In the May 2017 issue of The Practice, I introduced an analytic to help differentiate the market among big law firms. Looking at the Am Law 100 firms, I established a playing field that enabled firm management to determine where they were positioned currently vis-à-vis their big law competitors. Exiting from many years of weak demand as a result of the Great Recession, 2016 was a good time for firms to reassess their strategies and competitive positioning. This analytic tool was a starting point to help management teams come to agreement on the direction and positioning of a large firm. It helps answer the question, “What kind of a firm do we want to be, and where do we want to compete?”

Surprisingly leaders often do not share a cohesive vision for a firm’s future. Even more surprising, they may not know that they aren’t on the same page because the strategic choices have not been clearly defined and debated.

Related content

Lead Article

Related content

Postrecession Strategies

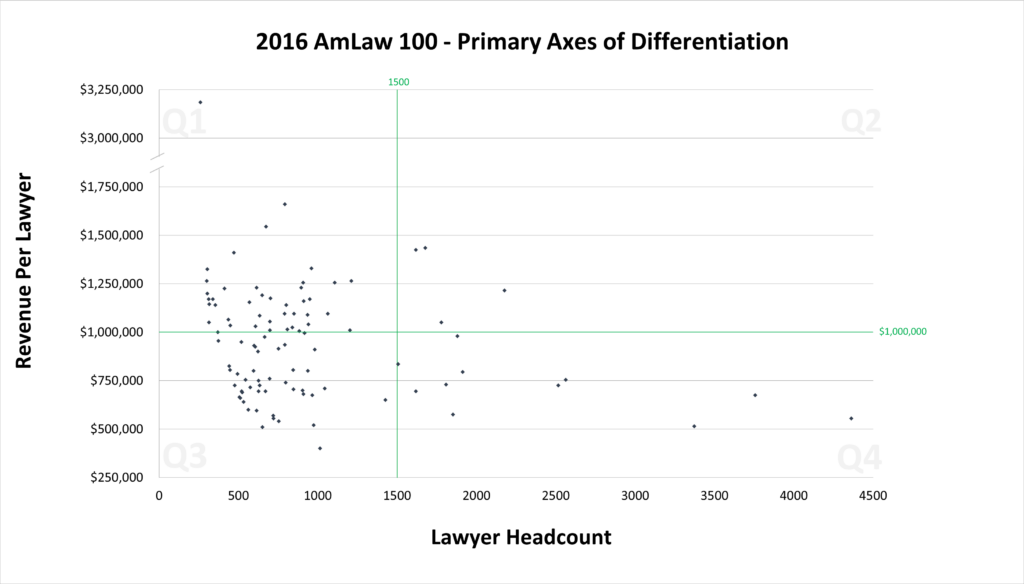

Using 2016 data from the American Lawyer, firms were positioned on an “axis of differentiation” that quantified the sophistication of the work they were doing and measured their ability to impact the marketplace based on their size. In this piece, as in my 2017 article, the amount a client is willing to pay for work acts as a proxy to understand the sophistication of that work. Six years later, it is instructive to look at where firms were then and where they are today after a multiyear period of very high demand growth for legal services. On the basis of the results of this analysis, leaders of a few firms who have made remarkable changes over this period were interviewed to understand how they guided their firms to their new positioning.

As a quick refresher from 2017

I suggest that market segmentation is best approached from the perspective of the client. Many factors go into a client’s decision regarding which firms to hire, but the most significant may be represented by the value of compensation paid for the work done. In other words, the price a client is willing to pay for the work is one of the most significant factors differentiating one firm from another. The spectrum from complex and sophisticated work to more routine, commodity-level work is vast and typically characterizes significant differences between firms. The financial yardstick most readily available to make this measurement is a firm’s revenue per lawyer (RPL). Although an imperfect measure due to varying productivity levels and geographic dispersion, it’s a good place to start in attempting to assess the client’s view of the relative value of legal expertise provided by each firm. This measure is also useful to a firm when attempting an exercise in differentiation because it is reasonably isolated from the manipulation that so often distorts other measures like profits per partner, leverage, or net margins. For example, if you would like to increase the profits-per-partner metric, redefine the number of lawyers you deem equity partners and profits increase. Likewise, capitalizing expenses rather than expensing them can improve the profits per partner as well as the net margins. But RPL is a difficult metric to adjust: you have revenue (typically cash), and you have lawyers. These are two difficult facts to change.

The second element of segmentation that becomes useful is a firm’s ability to “push” their value proposition into the marketplace. A small but highly valued firm may receive top dollar for the work they do but still have little impact on the overall market or their competitors due to their size. Today, market share is often overlooked because of the significant fragmentation in the legal market. But one doesn’t have to look far to see similar professional services markets where market share is critical because firms have more than 200,000 practitioners. Therefore, a useful second axis of differentiation is simply the size of the firm as measured by its total number of lawyers. This measure is also readily available.

Plotting the positioning of each firm on an x and y axis yields a scatter plot without much meaning, but context can be added by defining a “large” firm and a “high” RPL firm. By doing this, we can segment the Am Law 100 firms into four quadrants to provide meaningful differentiation among the firms in each of the groups. These definitions need not be precise as they can be modified to further define your competitors. For illustrative purposes, we’ll define a large firm as one that has more than 1,500 lawyers and a high RPL firm as having RPL greater than $1 million (which is the median).

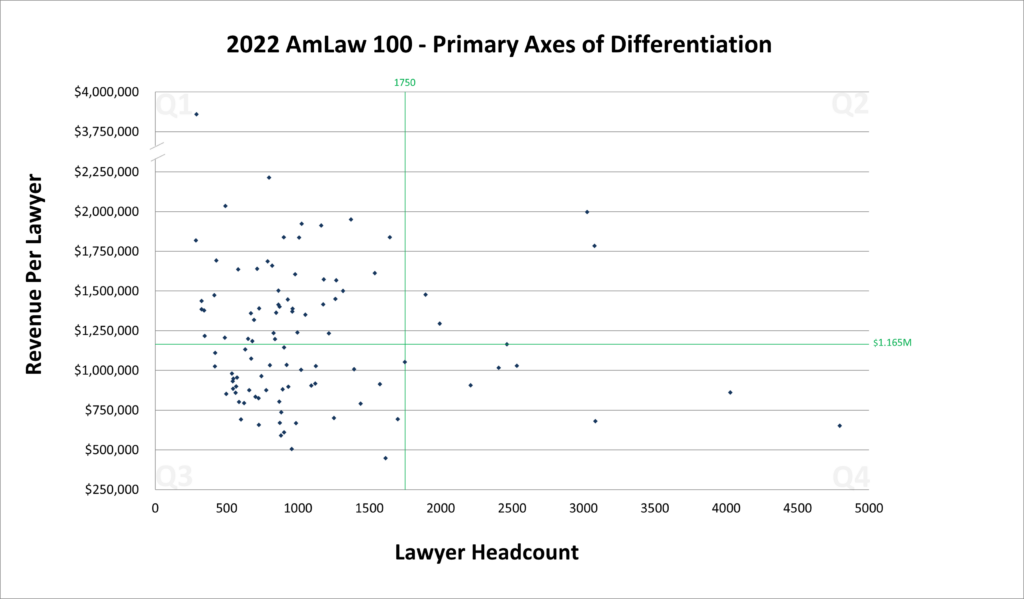

We now can fast-forward to 2022. The new, updated 2022 “axis of differentiation” chart is below, positioning each of the 100 firms. This depiction represents a “playing field” and positions each Am Law 100 firm on the chart representing their RPL and number of lawyers. It is difficult to recognize any meaningful use to this analytic until you put a firm name on each dot. At that point it becomes clear that “similar” firms by reputation are near one another on the matrix. Some firms are known for being “go to” firms for the most complex transactions or litigation, and others are known for their preponderance of “run the business” work that every corporate entity needs. Of course, these quadrants are entirely arbitrary, but adding them to the matrix helps bring understanding of the concept and context to the discussion. George Box, the British statistician, famously said, “All models are wrong, but some are useful.” Likewise, this model can be useful in discussing strategy with any firm leadership team. The quadrants for 2022 have been adjusted since 2016, reflecting the changes in median numbers over the six-year period. The lines of demarcation for each measure are updated to RPL of $1,165,000 and the number of lawyers to 1,750.

A quick review of the data comparing 2016 with 2022 would lead one to conclude that not much has changed when looking at all 100 firms in aggregate. Average RPL grew a total of 28 percent, which translates to a 4.2 percent compound growth rate (CGR)—a result easily attributable to rate increases. The average number of lawyers in these firms grew by a total of 16 percent, or 2.5 percent CGR. When looking at the median changes rather than averages, results are even more unremarkable. The median increase in RPL was 22 percent and median lawyer head count increased 17 percent over that time period. The firms that make up this group were also relatively stable with only four firms dropping out, which minimizes the potential for new players making a statistical impact.

However, beneath the averages and medians we can find some remarkable changes in positioning relative to the competition in individual firms, with the largest growth in RPL of 57 percent in one firm and number of lawyers growing by 87 percent at another. Because the respective changes in the median for these measures was 22 percent and 17 percent, these results represent an extraordinary performance by some firms and suggest significant events are at play that cannot be attributed to annual “drift” in the businesses. I suspect that management has defined and articulated concrete strategic actions, explained the reasons and logic for the transition, and is successfully executing their plans.

If we look closer at the top two movers in both categories (RPL and number of lawyers) by quadrant, some interesting observations can be made. The number in parenthesis is their performance in the second metric. So, for example, Paul Weiss had the highest RPL increase in the Northwest quadrant at 57 percent, and a 6 percent growth in number of lawyers.

NORTHWEST QUADRANT:

Revenue per lawyer:

– Paul Weiss: 57% (6%)

– Davis Polk: 56% (15%)

Number of lawyers:

– Goodwin Procter: 66% (37%)

– Cooley: 58% (38%)

Observations: Paul Weiss and Davis Polk intend to stay in the Northwest, and Goodwin Procter and Cooley may be making a play to move to the East while staying in the top half of the chart.

NORTHEAST QUADRANT

Revenue per lawyer:

– Latham & Watkins: 47% (41%)

– White & Case: 47% (29%)

Number of lawyers:

– Kirkland: 87% (40%)

– Latham & Watkins: 41% (47%)

Observations: Everyone is pushing the quadrant further to the Northeast. These are powerhouse players that also care about market share.

SOUTHWEST QUADRANT:

Revenue per lawyer:

– McGuireWoods: 53% (-5%)

– Holland & Knight: 42% (33%)

Number of lawyers:

– Womble Bond Dickinson: 79% (0%) (merger)

– Troutman Pepper: 79% (22%) (merger)

Observations: No generalizations here. McGuireWoods clearly slimmed down to get better work and push to the North. Womble Bond Dickinson merged two equals to push toward the Southeast, while Troutman Pepper managed to merge gaining scale and more complex work. These calculations are made using Womble and Troutman as the base firms.

SOUTHEAST QUADRANT

Revenue per lawyer:

– Hogan Lovells: 42% (1%)

– Jones Day: 35% (-1%)

Number of lawyers:

– Greenberg Traurig: 22% (24%)

– Mayer Brown: 16% (26%)

Observations: Hogan Lovells and Jones Day may be making a play to go north rather than build scale at this point. Mayer Brown and Greenberg Traurig appear to be taking a “steady as she goes” approach.

Related content

insight

Related content

Data in Detail: Leading the Way

While the data tells only a statistical story, to gain a deeper understanding of how some firms made extraordinary strides, I interviewed three of the firm leaders to discuss their thinking and operational execution of strategic objectives.

Bob Couture: Brad, your firm appears to have rapidly increased the complexity of the work you are doing for clients over the past six years as represented by an increase in RPL of 57 percent while the median within the Am Law100 firms was 22 percent. I recall a presentation you did in 2016 at a Bloomberg conference where you outlined your 13-point strategic plan for Paul Weiss. All the plan elements were important, but five of them stood out to me as integral to your strategy:

- Focus on five practice areas.

- Invest only in these five practices.

- Serve only the most strategic clients.

- Take on only the most complex matters.

- In only strategic jurisdictions.

Was this focus, which seemed to have a significant effect on the RPL measure, a critical part of your strategy?

Brad Karp: Absolutely. We believed that selecting and prudently investing in the right practice areas were the foundation of our strategy. Of course we needed to ensure that we had the right talent and the right clients and operated in the right jurisdictions for the strategy to work. At the end of the day, if I were to boil down the essence of our core strategy as it has evolved over the past 15 years, it is to represent the most important companies in the world on their most consequential matters and to become a ‘safe choice’ for CEOs, GCs and board chairs in each of our five key practice areas. Subsidiary to that goal is the objective of taking on only strategic clients and strategic matters that are price-inelastic and avoid the increasing commoditization of legal work.

Couture: Was there a challenge in getting agreement among the leadership team and partners?

Karp: No. I’ve been the chair of Paul, Weiss since 2008 and, looking back, the strategic themes I set forth in my first firm-wide address to my partners in May 2008 are not fundamentally different from the themes I articulated in May 2023. We are just at a more mature level of our strategy. There were a few partners early on who needed to be brought along, but there was broad consensus in support of the strategy and our partners wanted to be led in the right direction. I found the key was to articulate the bases for the strategy and to persuade my partners to strip away any sense of individual self-interest and focus at all times on the best interests of the firm. There were occasional challenges, including persuading the partnership to buy into the institutionalization of key client relationships, an issue that has become even more important in today’s uber-competitive world, with fraying partner and client loyalty at many elite law firms.

Couture: How did you communicate these objectives to the firm?

Karp: Twice a year I deliver a lengthy “state of the firm” address, which runs about an hour. I believe the only way you can effectively execute and implement strategy is if you communicate it continually, consistently and clearly—and hold individuals accountable. We also have a full partnership lunch every Thursday, which is very well attended, where I reinforce our strategic goals and we talk about culture, strategy and performance. Constant transparency is critical and it’s fairly easy to execute because most of our partners are in New York and zoom has overcome previous geographic hurdles.

Couture: How do you construct the elements of your message?

Karp: The strategic logic in our ongoing communication is consistent:

- This is what our firm looks like today.

- This is what the competitive landscape looks like.

- To be one of the two or three most commercially successful law firms in the world and to be true to our culture and our traditional, professional values. These are the key strategic objectives we need to focus on and these are the ways in which we need to implement our strategy.

Today, I believe we have the right practice areas, the right talent, the right demographics, the right diversity, and the right clients, but we cannot become complacent and we must continue to continually invest in and dynamically evaluate each of these areas. We remain on the lookout for transcendent talent and we constantly evaluate new strategic practice areas. We are not rigid or doctrinaire. We are not allergic to change. A recent example of our willingness to invest in new practice areas is ESG. We concluded early on that ESG issues are (and would continue to be) ubiquitous across the business landscape, implicating each of our core practice areas, and we were one of the nation’s first law firms to create a standalone ESG practice group, back in early 2020.

Couture: Do you have measurements to determine your progress?

Karp: Yes, we continually review our clients and matters to ensure that we are in fact delivering on our core objective of representing the world’s most important companies on their most consequential matters. We track cross-selling across the partnership. We continually check in with our clients to make sure that we are delivering on our commitment to provide world-class service and to add value in each representation. We closely track our profitability levels, our diversity metrics, our lawyer retention rates, our pro bono commitments. It’s critical for us to maintain our position as one of the world’s most profitable law firms, while maintaining our traditional values and our commitment to the most vulnerable members of our community.

Couture: Final thoughts?

Karp: Managing a law firm has never been more challenging. The legal world has never been more competitive. Formulating the right strategy is critically important. But continually communicating that strategy across the partnership and holding partners accountable for its implementation are equally important.

Couture: Neil, over the past six years, Davis Polk has modified the mix in the type of work you are doing for clients and increased your revenue per lawyer by 56 percent, more than 2.5 times the median for the Am Law 100 firms. You outlined your key strategic areas in the American Lawyer in May 2022. What additional elements of your strategy led to that performance?

Neil Barr: We think of our strategy in three parts. First, as you mentioned, the type of law that we practice. We have defined six major areas of focus and work hard to stay within—and be a preeminent firm in—those focus areas.

Second, the geography in which we practice. We are a firm that is materially more U.S.-centric than non-U.S., but we also want to have a strategic presence in key business centers around the globe.

Third is scale. We are not scale agnostic; we don’t want to be the biggest firm, but we do need to be large enough to provide competitive client coverage and manage down our cost base to increase efficiencies. Scale also provides increased operating flexibility to take risks and invest in strategic opportunities. And we want to do this in a way that preserves our value to clients and maintains our brand integrity.

We went through an evolution over the last decade to operate much more like a business. During that time we involved our partnership in the economics of the business, making sure performance was where we wanted it to be, and we did a bit of portfolio shaping. We had to rotate out of some businesses and into others to fit our strategic areas. It was also very important to ensure that our allocation of firm capital was aligned with our areas of strategic focus.

Couture: Were there any specific actions you took to get this alignment?

Barr: Probably the hardest thing we have done was adjusting our compensation structure away from one that is entirely and only lockstep. Our approach with our partners was highly consultative, which was critical in making the transition successful. We felt this added flexibility was crucial to grow and execute on our strategic objectives.

Couture: How do you communicate these critical efforts to the partners to make sure they understand that the things they do every day are critically important to getting the firm where you want it to be?

Barr: I think that’s a great question. At least once a year I give a strategy presentation that describes where we are, what we’re seeing in the marketplace, and how we are performing against our objectives. I also give an annual “state of the firm” update at our annual partner meeting, and every Thursday we have an informal meeting with the entire partnership where we get into microlevel topics. In that weekly meeting we discuss current transactions and cases and how they fit into the firm strategy. And we reinforce behavioral things like pricing optimization, cross-selling, CRM tools, etc. I view this as operational strategy as opposed to top-line strategic. And of course we keep informal lines of communication open, and a lot of important conversations happen just by walking the halls.

Couture: Do you have to decline work for pricing reasons?

Barr: Yes, we do. Sometimes we simply conclude that the opportunity cost for a particular mandate is too high relative to the financial return to the firm of that mandate. When we make that decision, it’s important to communicate to relevant partners the rationale for the decision so that everyone is aligned.

Couture: When communicating, there is a difference between “telling” partners what and why and actually getting them to internalize the logic of the reasons for change that leads to their agreement on the plans. How did you accomplish this?

Barr: With the big decisions we make, I try to start by framing our value system, what we believe in, and our culture, because that’s the architecture on which we are building our business. Then I link the operational decision to the architecture so it is anchored to the value system. This makes decisions less sterile and more a part of who we are as a business.

Couture: Final thoughts?

Barr: I think this industry is really changing. I think the law firms that overperform going forward will do so on the basis of characteristics that are different from those of the last 15 years or so—meaning that brand and prestige will be a part of the story, but strategy, operational efficiency, and other such issues will increasingly play a role in firms’ financial performance.

Couture: Jon, over the past six years you have grown the number of lawyers at Kirkland by 87 percent, five times the average of the Am Law 100 firms as a group. At the same time, the RPL of Kirkland has grown 40 percent, nearly twice as fast as the peer group. Was this growth in the number of lawyers a primary element of your strategy?

Jon Ballis: There was never a strategy that bigger is better. It was always about quality, staying focused on the complex, differentiated work and most important, anticipating where our clients were headed so we could meet them there with the corresponding talent and resources. That required investing in talent and thus growing almost organically based on client demand. For example, because our firm has a large volume of private equity [PE] clients, and we’ve seen an increase in the variety and complexity of funds our PE clients were raising over the past five plus years, we’ve also expanded our talent in those key areas—for example, secondaries, credit, and GP stakes. And this same strategy applies to multiple aspects of our business.

Couture: You differentiate between “bigger is better” and scale. Can you expand on that?

Ballis: We’ve seen really nice growth across all of our practices, but the biggest growth (scale) has been in the transactional area and primarily in private equity. Our clients were growing quickly—increasing exponentially in assets under management—and we knew we had to grow with them or we would lose market share. We saw the opportunity to capture more and more of that pie by looking around corners, finding our areas of competitive advantage, and investing in them. I often tell our partners that the speedboat that we were skiing behind was getting faster and bigger every day, and if we didn’t build some bigger skis, we were going to fall down.

Couture: In terms of communicating this opportunistic strategy, how did you get all of your partners to fully understand and embrace this vision?

Ballis: We’ve always been a really entrepreneurial firm, but I think the past 10 years—and the last five, in particular—have been transformational for us in how collaborative and team oriented our culture has become. Our partners see how it benefits all of us now. I don’t think they always did, and that’s why I continue to hammer home that message every chance I get—at our partner meetings, breakfasts, lunches, dinners, you name it. It is a practice of constantly reinforcing the message, and it’s critical to explain the strategy because the hard part—the execution—relies on everyone rowing in the same direction. I cannot overstate the importance of collaboration in our success. When I do that, they tell others and it cascades throughout the firm.

Couture: Can you expand on your view of the value of “scale”?

Ballis: While being bigger was not the objective, the reality is that scale is not unimportant and can be a very powerful tool for our business. It allows us to do things that other firms just find too expensive. We spend about 1 percent of our revenues in new initiatives.

Couture: Such as…?

Ballis: Investing in talent, both lateral hiring and developing industry-leading training programs; leveraging our scale and data with dedicated knowledge managers and data scientists; or launching new practice areas.

Couture: Is this analogous to a corporation’s R&D budget?

Ballis: Exactly. Some of it is capital expenditures; some of it is skunk works. For us to spend this much with annual revenues over $6 billion, we can do some very meaningful things that enhance our ability to work with clients and win new business.

Couture: Since you are not a corporation with retained earnings and this investment is directly affecting total partner comp distributed every year, how did you communicate the value of this “R&D budget”?

Ballis: I can have the greatest explanation and the most beautiful PowerPoint slides, but improved results are by far the most convincing. One last point on scale: if done properly and focused on practices where your brand is elite, it can help drive profitability, which in turn helps us to continue to recruit differentiated talent aggressively.

Couture: The type of work you do is highly sophisticated and complex. How do you maintain that level of expertise across the firm?

Ballis: The thing that keeps me up at night is how we continue to grow and keep up with our clients. In the PE arena, they splinter off and multiply, and our challenge is to follow and stay ahead of their needs. Quality cannot be compromised. We have to maintain our elite brand while growing. It’s a delicate balance between scale and brand preservation. And that’s part of the reason we focus so heavily on training and knowledge management and dissemination. We want it to be as easy as possible for our attorneys to function at their brightest and best.

Couture: Have you lost partners that have not been able to align with this strategy?

Ballis: Sure. We have grown our business by making each client a “firm” client with multiple Kirkland lawyers involved. I don’t think we’re unique in this approach, but not all partners are comfortable with that, so we part ways if we aren’t aligned. We reward people who act in the best interest of the institution. We attract a very motivated and entrepreneurial group of people, and scale helps us do that. I keep coming back to scale because it allows us to take more chances than most firms, but as a result we also have more misses than most.

Couture: What types of chances and risks are typical?

Ballis: Investing heavily in new industry capabilities, such as energy. This one worked out well, and we have substantial capabilities in Texas as a result. Another example is opening an office based on the availability of high-quality talent within a specific geography. Our Salt Lake City office is a great example of that.

Couture: Is there anything you would like to add that would help illuminate the reasons for your ongoing success?

Ballis: We have an entrepreneurial culture that allows people to swing for the fences. But we are intentional about the swings we take. We often win, sometimes we lose, but we have a growth mentality and every little win adds up. Lawyers are traditionally risk averse by profession, but Kirkland has a different vibe to it, and our people self-select to be part of this culture. Collaboration is also a huge piece of this. We have to consciously work together to drive our firm forward, and that’s something we incentivize our people to do. With respect to our private equity business, I like to say that we were lucky enough to fall into it in the first place, but then smart enough and bold enough to invest in it aggressively. That’s the punch line.

Reflections

Each individual reader can find different learnings from these interviews. Some may identify certain strategic business areas that are attractive. Others may see an opportunity in institutionalization, scale, or perhaps the rigors of identifying key initiatives and maintaining them over a long period of time. Maybe it’s the flexibility of an opportunistic approach that is a key to success. There are many books and missives written about legal strategy and execution, which can be an excellent menu of best practices and things to avoid. You can learn how to identify your firm’s competitive advantage, analyze competitors, develop proprietary offerings, improve internal efficiencies through case methodologies, expand your profile through marketing and PR campaigns, develop rigorous internal communication protocols, develop an intake system that keeps the firm on the defined strategic path … the list goes on and on. These can all be useful elements of a successful strategic approach for your business.

From these interviews I identify a rather simple commonality that, in my view, surpasses all the other elements of success: ownership and passion.

Using the analytic model discussed here can also lead to some difficult choices, since operating in every quadrant has advantages and challenges. For example, firms in the Northwest quadrant must consider the limitation of the total marketplace opportunity for the type of work they are doing. Growth in geography or scale may not be desirable because it is extremely difficult to increase market share due to the limited amount of high-value work and entrenched competition. Attempting to do so may risk damage to their brand. Firms in the Southwest quadrant typically have great regional client relationships and provide the bulk of legal services these clients need, yet they are always subject to new competitors who provide a more compelling value proposition. This can come from existing law firms (the Southeast quadrant) or new entrants commonly called alternative legal service providers (ALSPs). Outside of the U.S., these have included the Big Four accounting networks, and their threat within the U.S. market has been omnipresent for the past two decades. It also wouldn’t be surprising to see technology-enabled ALSPs make greater strides in capturing this type of legal work in the coming years using tools including the latest artificial intelligence systems. Firms operating in the Southeast and Northeast quadrants both have to deal with the management challenges of scale. Law firms do not typically have well-developed management organization and discipline that will be necessary to operate at greatly increased size. These certainly can be developed but will require cultural adjustments to the “partnership” model of organization that law firms have grown comfortable with during the past 40 years. There is also the difficult issue of legal conflicts that must be successfully managed and negotiated to support a very large organization. The norms and rules for these are just being adjudicated and developed. In addition, firms operating in the Northeast quadrant have developed partnering arrangements with some of the Big Four accounting firms to provide services they chose not to do themselves, which introduces a risk element of client relationship and overall leadership (whose client is it?). These are just a few of the issues that will be resolved as the legal industry consolidates and matures.

Related content

Related content

Preparing to Steer the Ship

Returning to the matrix analytic and the movement of firms in the Am Law 100 during the past six years, why did some far outpace the pack? What differences were present that allowed them to improve their strategic positioning vis-à-vis their competitors? From these interviews I identify a rather simple commonality that, in my view, surpasses all the other elements of success: ownership and passion. All three chairs have demonstrated a thorough understanding and belief in the approach they take and the logical reasons for selecting the strategy they pursue. The ownership and primary communication of their strategies have not been delegated to anyone, and the passion that goes along with all the communicating and preaching they do is constant and unrelenting. They go further than just communicating and ensure that the understanding and belief in their strategy is embraced by all of the partners. If there are any doubters, they continue to explain, cajole, and preach until converted. Yes, it feels a bit like strategic religion. Once this level of understanding and agreement gets to a critical level, the pace is much easier to maintain. But yet they don’t let up. All good leaders employ their management teams to help with execution, but to be really successful, the top executive has to delegate without abdication. And then own it. This is perhaps the most critical element of strategic execution, even more important than the strategy itself. Every strategy can be viewed as a road to somewhere, and there is more than one road to take, but the best leaders make the destination clear and compelling.

Robert Couture is a senior research fellow at the Harvard Law School Center on the Legal Profession. He was previously chief operating officer at McGuireWoods.