This article is derived from the authors’ larger work, “The Integration of Law into Global Business Solutions: The Rise, Transformation, and Potential Future of the Big Four Accountancy Networks in the Global Legal Services Market” in Law and Social Inquiry. The full paper is available for download here.

Throughout the 1990s, the Big Five accounting firms—Arthur Andersen, KPMG, Ernst & Young (EY), PricewaterhouseCoopers (PwC), and Deloitte—made a concerted effort to enter the legal services market. This effort was particularly pronounced—and particularly successful—in Europe. By the close of the twentieth century, legal networks that were directly owned or closely affiliated with the Big Five were major players in many markets around the world, and were threatening to enter markets in which they were still barred, such as in the United States. However, after the wave of accounting scandals that arose out of the 2001 financial crises—which brought down Arthur Andersen and ushered in regulatory reforms in the United States and other major economies that appeared to place severe restrictions on the ability of the now Big Four to offer nonauditing services to their audit clients—most observers concluded that the accounting firms’ legal networks were effectively dead. As a result, both practitioners and academics stopped paying attention to what these firms were doing in law.

Our research, however, points to a quite different conclusion. Using a unique data set comprised of information collected from the corporate websites of the Big Four and their affiliated or strategic partner law firms, as well as archival material accessible from the legal and accountancy press, we demonstrate, as Mark Twain might say, that the reports of the death of the Big Four’s legal ambitions have been greatly exaggerated. Far from dying, in recent years the legal service lines linked to the international accountancy networks have grown significantly in size, scope, and importance. Nor are the legal services these networks deliver confined to tax issues. Although tax-related advisory services remain an important cornerstone, the Big Four legal networks are now important players in a broad range of legal fields, including premium and fast-growing practices such as compliance, finance, M&A, and employment law.

As Mark Twain might say, the reports of the death of the Big Four’s legal ambitions have been greatly exaggerated.

Moreover, as impressive as the expansion of their legal networks has been over the last decade, there are good reasons to believe that the Big Four will be even more successful in penetrating the corporate legal services market in the decades to come. It is by now common knowledge that corporate clients are increasingly seeking globalized solutions that integrate law into a wider category of “business solutions”—precisely the approach these globally integrated multidisciplinary firms now champion. In the last decade of the twentieth century, the accounting firms attempted to enter the legal services market by aping the ways of large law firms, who at the time were universally acknowledged to be the market leaders. In the second decade of the twenty-first century, large law firms are now attempting to demonstrate that they can provide the same kind of seamless integration of law into effective global business solutions currently being championed by the Big Four (see “Navigating a Brave New World”). Indeed, by increasingly making themselves look like the Big Four in how they define and deliver legal services, large law firms may actually be hastening a world in which these global giants will no longer have to disguise their ambitions from regulators and the public.

The Takeaway

In the 1990s, the major accounting firms mounted a major campaign to capture a significant part of the legal services market around the world. After the accounting scandals in 2001 and the resulting regulation prohibiting auditors from providing legal and other nonaudit services to their audit clients, most practitioners and commentators assumed that these ambitions were dead. However, over the last decade the Big Four accounting firms have quietly rebuilt their legal networks, integrating these services into a new model of “globally integrated business solutions,” and aggressively promoting this model in important emerging economies in Asia-Pacific, Latin America, Africa, and the Middle East. Recent trends toward relaxing restrictions against “alternative business structures” and “multidisciplinary practice” are likely to accelerate the growth of the Big Four’s legal networks.

It is still unclear whether any of the Big Four will be able to fulfill their ambitions of building, as Alexandru Reff, partner-in-charge of Deloitte’s Romanian tax and legal practice, confidently declared in 2013: “the largest legal network in the world.” It is, after all, far easier to promise seamless global multidisciplinary services than it is to deliver them. As we detail below, our research tracks primarily what the Big Four and others are saying about the legal services that are being delivered by their legal networks, as opposed to what they are actually doing in various markets. Moreover, much of law, and the regulation of how law is practiced, remains both local and in the hands of lawyers, which many argue safeguards important values that protect clients and the public but which also certainly protects the legal profession from competition from outsiders such as the Big Four legal networks. Nevertheless, Deloitte, PwC, KPMG, and EY can all credibly claim to be able to provide, according to Reff, “global presence” and the “ability to understand businesses and operate pragmatically, in close connection with experts from other areas, at costs optimized through efficient processes and technologies.” That is likely to make the Big Four formidable competitors in the new climate of more for less (see “A Global Age of More for Less”), which even the most skeptical observers now concede is reshaping the global market for corporate legal services.

In the remainder of this essay we summarize our research about what the Big Four have been doing since many proclaimed the death of their legal networks, and we discuss why, notwithstanding regulation expressly designed to destroy them, these networks have not only survived but thrived—and seem likely to expand even further in the future. We begin, however, with a brief history of the rise and fall of the big accounting firms’ original legal networks.

Historical background

Lawyers and accountants have long competed over the terrain at the intersection of the two fields, particularly in the area of tax. Although this competition produced different resolutions in different countries, over the years the two professions reached a relatively stable equilibrium in which the accounting firms controlled most or all of the tax advisory field with the exception of the high-end tax work large law firms and specialized tax boutiques continue to do.

This uneasy truce, however, began to fray in the 1980s. Faced with declining margins in their core audit business, the Big Five began to offer a growing arsenal of nonaudit consulting services to their audit clients, particularly in the areas of information technology and financial management. Many of the most profitable of these new areas—e.g., corporate restructuring, insolvency, litigation support, and forensic accounting services—intersected significantly with law. In recognition of this new reality—and to exploit its potential—the Big Five ceased calling themselves accounting firms and began marketing aggressively as a new brand of multidisciplinary professional service organization (MDP). It wasn’t long before the “disciplinary” services offered by these increasingly large and global organizations included a broad range of legal services.

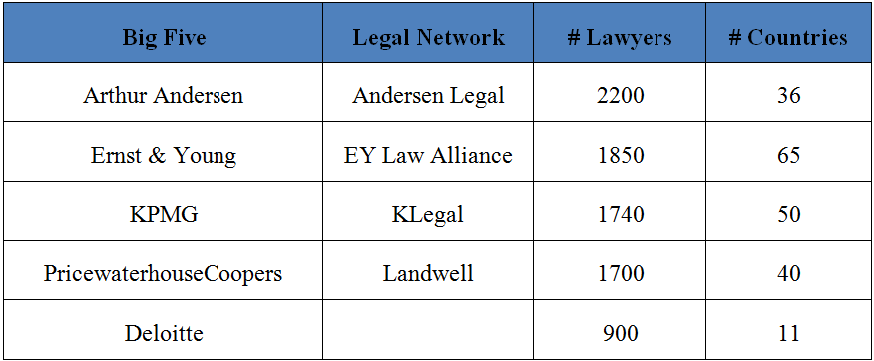

To deliver these services—and to placate regulatory officials in both law and accounting who were becoming concerned about the integration of the two disciplines—the Big Five began setting up independent legal networks that nevertheless operated under the overall umbrella of the accounting firms. The strategy was simple: look as much like a traditional law firm as possible. These networks grew rapidly during the 1990s, in part through the recruitment of “star” lawyers from law firms and government. As table 1 indicates, by the early 2000s, four of these networks—Andersen Legal, Landwell, Klegal, and EY Law—were as large as the largest law firms in the world. Accompanying this growth was a concerted public relations campaign to portray each of the Big Five legal networks as just another top firm—only bigger.

Table 1

This charm offensive, however, failed to impress the American Bar Association (see “Speaker’s Corner”) or the U.S. Congress. Citing the core values of the legal profession—conflict of interest, independence, and client privilege—in 2000 the American Bar Association’s House of Delegates rejected the recommendation of its own Commission on Multidisciplinary Practice that the Model Rules of Professional Conduct be amended to permit integrated MDPs such as the Big Five’s legal networks. Shortly thereafter, Enron and WorldCom collapsed, triggering a credibility crisis that the accounting profession had not experienced since the 1929 stock market crash.

The regulatory response was swift and, for the soon-to-be Big Four’s legal ambitions, apparently devastating. Arthur Andersen was criminally indicted and eventually declared bankruptcy. The U.S. Congress passed the Sarbanes–Oxley Act (SOX), prohibiting audit firms from providing certain nonaudit services to their clients, including legal services unrelated to the audit. A Public Company Accounting Oversight Board (PCAOB) was created to oversee implementation of standards and ethics rules related to audit practice aimed at strengthening auditor independence. Similar laws prohibiting the provision of specific nonaudit services by a public company’s auditor were enacted in many countries worldwide, including Mexico, Germany, China, Japan, France, Australia, and Canada.

In the years following SOX, the Big Four quickly unbundled their legal networks—or again, so it seemed. The logic behind these actions seemed both impeccable and indisputable. As no less an astute observer than the Economist declared in 2003: “When law firms hardly benefit from accountants’ huge client base and accountancy firms are allowed to offer legal services only to a few clients, there is little point in accountants having a legal arm. Moreover, law firms have themselves become more global in recent years and many do not need the accountancy giants’ international reach. ‘Accountancy firms’ drive in the legal arena is dead,’ says John Malpas of Legal Week, a trade publication.”

The Big Four have spent the last decade gradually rebuilding and strengthening their legal networks.

But as the old saw goes, predictions are hard—especially about the future. Far from abandoning their “drive in the legal arena,” the Big Four have spent the last decade gradually rebuilding and strengthening their legal networks. Moreover, they have done so in a manner befitting the competitive realities of the twenty-first century, as opposed to attempting to copy the model many law firms still use that was created to fit the realities of the nineteenth century.

Empirical research and methodology

To investigate whether SOX and other related legislation has in fact signaled the death knell of the Big Four’s legal ambitions, we examined the corporate websites of the Big Four and their affiliated law firms over several years. Websites have become a “virtual storefront” used by companies to promote their products and services. As such, they offer an approved, official, and formalized account of how the company wishes to be viewed, and they provide an important way of assessing what companies are trying to achieve and how these goals may be evolving over time.

From July 2011 to March 2012, we researched the corporate websites of PwC, Deloitte, KPMG, and EY, as well as those of affiliated law firms, collecting the following data: the location where legal services were promoted (global, regional, individual country sites); whether the websites mentioned that the firm provides legal services (if any); the web path to access legal services; the list of law practices offered; and the general textual description of the legal services.

Since a website is a hierarchy of information connected via hyperlinks to other sites or pages, we explored the websites using a top-down criteria to identify the information collected. Our goal was not only to track where “legal services” or another similar term appeared on one of the Big Four’s main websites but also to see whether these services were displayed on other country-specific, service-specific, or affiliated entities’ websites—and how easy or difficult it was to discover what (if any) legal services were being offered. Thus, in addition to examining each of the Big Four’s main websites, we also investigated a total of 491 location sites (151 PwC, 123 Deloitte, 102 KPMG, and 115 EY).

We also conducted a general search on Google using the brand names of the Big Four plus the key words legal and law allowing for the identification of a limited number of law firm websites that, despite not being accessible through a Big Four website, nevertheless were self-described as affiliated, associated, or strategic partners with one of the Big Four. Finally, we conducted a general search of the legal, accountancy, and economic press regarding the Big Four legal practices post-SOX.

In November 2015 we repeated the entire search process to determine what, if anything, had changed since 2012.

As the data underscores, our research methodology uncovered a wealth of information about how the Big Four have presented their legal networks in the years since SOX. What this kind of study cannot tell us, however, is whether what the Big Four say about their legal networks is in fact true. We therefore make no representation, for example, about whether the legal services that the Big Four claim to offer in any particular legal market are, in fact, being delivered, or whether their legal work is high quality. Nevertheless, given the data we report about what the Big Four are saying about the rapid growth in the size, sophistication, and geographic scope of their legal networks—and about the monetary and human resources they are devoting to building this capability—it would be surprising if what these large and sophisticated players are presenting on their websites does not bear some important connection to reality. Indeed, as we indicate below, the Big Four’s practices have now been recognized by major ranking services such as Chambers and Partners and the Financial Times as among best in their respective markets. At a minimum, the web presence we document reveals the Big Four’s ambitions for their legal services arms—as well as what they think will appeal to potential clients, and what they fear will be revealed to potential competitors and regulators.

Hiding in plain sight

Our empirical research reveals that far from fading away, the Big Four have reemerged as major players in the global legal services market, arguably staking out a position that is even more prominent than the one they occupied prior to SOX. Specifically, our data demonstrates that the Big Four have quietly managed to:

- Rebuild and expand the reach of their legal networks, including diversifying their practice expertise beyond tax law and their regional coverage beyond Europe

- Structure their legal practices through the most highly integrated form of MDP to enhance the provision of truly integrated legal services and innovative business solutions

- Increase the global visibility given to their expertise in law

Practice and regional expansion and diversification

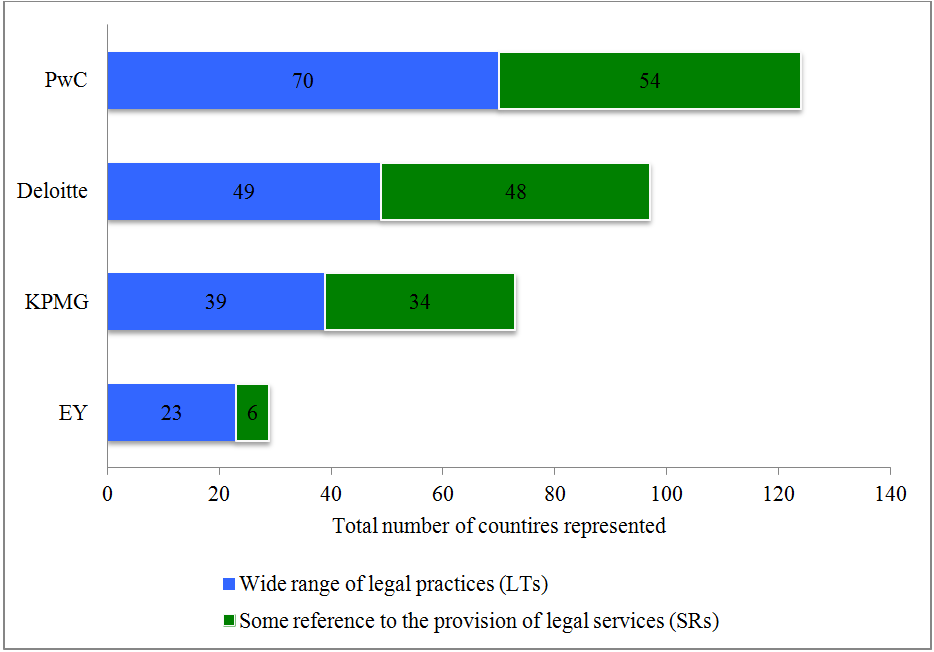

Figure 1 underscores just how much the Big Four have expanded the size and scope of their legal networks since 2001. In the spring of 2012, PwC was promoting legal services in 124 countries worldwide, Deloitte in 97 countries, KPMG in 73 countries, and EY in 29 countries.

Figure 1

Moreover, in the majority (and in the case of EY, the overwhelming majority) of these jurisdictions, the Big Four claimed to be offering a wide range of legal services—services that go far beyond their traditional expertise in tax law to address the growing need by multinational businesses for multidisciplinary business solutions across a global network. We refer to the jurisdictions in which the Big Four claim to deliver a broad range of legal services as “legal territories,” or “LTs.” Jurisdictions where only a narrow range of legal services (often primarily related to tax) are referred to as having “some reference” to law, or “SRs.”

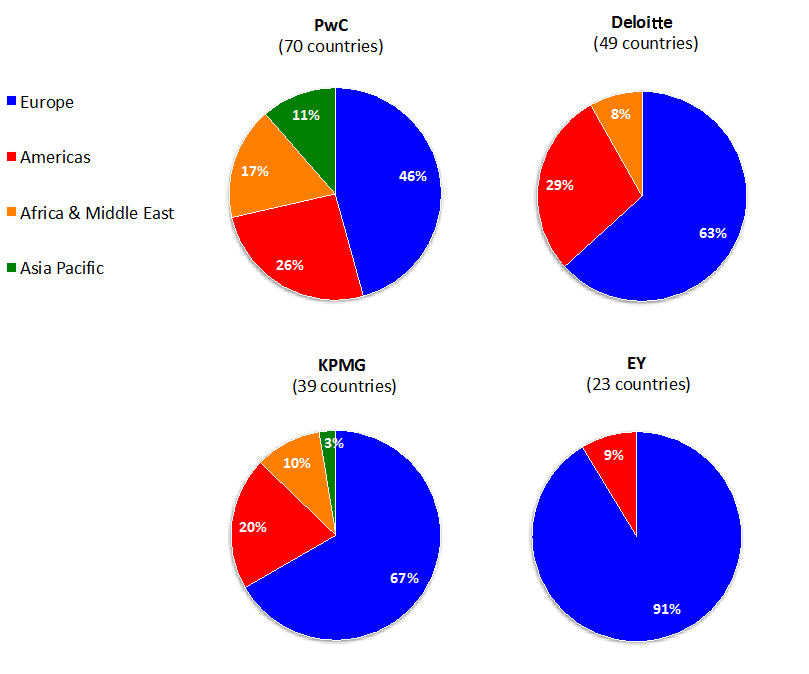

Finally, as figure 2 underscores, the Big Four have expanded the jurisdictional reach where they deliver a wide range of legal services far beyond their traditional European roots to include the fast-growing emerging economies in Asia-Pacific, Latin America, and Africa. As an illustration of the reputation achieved by some of these practices over the years, Chambers and Partners (2011) describes PwC Laos as a first-tier firm for “general business law,” which offers “a full-service transactional practice that is particularly known for its corporate, M&A, and IP work.”

Figure 2

Integration

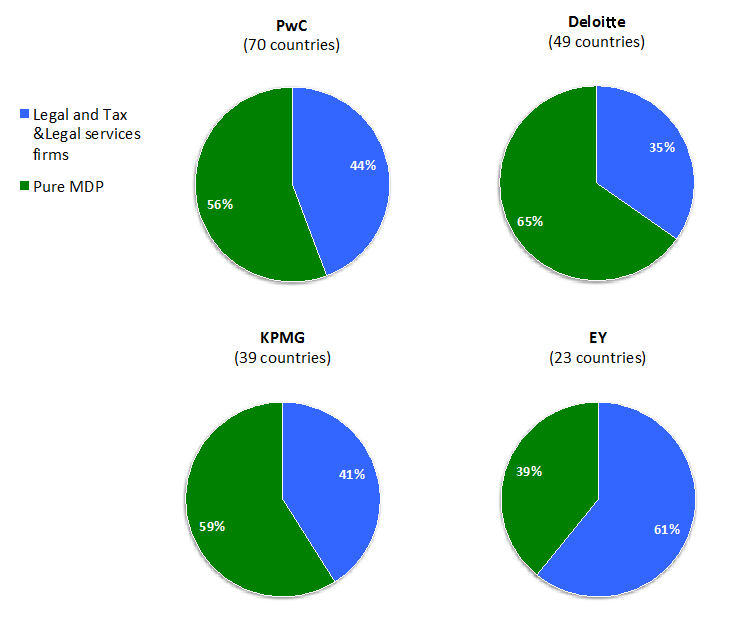

In addition to expanding both the substantive and geographic reach of their rebuilt legal networks beyond where they were in 2001, the Big Four have also begun to integrate these legal practices into their global multidisciplinary umbrella far more extensively than they did in the 1990s. As figure 3 illustrates, as of March 2012, in the majority of PwC LTs (56 percent), Deloitte LTs (65 percent), and KPMG LTs (59 percent), legal practices appeared on the web with no mention of any particular freestanding law firm or legal services firm as providing these services. Even in the minority of cases where legal services were described on the website of an independent law firm that was neither mentioned on nor linked to the Big Four’s own site, the law firms in question typically made explicit reference to their “alliance” with the other multidisciplinary practices under the particular Big Four firm’s umbrella through branding and other promotional material. The overall result is a clear effort to move away from the old strategy of law as a separate and largely independent service line and to embrace the vision of legal services as part of a globally integrated business solution for global clients.

Figure 3

Visibility

Although the Big Four have been quick to represent their new legal offerings as an integral part of their business model to clients, they have been less forthcoming about making this fact easily visible to the outside world. Notwithstanding the extensive reach of the Big Four legal networks by March 2012, legal services were accessible mostly on local websites and integrated with the tax function. Thus, the global websites of Deloitte, KPMG, and EY did not mention the countries where their local firms provided legal services to clients. Nor are the extensive legal offerings available in LTs typically accessible through a straightforward reference to “legal” or “law” on the accounting firms’ primary websites. Instead, the majority (54 percent) of these territories are only accessible through a “tax” or “tax and legal” core service line—notwithstanding, as we indicated above, that a much broader range of services beyond what has traditionally been considered to fall within these categories are offered. Finally, in 2011 and 2012, there was no reference concerning the provision of legal services in any of the Big Four’s global annual reports.

By the spring of 2012, however, PwC was beginning to take a bolder and more ambitious approach. Unlike the other firms, PwC featured a main legal service line as a hypertext integrated within the collection of its global services and linked to a PwC Global Legal Services Network (GLSN) website. The GLSN site reveals that the network was engaged in a full range of business-related legal services, resembling those typically promoted by a business law firm. At the same time, the site also highlighted a global, multidisciplinary, and solution-oriented approach as the network’s main source of differentiation from traditional law firms. In addition, PwC’s GLSN website gave access to the list of countries where legal services were offered by PwC, including 20 full-scale legal practices representing 29 percent of PwC’s LTs, which were otherwise not visible at the individual country–level website.

It is not surprising that PwC was more aggressive in staking this claim in 2012 than its rivals. Its legal network Landwell was the only accountancy-tied law firm network to survive SOX, and in March 2012 was still accessible through its own site on the Internet which showed law firms operating in five European countries. Unlike in 2003, however, where PwC sought to portray Landwell as an independent network, by 2012 four of Landwell’s law firms had already been integrated into PwC’s GLSN. As a result, PwC claimed in 2014 that its “global legal business has delivered substantial double-digit revenue growth since 2007.” Not surprisingly, these results have not escaped the attention of the remaining three members of the Big Four.

Where are they headed?

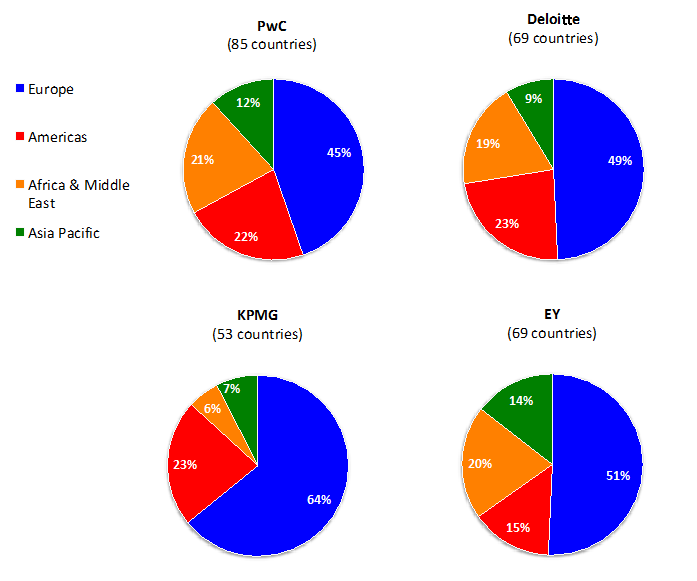

When we revisited the Big Four’s websites in 2015, it was clear that time had reaffirmed each of the three trends identified above. By June 2015, Deloitte, EY, and KPMG had all joined PwC in giving global visibility to their extensive legal expertise in all areas of business-related law. Similarly, revisiting the global websites of the Big Four in November 2015 also confirmed the remarkable international expansion and regional diversification of these networks into emerging markets (figure 4). Most notably, since March 2012, EY has increased by 200 percent the number of countries where its member firms offer a wide range of LTs, thus shifting from the almost exclusive location of LTs in Europe (figure 2) to having 20 percent of LTs in Africa and the Middle East, and 14 percent in Asia-Pacific.

To support this expansion, the Big Four have returned to the kind of lateral recruiting of star lawyers not seen since the 1990s. Consider, for instance, Richard Norbruis, whom EY recruited to become its global transaction law leader and a member of its Global Law Leadership team. Prior to being hired by EY, Norbruis was at Freshfields Bruckhaus Deringer, where he was the firm’s global people partner and a member of the Partnership Council. Similarly, PwC recently poached another Freshfields partner, Nikolaus Schrader, who recently joined to colead its nationwide corporate and M&A practice group, as well as Tony O’Malley, former King & Wood Mallesons’ deputy global managing partner, who now leads PwC’s legal practice in Asia-Pacific. Not to be outdone, KPMG recently hired DLA Piper’s joint head of the Asia-Pacific corporate practice, David Morris, to lead and develop the accounting firm’s legal practice in Australia beyond its traditional concentration on tax law.

As impressive as this lateral hiring spree is, however, the fact that each of the global leaders of the Big Four’s legal networks have all grown up inside these organizations underscores their strong commitment to integrating these practices into the broader culture and practices of their global multidisciplinary network. To accomplish this goal, KPMG, EY, and Deloitte have followed PwC’s lead of integrating their independent law firm partners into their umbrella networks. For example, since 2012, Deloitte has initiated the process of fully integrating its German strategic partner Raupach & Wollert-Elmendorff Rechtsanwaltsgesellschaft mbH into the Deloitte network—now rebranded as Deloitte Legal Rechtsanwaltsgesellschaft mbH—as well as rebranding its Canadian-affiliated law firm Heddema & Partners LLP to Deloitte Tax Law LLP.

Finally, and most importantly, in 2013-2014 PwC, KPMG, and EY all filed applications to launch an alternative business structures (ABS) that will allow them to provide legal services in the United Kingdom under the new law that allows for organizations not exclusively owned and controlled by lawyers to deliver legal services. Significantly, two of the three—EY and KPMG—have now been granted an ABS license to become a multidisciplinary professional service firm, under which they are now entitled to provide a mix of legal and nonlegal services to clients.

Clearly in 2015, more than a decade after they were proclaimed dead by most pundits, the Big Four’s increasingly integrated and expansive legal networks are alive and well in the global market for legal services. Indeed, in the Financial Times’ Innovation Awards for this year, PwC Tax and Legal Services in Spain was named the third-most innovative law firm in continental Europe, ahead of such traditional Spanish powerhouses as Cuatrecasas and Uría Menéndez, which were ranked fourth and fifth respectively (see “In the News”). The question is, how did this happen right under the nose of so many people who thought that they had ensured that just such a result could never take place? More importantly, what are the implications of the Big Four’s ability to sidestep the death sentence they were given by both bar organizations and regulators for their future ambitions in the legal arena, and for the future of that arena in general?

How did this happen?

Looking back, we believe that four interrelated factors allowed the Big Four accounting firms to expand their legal offerings:

- Gaps in the regulation of auditor independence

- Changes in the legal profession’s regulatory framework

- The organizational evolution of the Big Four

- Globalization and the attractiveness of the global market for legal services

Significantly, each of these developments appears likely to continue in the coming years, thereby accelerating the growth and importance of the Big Four’s legal networks.

Gaps in the regulation of auditor independence

Contrary to popular perception, section 201 of SOX did not establish an audit-only rule for the accounting firms. Instead, it provides a list of nonaudit services (NAS) that are off-limits for registered public accounting firms regarding their U.S.-listed audit clients and empowers the audit committees to preapprove the purchase of tax services and other “SOX-permissible” NAS from the auditor. This framework, however, is far less clear or determinate than it might appear, given the difficulty in defining where auditing ends and consulting begins. As a result, accountants have been able to continue to provide publicly traded U.S. audit clients with a wide range of advisory services in fields where accounting, consulting, and law overlap, such as risk and compliance, financial management, human resource organization, forensics, merger due-diligence services, and high-end tax services—all of which involve significant law or law-related issues in which law firms are also trying to give advice.

More importantly, even those nonaudit services that are acknowledged to fall under SOX are prohibited only for a Big Four firm’s own audit clients. Each firm is still lawfully permitted to target the large body of public companies they do not audit. These nonaudit clients have become the engine of growth for the Big Four’s legal practices.

In the rest of the world, the gaps in the regulatory framework regarding the delivery of nonaudit services by the Big Four have been even more extensive. In Europe, where the Big Four’s legal networks first regained their strength, the application of the European Union Directive on this issue was largely left up to individual member states, many of which adopted restrictions that were even less clear than SOX about what was prohibited. But even outright bans on accounting firms providing legal services in countries such as France and Germany have not prevented the revival of the Big Four legal practices in these important European countries.

These gaps in the regulation of auditors have in turn been accentuated by changes in the regulation of the legal profession.

Changes in the legal profession’s regulatory framework

Since the turn of the millennium, a growing number of governments have pressed for deregulating the market for legal services with the goal of promoting competition, reducing prices, and spurring innovation. The United Kingdom has been the most aggressive of the jurisdictions to take up this deregulatory crusade. Following Australia’s lead, the United Kingdom enacted the Legal Services Act of 2007 (LSA), ushering in the most influential deregulatory reforms in the history of the market for legal services anywhere in the world (see “How Regulation Is—and Isn’t—Changing Legal Services“). These reforms expressly authorized ABSs and MDPs and removed self-regulation in the legal profession by creating an independent body to oversee legal regulators in England and Wales. As indicated above, three of the Big Four have now applied to take advantage of this regulatory exemption.

Nor is the United Kingdom alone in following this path. In addition to Australia, where ABSs and MDPs have long been legal, several other countries are actively considering adopting similar reforms, including major legal markets such as Canada, South Korea, Singapore, and Hong Kong. Even in the United States, the American Bar Association’s 2020 Commission on the Future of Professional Regulation actively debated allowing MDPs for the first time since the House of Delegates rejected a similar recommendation in 2001. Although the proposal was ultimately defeated, the fact that it received serious consideration underscores just how far the deregulatory tide has moved in the last several years (see “Speaker’s Corner“).

At the same time, the Big Four have been able to exploit loopholes in the regulation of the legal profession in emerging economies where this regulatory framework is far less developed than it is in the West. Consider, for example, China. Although foreign law firms are barred from directly or indirectly investing in, managing, operating, controlling, or taking equity interests in Chinese law firms, there are no regulations expressly restricting the form or nature of cooperation between a Chinese law firm and an international accounting firm. Taking advantage of this regulatory ambiguity, on its website Deloitte China markets the provision of legal services through Qin Li Law Firm, “a licensed Chinese law firm that specializes in cross border legal advisory services,” as part of the international Deloitte legal services network.

As a result of these developments, much of what the Big Four have been quietly doing in the years following SOX is acquiring official status in many countries around the world. In addition, significant pressure is building for the deregulation of professional services at the transnational level through the General Agreement on Trade in Services (GATS). Significantly, the large accountancy networks have played a key role in framing this debate by actively pushing to eliminate global barriers to trade and investment in professional services. Ironically, notwithstanding their traditional distrust of government intervention, many big law firms have followed the accountants’ lead, lobbying both their own governments and the WTO for transnational rules barring states from enforcing restrictions on the entry of foreign law firms.

Lacking a large domestic market of their own, the U.K. firms have been particularly active in these debates. Since 2000, these firms have become, in the words of the English legal scholar John Flood, “agents of deregulation” at international and national forums. Thus, U.K. firms have actively lobbied for easing current restrictions on a wide range of regulatory issues, including conflicts of interest, the hiring and compensation of nonlawyer professionals, and new structures and practices such as Swiss vereins and the acceptance of outside capital. Many U.S. law firms are beginning to follow suit.

All these changes have made large law firms look more and more like the Big Four—only with an organizational form that is not nearly as well developed.

The organizational evolution of the Big Four

In the years following SOX, the legal market grew significantly, with large law firms expanding in size and geographic scope. The mantra for international law firms has been “premium work for premium clients,” thereby leading many firms to exit the commodity businesses in order to concentrate on high-margin assignments. By targeting only “bet the company” deals and litigation, however, top law firms unwittingly ceded the battle for industry expertise to the Big Four, who were only too happy to help their multinational clients with the full range of their legal problems and to treat these reoccurring legal matters as part of an overall business strategy. This new approach, in turn, dovetailed with the Big Four’s own organizational transformation from multidisciplinary firms, offering a variety of separate service lines, to integrated problem-solving networks with deep industry expertise. Leveraging their skill in process management and IT expertise across their increasingly large global footprint, the Big Four easily moved into spaces that the law firms were abandoning.

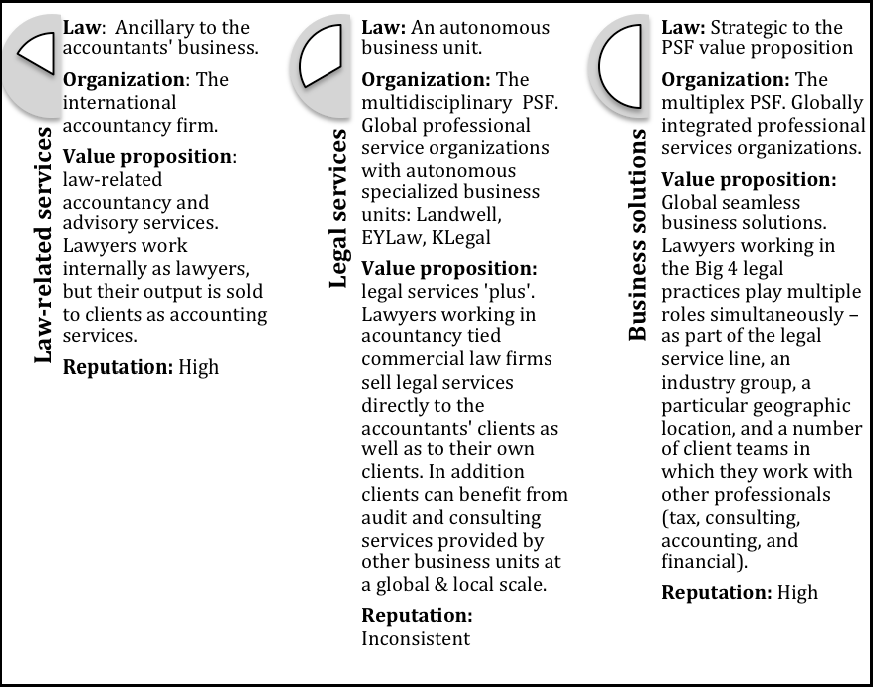

One can get a sense of the depth of this institutional transformation in the twin goals of “quality” and “integration” articulated by EY’s then-chairman and CEO, James Turley, in his farewell letter when he stepped down in 2012. Key to the realization of these objectives has been the development by EY and its Big Four counterparts of sophisticated client management systems, as well as the positioning of risk management at the core of their strategy, spanning all countries and services lines. In this model (Figure 5), lawyers working in the Big Four legal practices worldwide play multiple roles simultaneously—as part of the legal service line, an industry group, a particular geographic location, and a number of client teams—thus interacting with other professionals with different expertise around the world (e.g., tax, consulting, accounting, financial), industrial specialists, and/or local experts. As a result, these legal practices are now able to differentiate their value proposition from that of law firms by offering business solutions to corporate clients’ most complex challenges.

Figure 5

With global economic and regulatory uncertainty threatening the sustainability and growth prospects of multinational companies since the economic downturn beginning in 2008, clients increasingly cherished this partnering approach, requesting legal advisors that understand the company’s business and provide “value for money.” The Big Four understood this demand far more quickly than law firms. This was particularly true in Europe and other markets where indigenous firms were still very traditional, allowing the Big Four to leverage their existing relationships to move up the value chain, especially in areas at the intersection of law and business. Ian Tod, the former chairman of Deloitte Legal, explains this role: “The ones thinking that law as such is the most essential thing about our work do not get the point. The reason we are here is to help and advise our clients—that is the purpose of our work.”

Finally, the Big Four have been far quicker to realize that to remain globally competitive, they needed to develop a model for attracting, retaining, and developing human capital that is as well thought out and robust as their model for delivering high-quality services to clients. Thus, while law firms are becoming increasingly tough places to work, the Big Four are leveraging their culture of “global teaming” and a focus on “building a better working world”—as EY’s logo states—to increase their attractiveness for talent in the legal market (see “Life in the Big Four”).

Globalization and the attractiveness of the global market for legal services

Global megatrends, particularly the shift of economic power to emerging economies, have also favored the Big Four’s legal strategy. Multinational companies require consistent services around the globe, including legal services. Given their extensive experience in marshaling global resources, the Big Four are in an ideal position to meet this need, particularly in the emerging economies of Asia-Pacific, Latin America, and Africa, which are likely to see the fastest growth in the demand for legal services.

To take advantage of these opportunities, the Big Four have invested heavily in these high-growth markets during the last decade—investments that dwarf those made by any law firm. For example, in 2011, EY invested more than US$1.5 billion over five years, “mainly in the emerging markets,” and was planning to “maintain this investment at comparable levels for the foreseeable future.” With respect to legal services in particular, Legal Week published PwC’s aim to double the network’s lawyer headcount in Asia as part of an expansion plan. Similarly, Howard Adams, EY’s law leader in Australia, told The Lawyer that their plans were to double in size in the Asia-Pacific region by March 2015.

It is not hard to see why the Big Four are so interested in pursuing these opportunities. According to published estimates, the global legal services market grew 72 percent between 2005 and 2014, reaching a total value of US$616.4 billion. This amount represents three times the value of the audit market, according to data from MarketLine. Moreover, the global legal market is incredibly fragmented. While the Big Four’s joint turnover for audits in 2014 represents 23 percent of the value of global audits, the turnover jointly generated by all of the top law firms ranked in the Am Law 100 for the same year accounted for a scant 13 percent of the global legal market. In this context, if any of the Big Four were to capture even a 1 percent share of the global legal market’s forecasted value of $726.2 billion for 2019, that one network would become the largest legal services organization worldwide by far.

Finally, the Big Four are not only marshaling their financial resources to capture a larger share of this lucrative prize, they are also increasingly leveraging their already important role in the technology space through alliances with leading tech companies. The most recent and breathtaking initiatives have been led by PwC and EY. In 2014, PwC announced its joint business relationship with Google for Work to cocreate solutions for clients. “We bring in the content, they bring in the technology” explained PwC’s chairman Dennis Nally. More recently, EY has established an alliance with LinkedIn designed to “help companies develop deeper and more trusted customer relationships through the use of social and data analytics.” How these moves are going to impact their global legal businesses is yet to be seen. Nonetheless, it will surely prepare the Big Four for the technological disruptions that are already reshaping the global market for legal services.

Are we all consultants now?

In a prescient article published in 2002, the American legal scholar Robert Eli Rosen hypothesized that changes in the corporate market for legal services were turning both in-house counsel and outside firms into just another “consultant” whose primary task is to integrate legal knowledge into cross-functional teams to better achieve business objectives. As one of us has argued elsewhere, in the decade since Rosen’s article was published, changes in the economic and regulatory climate have only accentuated the trend he describes. Whether or not this trend results in the death of lawyer professionalism, as Rosen intimated, it will very likely further the legal ambitions of the Big Four. To the extent that the world of law is increasingly turning to traditional business methods such as unbundling, outsourcing, process management, and partnering to reduce costs and increase effectiveness, the legal networks of the global accounting firms have a distinct advantage. The Big Four have successfully utilized all of these processes to transform themselves from accounting firms to professional service organizations offering integrated global business solutions to complex problems at the intersection of finance, tax, strategy, organization—and increasingly law.

Several of the largest and most influential global law firms are now advertising themselves in ways that are indistinguishable from the Big Four’s self-presentation, dramatically underscoring just how much the legal world as a whole has moved to the latter’s terrain. When one adds the fact that the legal world is also shifting rapidly toward emerging markets in Asia-Pacific, Latin America, Eastern Europe, and Africa, where the Big Four already have a significant presence, the potential for the Big Four to carve out an even more dominant position in the global market for corporate legal services becomes even more apparent.

Time will tell whether these changes will finally allow the Big Four to achieve their renewed ambition to not only be important players in the global market for legal services but reshape the very definition of that market toward a view that law is simply one part of achieving a “globally integrated business solution.” And it remains to be seen what effect the Big Four’s growing presence in law will have on larger issues of lawyer professionalism, client service, and public policy. For now, we simply conclude by urging both practitioners and commentators to pay greater attention to what these important players are doing—and, equally as important, to what law firms, clients, and regulators are, or should be, doing in response.

David B. Wilkins is the Lester Kissel Professor of Law, faculty director of the Center on the Legal Profession and vice dean of global initiatives on the legal profession at Harvard Law School. Maria Jose Esteban is a lecturer at the Department of Law at ESADE-Universitat Ramon Llull, an affiliated researcher at the Harvard Law School Center on the Legal Profession, and co-director the Center’s Big Four research project. She is also a partner in the Spanish law firm Bugete Escura.