The student debt crisis disproportionately impacts Black Americans, reflecting and perpetuating the Black-White wealth gap and reverberating over generations and the life course. Among law student populations, this disparity has spillover effects onto democratic processes and access to legal services, further creating and compounding inequality in the United States.

The cost of postsecondary education in the United States has skyrocketed over the past several decades, with the national student debt surpassing credit card debt to reach an unprecedented $1.75 trillion, or about 7.5 percent of the national GDP. Federal loans account for 92.6 percent of total student loan debt, with 44 million borrowers holding an average of $37,338 in federal student loan debt. The average student debt for private loan borrowers is even higher: $54,591. But there are large disparities in how this student debt crisis is distributed and felt, with an uneven impact across racial/ethnic groups. While White borrowers graduate with an average undergraduate student debt of about $30,000, Black men graduate with $35,665 and Black women with $37,558.

Scholarly research and public discourse surrounding student debt tend to focus on undergraduate education, yet recent studies have identified an increasing proportion of student loan debt accrued at the graduate and professional degree level.1 On average, Black students borrow more than White students for graduate and professional education, with the highest debt accrued by Black students in private institutions.2 These findings suggest the dramatic rise in student debt associated with advanced-degree programs plays a key role in reproducing social stratification by raising the cost of graduate and professional credentials and by deterring undergraduates from disadvantaged and underrepresented racial backgrounds from pursuing these programs in the first place.3 These barriers to higher education have important implications for racial equity and civil rights as they systematically disadvantage and limit access to education for students from historically subordinated racial groups.4

Why this matters for the legal profession

Racial disparities in student loan borrowing among graduate and professional students in general are reflected in patterns of borrowing among law students, with Black law students being more likely to rely on loans than White students5 and Black women disproportionately graduating with high levels of student debt.6 Unequal access to legal education in particular has important implications for democracy as lawyers play a central role in mediating the relationship between the state and its citizens.7 Barriers to legal education and the legal profession also have serious implications for racial equality and social justice. Many lawyers in the United States take on prominent roles in the economic and political spheres, and student debt limits opportunities for Black individuals to participate in positions of power and privilege in American society. Moreover, lawyers are an integral part of the administration of justice and ultimately regulate the cost and accessibility of their services, with the accessibility of legal services directly influencing the degree to which the goal of equality before the law can be accomplished. Although it is difficult to estimate the impact of student debt in deterring individuals with bachelor’s degrees from pursuing legal education, I find a striking student debt gap among Black and White law school graduates.

After the JD Data

My research draws on a rich and novel data set on law school graduates from the first ever national study of lawyers’ careers. After the JD (AJD) employs a rigorous and sophisticated multimethod research design to track the first 20 years of lawyers’ careers, collecting data on a broad array of topics including social and educational background; legal education financing; earnings and hours worked; job mobility; fields of practice and legal specialties; career and job satisfaction; family formation; mentorship and professional networks; gender-, race-, and class-based inequality; and experiences of workplace discrimination.

The concept for the project was first pitched by members of the National Association for Law Placement (NALP) over 40 years ago and was moved in 1996 to the American Bar Foundation (ABF), which has long been recognized as the principal source of empirical research on legal education and the legal profession. The capstone book on the findings from AJD will be published in October 2023 by the University of Chicago Press.

AJD follows a cohort of individuals who graduated from law school between 1998 and 2000 and joined their first state bar in 2000. Respondents were surveyed at three points in time: wave 1 data was collected in 2002–03, when respondents were launching their careers; wave 2 data was fielded in 2007; and wave 3 data was collected in 2012–13, when respondents were entering their midcareers. Survey respondents were drawn from 18 primary sampling units that, when combined, represent the national market for new lawyers, including all four “major” markets (New York City, Chicago, Los Angeles, and Washington, DC), five of the nine “large” markets (those with 750 to 2,000 new lawyers), and nine smaller markets (those with fewer than 750 new lawyers). The final sample included 8,225 eligible individuals, including an oversample of 1,456 new lawyers from racial/ethnic minority groups.

In total, 5,399 unique respondents participated in the AJD study. Wave 1 yielded 4,538 eligible responses, for a response rate of 56 percent. Wave 2 was sent to wave 1 respondents and nonrespondents, yielding 3,705 eligible responses, for a response rate of 50.6 percent. All respondents who participated in at least one of the first two waves of the study were invited to participate in wave 3, yielding 2,984 eligible responses, for a response rate of 53 percent. The study also includes more than 200 in-depth interviews with respondents and web-based employment data for respondents through 2019.

Debt repayment and the Black-White wealth gap

While research on student debt often relies on snapshots of a cohort’s projected or actual student debt upon graduation or on aggregate statistics at a single point in time, longitudinal data on student loan repayment indicates the Black-White student debt gap increases substantially in the first few years after earning a bachelor’s degree and is thus far wider than suggested by studies of racial gaps in borrowing.8 Studies of group differences in student debt—including my own—suggest Black men encounter the greatest difficulty in repaying their loans,9 while research on individual student loan trajectories indicates that Black women pay off their student debt more slowly than both White women and Black men.10 Taken together, these findings illustrate the disproportionate burden of student debt borne by Black borrowers and how the racial gap in student debt widens over the early-adult life course, a pattern that is attributable to “hardship and discrimination experienced at different stages of the life course: family resources when young, postsecondary experiences and credit market access as students, and social and financial success as young adults.”11

The current regime for financing higher education is both cementing and polarizing racial inequality and the Black-White wealth gap.

According to a 2019 report by the Legal Defense Fund’s Thurgood Marshall Institute, Black households in the United States hold about seven percent of the wealth of White households, which is a consequence of centuries of entrenched, structural racism, and racialized and exploitative social and legal policies and structures. The disproportionate impact of the student debt crisis on Black Americans both reflects and reinforces the Black-White wealth gap,12 which has been perpetuated through processes of intergenerational wealth transmission; racist housing, credit, and welfare policies; and Black Americans’ historical and ongoing exclusion from and discrimination within education and labor markets.13 Research on the National Longitudinal Survey of Youth 1979 indicates that the Black-White wealth gap increases with age, accumulating over the course of individuals’ lives, particularly in early and middle adulthood, highlighting the ways in which racial wealth gaps are shaped by intergenerational legacies of disadvantage and reproduced in subsequent generations through disparities in wealth-enhancing traits.14

In addition to—and underlying—durable quantitative differences in the wealth of Black and White families are important qualitative differences, with White families enjoying intergenerational inheritances that fund education and home ownership and provide advantages and economic security that accumulate over the life course and in subsequent generations.15 Research indicates that the racial wealth gap tripled among college-educated families between 1989 and 2013, and that student debt is an important and emergent mechanism undergirding the Black-White wealth gap today.16

The current regime for financing higher education is both cementing and polarizing racial inequality and the Black-White wealth gap.17 Coming from lower-wealth families on average, Black students must borrow more to finance their education than White students and are more likely to default on these loans.18 Black students and students of private postsecondary institutions—in which Black students are overrepresented—take on more and larger loans and encounter greater difficulty in repaying their debt, which further impedes wealth accumulation19 and contributes to Black-White disparities in education, earnings, health, and other outcomes.17 Thus, the crushing weight of student debt impacts long-term disparities that widen the Black-White wealth gap and constrain educational and socioeconomic inequities for students both over the life course and for generations to come.20

Rising law school costs and the AJD cohort

In the 20 years before AJD respondents graduated from law school, the cost of attending American law schools increased more than sevenfold. The average tuition for private law schools had soared to $19,000 by 1997, while out-of-state public law schools cost $12,500 and tuition for in-state public law schools rose to $6,000.21 Law school debt and the proportion of legal education costs covered by loans grew in tandem with the sharp increase in law school tuition.22 In the 1996–97 academic year, family and personal resources financed 31 percent of the cost of legal education. This share grew over time as students repaid government loans, making personal finance the principal underwriter of the cost of legal education.23

Diving into the AJD data

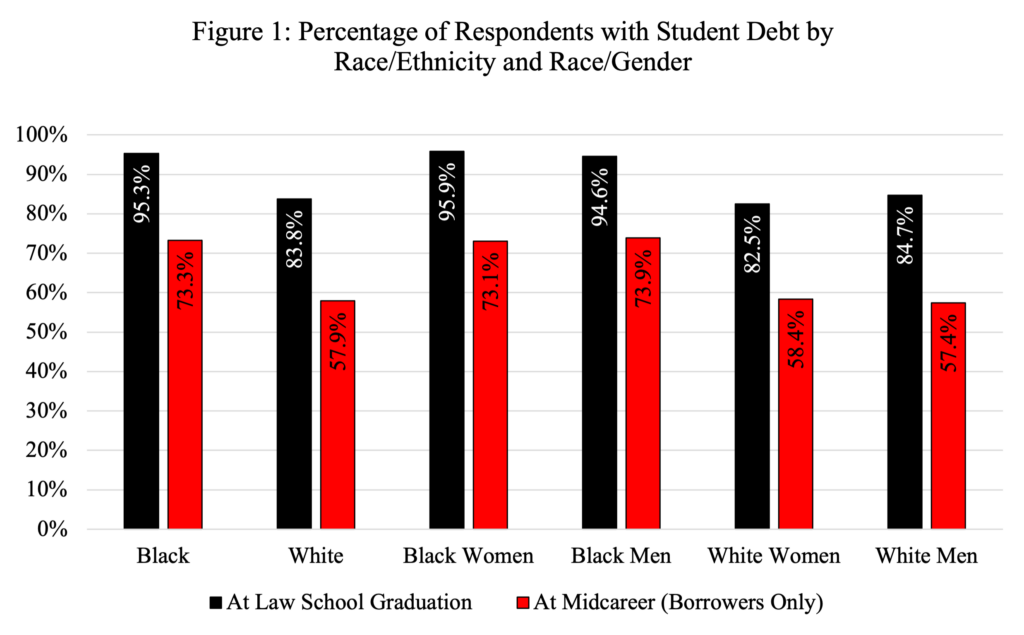

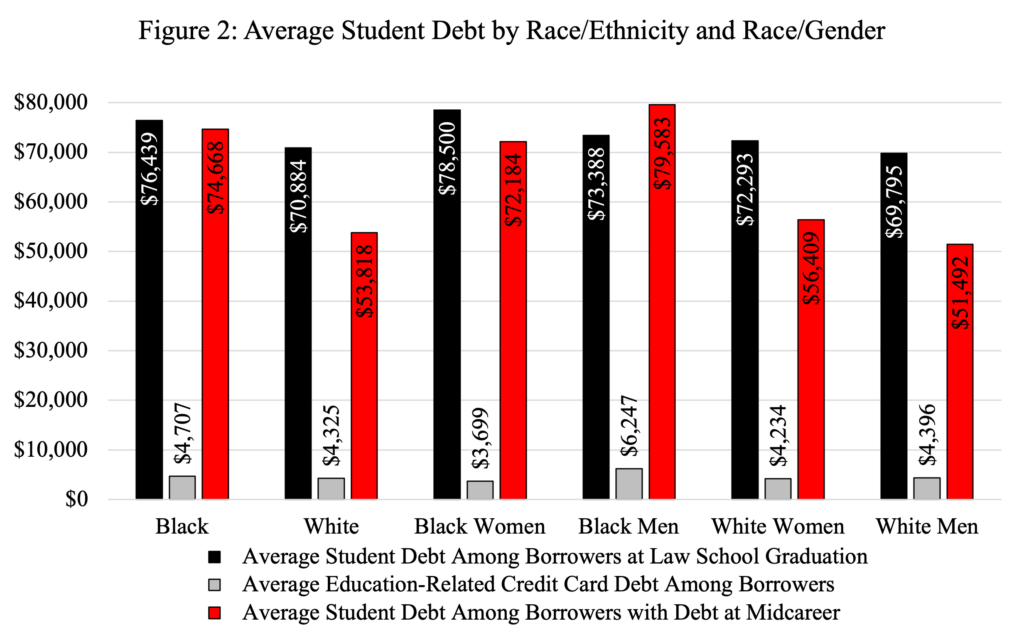

Among law school graduates who participated in the AJD study, Black respondents are 13.7 percent more likely than White students to graduate from law school with student debt (see Figure 1), and Black borrowers graduate from law school with 7.8 percent more student debt than White borrowers (see Figure 2). By midcareer, these differences are even starker: Black borrowers are 26.6 percent more likely than White borrowers to have student debt remaining, and, among midcareer debtors, Black borrowers owe 38.7 percent more than their White counterparts. Black women are the most likely to graduate with student debt (95.9 percent), followed closely by Black men (94.6 percent), and Black women graduate with the highest average debt among student loan borrowers ($78,500). By midcareer, Black women and men who graduated with student debt are about equally likely to remain indebted (73.1 percent vs. 73.9 percent), and indebted Black men owe the most ($79,583), suggesting they encounter greater difficulty than Black women in repaying their loans.

Rigorous and systematic demographic and sociological research has demonstrated the racialized and gendered nature of student debt, and the unique impact of student debt on Black women. Existing at the intersection of two marginalized identities, Black women experience both sexism and racism. Intersectionality refers to the interlocking systems of oppression related to race/ethnicity, gender, socioeconomic position, and sexuality that simultaneously shape individuals’ lived experience.24 Both women and Black individuals were historically defined by law as inferior to men and White Americans and were excluded from higher education and paid employment. Despite legal and structural changes in the status and inclusion of women and Black Americans, this historical culture of exclusion endures, manifesting in institutional and individual biases that operate to sustain workplace inequities.25 AJD research also indicates that Black women are more likely to experience workplace discrimination than any other group in the legal profession.26

Although women have made remarkable inroads into education and the labor market, the gender wage gap persists, with women earning less than men due to gender segregation in the labor force, discrimination, and household/family inequality, including work interruptions and economic and opportunity costs related to childbirth and childcare, and with Black women earning less than both White workers and Black men. Consequently, Black women have reduced access to financial resources, must borrow more money to cover their education, and encounter significant barriers in repaying their loans.27

Despite legal and structural changes in the status and inclusion of women and Black Americans, [a] historical culture of exclusion endures, manifesting in institutional and individual biases that operate to sustain workplace inequities.

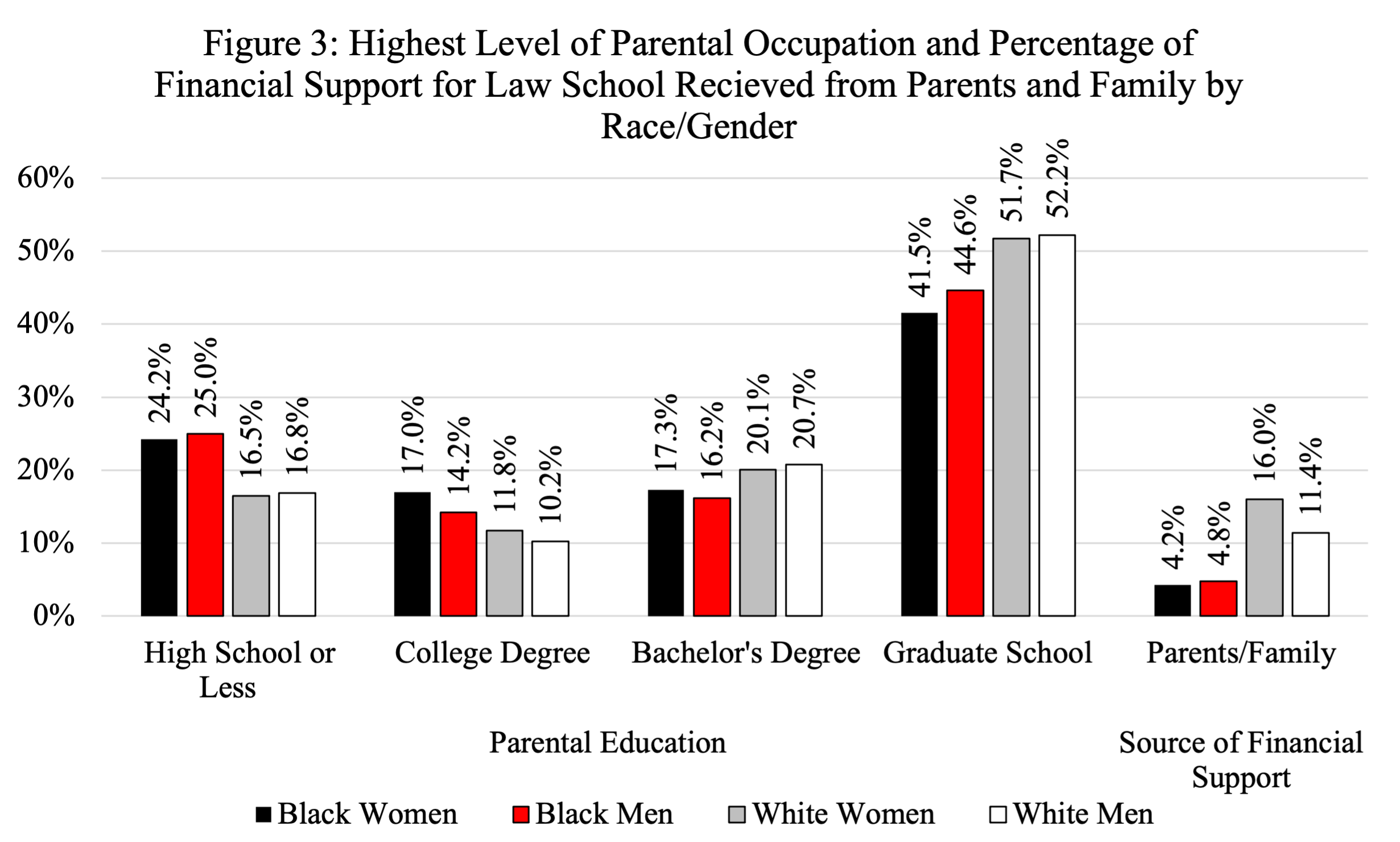

AJD data indicates similar borrowing patterns among law school graduates, with Black women being the most likely to borrow money to finance their education and borrowing more money than other groups. Financial contributions from parents and other family members are an important source of support for paying for law school, yet the availability of this form of financial contribution is tied to relatives’ means, which are unevenly distributed.28 The proportion of law school financing that respondents received from their parents and other relatives is highly correlated with social background, with respondents whose most highly educated parent had a high school degree or less receiving 5.2 percent of their legal education funds from family members, those whose parent(s) graduated from college receiving 7.2 percent, those whose parent(s) had a bachelor’s degree receiving 10.9 percent, and respondents whose parents attended graduate or professional school receiving 18.5 percent of their law school funding from parents and relatives. As indicated in Figure 3, Black respondents’ parents are less highly educated than White respondents’ parents, on average, and Black respondents received a far smaller proportion of the funds they used to finance their legal education from parents and other relatives.

Multivariate models indicate that a substantial portion of Black women’s higher student debt borrowing compared with white men’s is related to their higher likelihood of graduating from top 20 law schools, particularly those ranked in the top 10 (18 percent vs. 10.6 percent), as average student debt is higher among graduates of higher-ranked law schools. Black women’s higher student debt at graduation is also attributable to the significantly lower share of financial support for law school that they receive from parents and other family members, net of parental education.29

Intergenerational wealth transmission and financing legal education

Although AJD did not collect data on familial wealth, racial differences in the role of intergenerational wealth transmission in funding respondents’ legal education, illustrated in the following quotes featured in the forthcoming capstone book on AJD, are suggestive:

“[Katrina’s White] parents were middle-class and well educated, and, with her grandfather’s support, she was able to earn her undergraduate degree and JD without any debt.”

“Stewart, an African American man . . . attended a historically black undergraduate institution and a top 20 law school. He did not receive financial support from his parents and graduated with $60,000 in student debt.”

“The son of a mathematics professor from New York City, [Bryce, a White man,] attended a prestigious liberal arts college and one of the city’s top law schools . . . He graduated without debt, thanks to an inheritance from an aunt.”

“Isabel attended a historically Black university as an undergraduate and was encouraged by a professor to apply to law school . . . She left law school with $150,000 in debt.”

Importantly, Black women remain the most indebted race/gender group upon graduation from law school irrespective of undergraduate rank and performance, law school characteristics, and financial support from scholarships and family, reflecting the disproportionate burden of student debt borne by Black women in American society more broadly. This portion of the gap that remains unexplained is likely attributable to variables beyond the scope of the AJD data, including the reduced access to wealth and greater hardship and discrimination that Black women encounter over the early life course compared with white men.

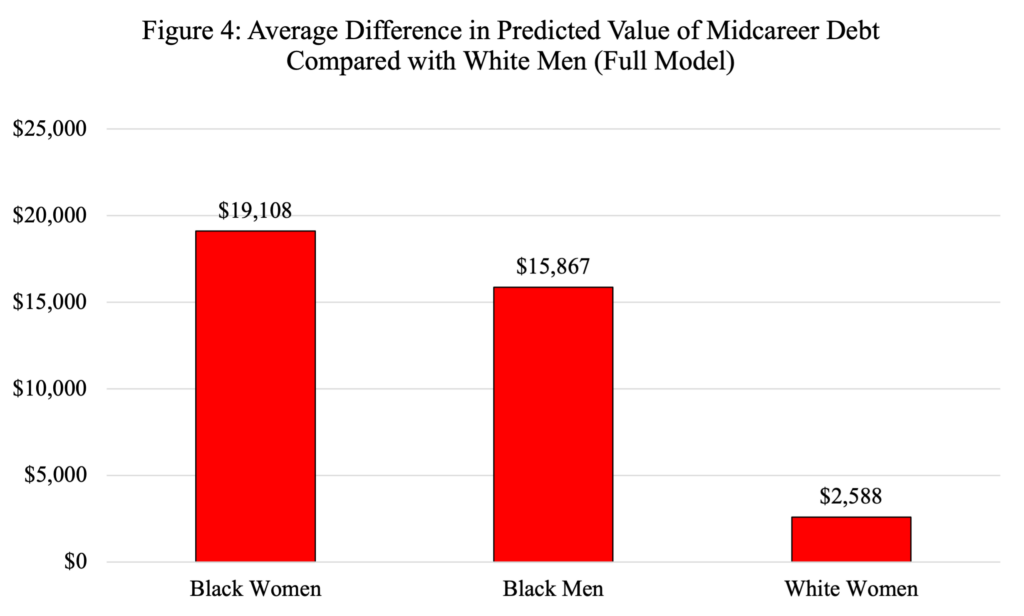

Although Black women are slightly more likely than Black men to repay their debt in full by midcareer (26.9 percent vs. 26.2 percent), indebted Black men carry substantially higher student debt at midcareer than Black women on average. However, multivariate models indicate that the higher debt burden of indebted Black men at midcareer compared with Black women’s is attributable to the higher amount of credit card debt they accrue as law students (Figure 2). In baseline models, predicting midcareer student debt, Black men are both more likely than Black women to have debt remaining and, if indebted, to have more debt. However, when controlling for amount of credit card debt at graduation, Black women emerge as the most likely to be indebted and as holding the greatest debt among debtors, and this pattern remains in models controlling for differences in educational background and earnings at midcareer (Figure 4).

Investigating student debt longitudinally highlights the ways in which Black Americans are uniquely burdened by student debt, and the manner in which gender intersects with race in shaping experiences of student debt over the life course.

These findings indicate that Black men encounter greater difficulty in repaying their debt, but that if it were not for their greater initial sums of high-interest credit card debt, Black women would be worse off. It is also notable that the relationship between debt and law school rank inverts between graduation and midcareer, with average debt levels decreasing among graduates of higher-ranked law schools. Thus Black women are more indebted than white men despite their overrepresentation among top-tier law school graduates. Taken together, the results underscore the salience of the Black-White student debt gap among law school graduates and its persistence over the course of lawyers’ early careers, shedding light on the mechanisms that differentially impact Black men and Black women in sustaining this racial gap.

Recent developments

In 2021 the Biden administration announced its intention to narrow the Black-White wealth gap, an important driver of which is student debt. In 2022 the Administration announced that it would pursue a substantial and semitargeted loan forgiveness plan that would reduce the loans of 43 million Americans and eliminate the loans of another 20 million. The proposed program had three parts: (1) It would forgive up to $10,000 in federal loans for single borrowers with incomes less than $125,000 and married borrowers with household incomes less than $250,000, and forgive up to $20,000 for Pell Grant recipients. (2) It would modify income-driven repayment plans by lowering repayment caps from 10 percent to 5 percent of discretionary income and by lowering the total discretionary income that would be calculated toward that cap. And (3) it would extend the COVID-19 moratorium on student loan payments and interest.

In May 2022 Republican senators introduced a bill to stop Biden’s student loan cancellation plan, claiming it would increase inflation, encourage universities and colleges to raise their tuition, increase the national debt, and amplify inequality by disproportionately benefiting wealthy individuals, characterizing loan forgiveness as both expensive and regressive. The Biden administration’s plan was halted in November 2022 by lawsuits brought by conservative opponents, prompting President Biden’s attempt to salvage loan forgiveness by using emergency “waiver” powers activated by the COVID-19 pandemic. The case was directed to the Supreme Court of the United States, and on July 6, 2023, the conservative-majority SCOTUS struck down the Biden administration’s student loan forgiveness plan, ruling that the president lacked the legal authority to cancel student debt and effectively killing the proposal.

While the Biden administration framed the student debt crisis as a public issue in which the government should intervene, the Right criticized loan forgiveness as regressive. Conservative politicians, scholars, and think tanks often argue that canceling student debt would be regressive because it would benefit privileged Americans by forgiving the loans of highly educated (and thus, higher-earning) individuals at the expense of lower-educated and lower-paid taxpayers. However, this argument is misguided for many reasons. For example, having student debt neither guarantees that one graduated from or even attended college as many people assume student debt in the form of parent PLUS loans to support the education of their children and grandchildren, and having student loans has become a marker of relative disadvantage as it is an indicator that borrowers’ families did not (or could not) contribute to their educational expenses. Conservative critics of student debt cancellation programs also argue that these proposals are regressive because they would cancel only debt for which the federal government is the lender. Borrowers with strong credit can refinance their debt with private lenders who offer more favorable repayment terms, and thus only a subset of the lowest-earning student loan borrowers would have their debt forgiven. However, the debt-income ratio for student loans is highest among lower-income earners, and canceling student debt would help equalize the wealth distribution. Thus, student debt cancellation programs are in fact progressive, not regressive.30

What AJD teaches us

While AJD data cannot directly speak to policy solutions, the findings reinforce broad evidence of racial inequality in student debt borrowing and repayment patterns. Policy and discourse surrounding student debt often rely on student loan borrowing and point-in-time estimates, yet research suggests it is crucial to understand how debt unfolds over the life course. While the Black-White gap in student loan borrowing is well-documented in research on student debt, racial differences in student loan repayment are less understood. Investigating student debt longitudinally highlights the ways in which Black Americans are uniquely burdened by student debt, and the manner in which gender intersects with race in shaping experiences of student debt over the life course.

Statistical models based on administrative data drawn from credit reports predict American student loan debt will never be repaid. Given the durable and pervasive Black-White gaps in both wealth and student debt, plans aimed at student debt cancellation ought to be evidence-based and center their potential impact on racial equity. For example, Charron-Chénier and colleagues modeled the effects of universal loan forgiveness designs and targeted designs incorporating income thresholds using data from the 2019 Survey of Consumer Finances, and found that forgiving between $50,000 and $75,000 of debt for borrowers in households with an income of $100,000 to $150,000 would reach a majority of borrowers and eliminate about half of student debt without substantially increasing the racial wealth gap and still generating wealth gains, especially among Black households.31 However, social science research suggests that using income as an indicator of ability to repay student debt can obscure the role of historical discrimination and its impact on the intergenerational accumulation of wealth, which undergirds and perpetuates the Black-White wealth gap and impedes the ability of Black student loan borrowers to repay their student debt.30 Indeed, AJD data demonstrates that Black women and men have significantly more debt than their White counterparts at midcareer irrespective of their earnings. These findings support the argument that income-driven repayment is an insufficient solution to the student debt crisis.

Progressive politicians, scholars, and analysts such as senators Elizabeth Warren and Bernie Sanders and law professors Dalié Jiménez and Jonathan Glater advocate for bolder interventions, including near-total and even complete student loan forgiveness and free tuition at public higher education institutions through increased federal funding and taxes imposed on the wealthiest Americans and financial transactions.32 (For more on Elizabeth Warren’s thoughts on student debt, see “What We Owe Our Students.”) Representing a mere 5.3 percent of America’s national debt of $32.8 trillion,33 the cost associated with forgiving student loan in full would be a drop in the proverbial bucket. The federal government spent approximately $1.35 trillion (inflation adjusted) bailing out banks in the wake of the savings and loans crisis of the 1980s and the 2008 financial crisis alone.34 Rather than rewarding corporations and financial elites, canceling student debt outright would improve the life chances of 44 million individual Americans and their families and would help close the racial wealth gap—a relatively small price to pay for civil rights, racial equity, and social justice.

The magnitude of the student debt crisis and the racial wealth gap have made this a pivotal moment for our generation.

Although forgiving student loan debt would help undo past injustices associated with the student debt crisis, preventing a recurrence in the future would require lowering the cost of higher education through regulation and increased government spending. Although these measures would certainly cost taxpayers money, producing university and college graduates free of debt would benefit the economy by enabling higher income tax contributions and support for employment, commerce, and the production of goods and services through increased consumption,35 and would constitute an important and substantial investment in promoting the ideals of democracy and equality that the nation so fiercely espouses.

The present scale of student debt in the United States is alarming and has limited the financial options of millions of borrowers. The Black-White student debt gap—particularly that among law school graduates—has important implications for democratic participation, racial equity, and civil rights, and both reflects and reinforces the Black-White wealth gap. The magnitude of the student debt crisis and the racial wealth gap have made this a pivotal moment for our generation. Intersectionality theory is important for improving research design and policy outcomes, yet its application in social science research should go beyond measuring the impact and experience of overlapping identities to unpacking the ways in which processes like gendering and racialization intersect to create hierarchical systems of oppression.36 With its rich longitudinal data on education, work histories, family formation, and other aspects of lawyers’ lives and careers, AJD offers a unique opportunity to investigate the mechanisms underlying the Black-White student debt over the life course. Researchers and policymakers should adopt an intersectional lens to analyze and interpret findings from high-quality social science studies like AJD and from administrative (or “big”) data to better understand the demography and impact of the student debt crisis. In turn, they might develop evidence-based policy interventions that account for the structural determinants of student debt borrowing and repayment and help close the wealth gap between Black and White women and men in the United States.

Meghan Dawe is a Resident Research Fellow at the Center on the Legal Profession and a sociologist whose research analyzes the relationship between law and inequality through the lens of the legal profession and lawyers’ careers. She is engaged in four research projects at the Center on the Legal Profession. The first project is a co-authored book on the results of the first three waves of After the JD (AJD), a national longitudinal study of a cohort of American lawyers based at the American Bar Foundation for which Meghan is the Project Manager.

Acknowledgment: Statistical support was provided by data science specialist Dan Yuan at Harvard University’s Institute for Quantitative Social Science.

- Pyne, Jaymes, and Eric Grodsky. 2020. “Inequality and Opportunity in a Perfect Storm of Graduate Student Debt.” Sociology of Education 93(1):20–39; Webber, Karen L., and Rachel A. Burns. 2022. “The Price of Access: Graduate Student Debt for Students of Color 2000 to 2016.” Journal of Higher Education 93(6):934–61. [↩]

- Webber and Burns 2022. [↩]

- Pyne and Grodsky 2020. [↩]

- Jiménez, Dalié, and Jonathan D. Glater. 2020. “Student Debt Is a Civil Rights Issue: The Case for Debt Relief and Higher Education Reform Symposium – United States of Debt.” Harvard Civil Rights–Civil Liberties Law Review 55(1):131–98. [↩]

- Taylor, Aaron N. 2018. “Robin Hood, in Reverse: How Law School Scholarships Compound Inequality.” Journal of Law and Education 47(1):41–108. [↩]

- Deo, Meera E. 2021. “The End of Affirmative Action.” North Carolina Law Review 100:237–80. [↩]

- Dinovitzer, Ronit, and Bryant Garth. 2015. “Lawyers and the Legal Profession.” In The Handbook of Law and Society,103–17. Edited by Austin Sarat and Patricia Ewick. Hoboken, NJ: John Wiley & Sons. [↩]

- AAUW 2017; Kent, Ana Hernández, and Fenaba R. Addo. 2022. “Gender and Racial Disparities in Student Loan Debt.” Federal Reserve Bank of St. Louis, November 10. https://www.stlouisfed.org/publications/economic-equity-insights/gender-racial-disparities-student-loan-debt; Scott-Clayton, Judith, and Jing Li. 2016. Black-White Disparity in Student Loan Debt More Than Triples After Graduation. Brookings Institution, October 20; Houle, Jason N., and Fenaba R. Addo. 2019. “Racial Disparities in Student Debt and the Reproduction of the Fragile Black Middle Class.” Sociology of Race and Ethnicity 5(4):562–77. [↩]

- AAUW 2017. [↩]

- Kent and Addo 2022. [↩]

- Houle and Addo 2019, 573. [↩]

- Houle and Addo 2019; Pfeffer, Fabian T., and Alexandra Killewald. 2019. “Intergenerational Wealth Mobility and Racial Inequality.” Socius: Sociological Research for a Dynamic World 5. https://doi.org/10.1177/2378023119831799; Killewald, Alexandra. 2013. “Return to Being Black, Living in the Red: A Race Gap in Wealth That Goes Beyond Social Origins.” Demography 50(4):1177–95. [↩]

- Houle and Addo 2019; Seamster, Louise, and Raphaël Charron-Chénier. 2017. “Predatory Inclusion and Education Debt: Rethinking the Racial Wealth Gap.” Social Currents 4(3):199–207; Maroto, Michelle. 2016. “Growing Farther Apart: Racial and Ethnic Inequality in Household Wealth Across the Distribution.” Sociological Science 3:801–24; Sykes, Bryan L., and Michelle Maroto. 2016. “A Wealth of Inequalities: Mass Incarceration, Employment, and Racial Disparities in U.S. Household Wealth, 1996 to 2011.” RSF: The Russell Sage Foundation Journal of the Social Sciences 2(6):129–52; Dwyer, Rachel E. 2018. “Credit, Debt, and Inequality.” Annual Review of Sociology 44(1):237–61; Pager, Devah, and Hana Shepherd. 2008. “The Sociology of Discrimination: Racial Discrimination in Employment, Housing, Credit, and Consumer Markets.” Annual Review of Sociology 34(1):181–209. [↩]

- Killewald, Alexandra, and Brielle Bryan. 2018. “Falling Behind: The Role of Inter- and Intragenerational Processes in Widening Racial and Ethnic Wealth Gaps Through Early and Middle Adulthood.” Social Forces 97(2):705–40. [↩]

- Oliver, Melvin L., and Thomas M. Shapiro. 1997. Black Wealth / White Wealth: A New Perspective on Racial Inequality. London: Routledge; Seamster, Louise. 2019. “Black Debt, White Debt.” Contexts 18(1):30–35; Killewald and Bryan 2018. [↩]

- Sullivan, Laura, Tatjana Meschede, Thomas Shapiro, and Fernanda Escobar. 2019. “Stalling Dreams: How Student Debt Is Disrupting Life Chances and Widening the Racial Wealth Gap.” Institute on Assets and Social Policy, September. https://heller.brandeis.edu/iere/pdfs/racial-wealth-equity/racial-wealth-gap/stallingdreams-how-student-debt-is-disrupting-lifechances.pdf; Seamster 2019. [↩]

- Sullivan et al. 2019. [↩] [↩]

- Jackson, Brandon A., and John R. Reynolds. 2013. “The Price of Opportunity: Race, Student Loan Debt, and College Achievement.” Sociological Inquiry 83(3):335–68. [↩]

- Scott-Clayton and Li 2016; Pyne and Grodsky 2020. [↩]

- Wright 2023. [↩]

- Olivas, Michael A. 1999. “Paying for a Law Degree: Trends in Student Borrowing and the Ability to Repay Debt.” Journal of Legal Education 49(3):333–41. [↩]

- Kornhauser, Lewis A., and Richard L. Revesz. 1995. “Legal Education and Entry into the Legal Profession: The Role of Race, Gender and Educational Debt.” New York University Law Review 70:829–964. [↩]

- Olivas 1999. [↩]

- Agénor, Madina, Nancy Krieger, S. Bryn Austin, Sebastien Haneuse, and Barbara R. Gottlieb. 2014. “At the Intersection of Sexual Orientation, Race/Ethnicity, and Cervical Cancer Screening: Assessing Pap Test Use Disparities by Sex of Sexual Partners Among Black, Latina, and White U.S. Women.” Social Science and Medicine 116:110–18. [↩]

- Houser, Kimberly A., and Jamillah Bowman Williams. 2021. “Board Gender Diversity: A Path to Achieving Substantive Equality in the United States.” William and Mary Law Review 63(2):497–560. [↩]

- Nelson, Robert L., Ioana Sendroiu, Ronit Dinovitzer, and Meghan Dawe. 2019. “Perceiving Discrimination: Race, Gender, and Sexual Orientation in the Legal Workplace.” Law and Social Inquiry 44(4):1051–82. [↩]

- Jackson and Williams 2022. [↩]

- Kornhauser and Revesz 1995. [↩]

- Addo, Fenaba R., Jason N. Houle, and Daniel Simon. 2016. “Young, Black, and (Still) in the Red: Parental Wealth, Race, and Student Loan Debt.” Race and Social Problems 8(1):64–76 [↩]

- Perry et al. 2021. [↩] [↩]

- Charron-Chénier, Raphaël, Louise Seamster, Thomas M. Shapiro, and Laura Sullivan. 2022. “A Pathway to Racial Equity: Student Debt Cancellation Policy Designs.” Social Currents 9(5): 4–24. [↩]

- Warren, Elizabeth. 2020. “My Plan to Cancel Student Loan Debt on Day One of My Presidency.” Warren for Senate, last accessed August 28, 2023. https://elizabethwarren.com/plans/student-loan-debt-day-one; Sanders, Bernie. 2020. “College for All and Cancel All Student Debt.” Bernie, last accessed August 28, 2023. https://berniesanders.com/issues/free-college-cancel-debt/; Whistle, Wesley. 2020. “Senator Elizabeth Warren Announces a New Plan to Cancel Student Debt.” Forbes, January 14. https://www.forbes.com/sites/wesleywhistle/ 2020/01/14/senator-warren-announces-a-new-plan-to-cancel-student-debt/?sh=1da441421c1d; Jiménez and Glater 2020; Perry et al. 2021. [↩]

- US Treasury Department. 2023. “What Is the National Debt?” Last accessed August 27, 2023. https://fiscaldata.treasury.gov/americas-finance-guide/national-debt/. [↩]

- Federal Deposit Insurance Corporation. 1997. “The Savings and Loan Crisis and Its Relationship to Banking.” History of the Eighties—Lessons for the Future, Volume 1, Chapter 4. Washington, DC: Federal Deposit Insurance Corporation; Harbert, Tam. 2019. “Here’s How Much the 2008 Bailouts Really Cost.” MIT Management Sloan School, February 21. https://mitsloan.mit.edu/ideas-made-to-matter/heres-how-much-2008-bailouts-really-cost#:~:text=By%20those%20calculations%2C%20the%20total,gross%20domestic% 20product%20in%202009; Bureau of Labor Statistics. 2023. “CPI Inflation Calculator.” Last accessed August 27, 2023; CPI Inflation Calculator. https://data.bls.gov/cgi-bin/cpicalc.pl?cost1=500&year1=200801&year2=202307. [↩]

- Jiménez and Glater 2020. [↩]

- Choo, Hae Yeon, and Myra Marx Ferree. 2010. “Practicing Intersectionality in Sociological Research: A Critical Analysis of Inclusions, Interactions, and Institutions in the Study of Inequalities.” Sociological Theory 28(2):129–49; Viterna, Jocelyn. 2023. “Gender and Intersectionality.” Sex, Gender, Sexuality Program. Harvard Extension School, June 26. [↩]