Goldstein. But, she notes, there is a moral to the story that organizations can pick up on. “When you look at organizations that have innovation centers, the ones that are successful are the ones that are completely outside of the organizational construct. They don’t have to worry about ROI. They don’t have to worry about any of the short-term metrics and measures of success that the rest does.” (For one clear example of what this can look like, see the case study of design thinking at Faegre Baker Daniels in “Designs on the Law.”)

What makes a difference?

This, of course, can be difficult to replicate at organizations like large law firms or major companies. At the same time, there are other ways such organizations have found to reap the rewards of innovation. Since 2005, Jaruzelski and his team at Strategy& have produced the Global Innovation 1000 study, which follows broad trends in how companies innovate looking at a sample that accounts for roughly 40 percent of global R&D spending. In the 14 years since the first iteration of the study was released, Jaruzelski notes that companies who perform best tend to have certain characteristics in common.

The safety, the low risk of failure, the nondisruptive outcomes—these all appeal to organizations because they are built to make incremental improvements to what already exists.

Jodi Goldstein

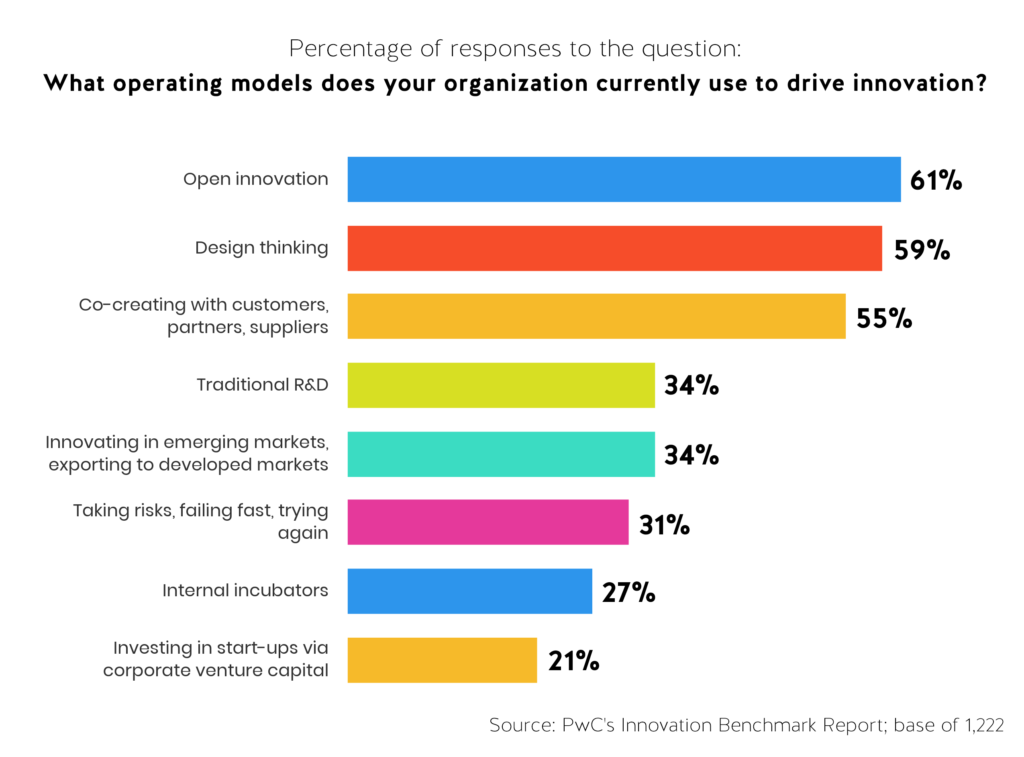

Deep customer engagement. Both Goldstein and Jaruzelski keep coming back to the same key to successful innovation: know the market. To do this really well, that means going so far as to understand how a product or service is received by the people who actually have to use it. And Jaruzelski makes a distinction between the customer and the end user. “Sometimes your customer is three steps removed from the end user,” he points out. “That makes a huge difference, and those who go out and try to understand their end user tend to perform far better than those who rely on intermediaries to do it.” This becomes increasingly important in the context of global markets, where the end user may be in a markedly different context from where a product or service is developed. And companies are changing how they read and respond to the market in an attempt to capture these details. PwC’s 2017 Innovation Benchmark Report found that many organizations are moving away from traditional R&D labs and toward more inclusive and collaborative innovation systems (see Figure 1 below). The Report writes:

Innovative companies aren’t going it alone. Instead, they’re pushing the boundaries of innovation both inside and outside their organizations by breaking down traditional barriers, tapping a much wider ecosystem for ideas, insights, talent, and technology, and incorporating the customer throughout the innovation process. More-inclusive operating models, such as open innovation, design thinking, and co-creation with partners, customers, and suppliers, are now all embraced ahead of traditional R&D, and by a wide margin—almost twice as many companies favor these models.

Alignment of innovation strategy and business strategy. There is no one prescription for how organizations should innovate. Indeed, the potential impact for any innovation initiative is largely dependent on the culture of the organization, where they are in the market, and where they are trying to go. That is to say, it depends on their strategy. (For more on crafting deliberate strategy in a law firm context, see Robert Couture’s “Postrecession Strategies.”) Why make a hammer when you are only looking for screws? Alternatively, what good is a hammer if no one knows you have it? According to Jaruzelski, companies do better when they have integrated innovation into their larger strategies, when there is a companywide culture that supports innovation, and, relatedly, when leadership supports and effectively communicates the importance of innovation.

Rigorous approach to new project selection. The importance of good strategy is critical, and often a business’s strategy comes down to what they choose to do and what they choose not to do. As Jaruzelski notes above, their research has found no meaningful connection between performance and R&D spend. “What matters is how you spend the money,” he says. “And the most successful organizations have a very rigorous process around project selection. We’re going to do X; we’re not going to do Y and Z.”

Innovative organizations: Three models

As Jaruzelski notes, innovation looks different depending on an organization’s strategy. He points to three distinctly different models of innovation—none of which is inherently better than the other, but the success of each requires alignment with larger strategic goals. Model one, which Jaruzelski calls “need seekers,” focuses most on end-user needs through a high level of investment. Or, as Jaruzelski puts it, “Need seekers invest substantially in end-user understanding to surface unarticulated needs.” Model two, “market readers,” focuses more on competitors than the end users. “This doesn’t mean you ignore the customer,” Jaruzelski notes, “but it’s more about where the center of gravity is.” Model three, “technology drivers,” instead pushes new technology out into the market on a more trial-and-error basis. “And I can give you three examples, all in the mobile phone market,” says Jaruzelski. “Apple with its iPhone (the need-seeker model), Samsung with the Galaxy (the market-reader model), and obviously Google with the Android (the technology-driver model)—all of them wildly successful, all of them following fundamentally different approaches to innovation and the role of innovation, and all of them very well aligned with the overall business strategy they’re pursuing.”

Operationalizing innovation

Few would accuse the law of being ahead of the curve when it comes to innovative thinking, but the need to innovate in the legal service industry has arrived all the same. In recent years, the profession has seen an uptick in investment in legal disruptors like LegalZoom (which received a $500 million investment this past summer) and Kira Systems (which received $50 million shortly thereafter). Governments are launching innovation initiatives of their own, such as Singapore’s Future Law Innovation Programme (or “FLIP”). We have even seen innovations around new organizational forms, such as alternative business structures in the United Kingdom (see “How Regulation Is—and Isn’t—Changing Legal Services”). These are all signs the profession is beginning to genuinely grapple with the innovation imperative.

The potential impact for any innovation initiative is largely dependent on the culture of the organization, where they are in the market, and where they are trying to go.

There is perhaps no greater sign of innovation’s march toward the legal profession than newly emerging roles within in-house legal departments and law firms charged specifically with leading innovation efforts. On the in-house side, these individuals are often called “heads of legal operations.” On the law firm side, they are often called “chief innovation partners.” There remain questions, however, around how effective some of these professionals can be when it comes to changing their organizations’ culture and work product (for more on this, see The Law Firm Chief Innovation Officer”). Indeed, despite beginning to pick up on the language of innovation, according to a recent Acritas Sharplegal survey, 73 percent of global general counsel reported seeing no innovation in their primary law firms. The Center on the Legal Profession has recently convened chief innovation officers and heads of legal operations at events in New York City and the Bay Area. Of particular interest at these events was alignment between the pain points clients experience and the innovations that firms and other organizations might come up with to both alleviate them and provide better value and quality of service. This ongoing research will appear in a future issue of The Practice in our series on innovation in the legal profession.

Coming up with solutions

What should lawyers make of innovation, the concept, at the end of the day? Through Goldstein and Jaruzelski, we gain a framework for understanding what innovation is—not just technology, not just science, and not just a tool, but a novel idea that stands as a solution to a problem. Their two vantage points also offer a nuanced and deeply valuable perspective on how innovators think and how they are best supported. While the legal profession may be a lagging indicator of change, these issues will become only more important to lawyers as the profession is forced to confront (and, in many ways, has already broken through) the massive change gathering outside its walls. In “Designs on the Law,” we expand on one innovative technique—design thinking—that has garnered significant attention in legal academia and law firms alike. The trick now for lawyers will be to think of innovation less in terms of the tool and more in terms of the problem at hand.